- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

A traders’ week ahead playbook – the equity juggernaut builds momentum

In the week ahead the known event risks are less impactful than what we faced last week, and we see catalysts that are more idiosyncratic to a set region. The RBNZ should hike by 50bp and indicate more is coming, and while much of this hike is already priced, I favour following the technical breakdown seen in EURNZD, GBPNZD, and GBPAUD EURAUD.

We get UK jobs and CPI inflation data (consensus 9.8% YoY ) which could seal a 50bp hike at the 6 Sept BoE meeting, or if weak swing the pricing towards 25bp – the latter which would naturally weaken the GBP – given UK rates market are already pricing 47bp of hikes for the Sept BoE, and there is a ceiling at 50bp (i.e the BoE won't hike by 75bp), then you can understand why the market is selling GBP, certainly against high beta FX (AUD, NZD, MXN). Watch the double top neckline in GBPUSD (daily chart) at 1.2003, if that goes this week then we could be ready to make a move to 1.1800/50.

The AUD looks well supported as global (and notably EM) equity markets fly – the Aussie Q2 wage and employment report could solidify the 50bp call for the September RBA meeting and see more being priced into the Aussie rates curve for the remainder of 2022. If equity markets remain supported, which seems likely to be the case, then weakness in the AUD should be mopped up, given its role as a thematic vehicle for trading an improvement in market sentiment – that said, a focus on a broad set of classic fundamental inputs also looks bullish for the AUD – where Aussie 10yr real rates, terms of trade and 2-year nominal bond yields are all outperforming that of the US and many other nations.

The equity juggernaut rolls on

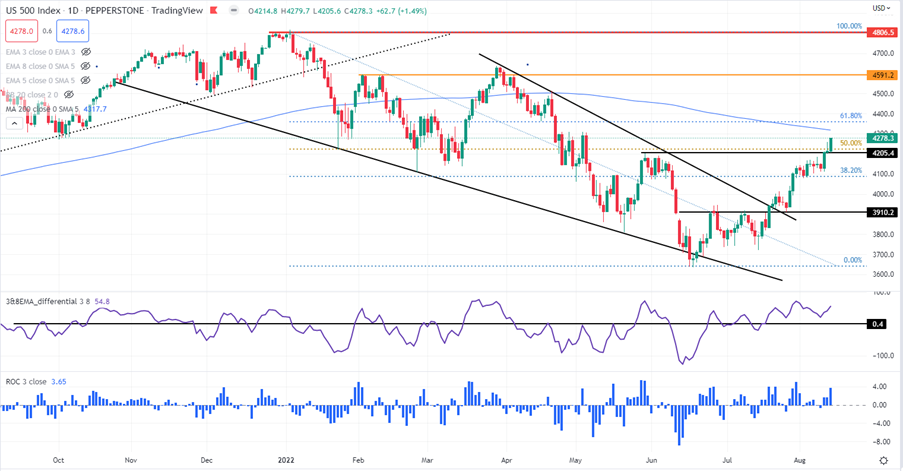

Arguably though the big talking point is around moves in global equity indices, many of which are showing real momentum. I like the JPN225 from the long side, but the NAS100 has rallied for four straight weeks and has led us higher, with names like Apple at the heart of the moves, rallying 33% from its lows of $129. As is the case for the US500 and US30, we look at fibo retracements of the Jan-June and April-June sell-downs as markers (and potential resistance), but we also eye the 200-day MA. The US 500 200-day MA comes in at 4317, so expect this to make headlines if breached.

The equity drivers?

There is no doubt that better US data has helped drive this bullish equity trend, and we can see the influence by a simple overlap with the Citigroup US economic surprise indices. The harder part for retail is the liquidity aspect and we must understand the plumbing in the US monetary system. So, while we’ve seen securities (Treasuries and Mortgages) holdings start to roll off the Fed’s balance sheet (BS) through QT, what’s important is that the liability side of the BS, and specifically the levels of excess reserves that commercial banks hold with the Fed, have been increasing – and at a faster clip than the securities they hold have fallen – in layman terms, this is essentially QE – better liquidity results in risk-taking.

We then turn to flow-based activity – as equities push higher options dealers have covered their delta hedges – while I could spend much time explaining this concept, essentially this has meant dealers buying back a sizeable short S&P500 and NAS100 futures position. We also saw ‘CTAs’ (Commodity Trading Advisors) – systematic trend-following hedge funds that use futures to trade trending markets buying back their short equity index futures exposures and are now net flat. Remember, these players are typically rules-based, and the talk is if S&P500 futures can push above 4310/20, then the trend players will start to buy S&P500 and NAS futures – a trigger then for a further push higher.

We also see the VIX index below 20% and S&P500 20- and 30-day realised volatility dropping hard – funds that target a level of volatility – or what we call ‘volatility control’ funds have been reducing cash holdings and adding capital into equities again. If statistical levels of S&P500 volatility continue to decline, then these massive players will add to the equity rally – it will also incentivise FX funds to be long ‘carry’ – or income – which means buying those currencies with the highest yields (or forward points)– we’re talking MXN, ZAR and NZD.

The equity rally is tough to fully grasp – getting the intel on many of these flow-based activities and truly understanding what is really going on can be a challenge for many – but as long as the liquidity dynamic holds up, US data comes in line and various big money players chase the tape higher then there may be more juice in the tank – I certainly wouldn’t get in front of it at this stage.

Another big week ahead – keep an open mind and prepare to react accordingly.

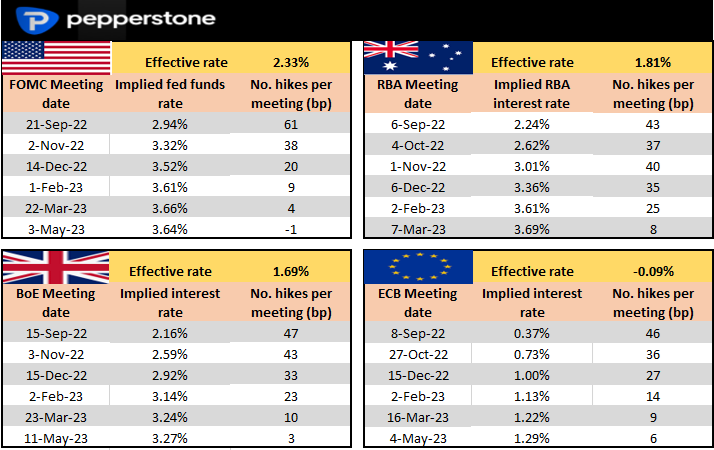

Rates Review – to help understand what is priced into market we look at interest rate pricing – here, we see the rates/swaps market pricing for the upcoming central bank meeting, and the step up (in basis points to the following meetings. For example, we see 61bp of hikes priced for the Sept FOMC meeting. We see 43bp of hikes priced for the next RBA meeting.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.