- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

Analysis

US 5-year real rates (i.e. US 5-year Treasury adjusted for expected inflation over the coming 5 years) have printed new cycle lows and sit at the lowest yield since May ’23.

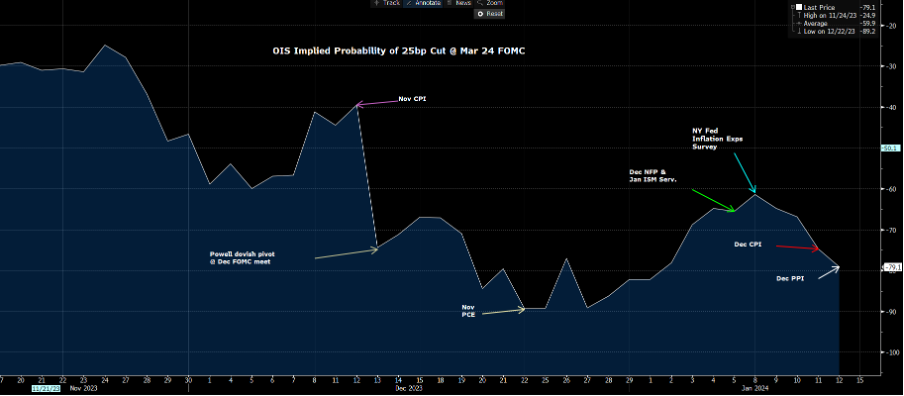

Some have stated the case that the US CPI print gives the Fed less scope to ease in March. Perhaps…but when we take the components from CPI and PPI that feed into the core PCE calculation (released 27 Jan), and we’re looking at an estimate of c. 0.2% mom, which sees the 6-month annualised rate of core PCE around 2% - and given core PCE is what the Fed set policy to – bingo, we have a clear justification as to why the bond and rates market feels March is the starting point.

The implied probability of the Fed cutting in March (h/t to my colleague Michael Brown for this chart)

Tuesday’s (Wed 03:00 AEDT) speech from Fed member Christopher Waller will be one of the key focal points this week, where recall he set off the rally in late November with definition on a timeline and a path to cut rates, which essentially started the Fed pivot and the year-end risk rally.

With talk of an earlier start to QT tapering and lower relative US bond yields, it’s a surprise that the USD is holding in so well with the DXY tracking a sideways range of 102.70 to 102.10. On the week the GBPUSD was the best performer in G10, with price pushing 1.2800, while the BRL got spoils in the EM FX space.

Gold has seen somewhat of a renaissance against this backdrop though, where on the 4-hr chart price closed above the recent downtrend, where on the daily price closed above the 5-day EMA. A weak US retail sales could offer renewed life for gold bulls and see price target 2075.

It's been a mixed picture in equity land, with much focus on the JPN225 gaining a massive 6.9% - although, the risk-to-reward trade-off suggests refraining from new longs and waiting for some of the heat to come out of the move. An RSI of 80 aside, 87% of stocks are above the 50-day MA, and 68% of stocks closed at a 4-week high. A sign of euphoria and a signal for contrarians or solid participation and therefore bullish? I favour the latter.

While US earnings continue to trickle in and the US election process officially kicks off in Iowa, China takes centre stage once again with retail sales, Q4 GDP, and property sales. China/HK equity remains challenged, but the tape is turning, and shorts are seeing signs that we may be turning from a trend position to one of trading a consolidation, where range trading in the CHINAH, HK50 and CN50 may be the strategy. We’ll see but if the data comes in softer, or we don’t see the level of monetary policy easing that’s priced, then frustration will likely see renewed selling flows.

The set-up in US equity indices look balanced with 2-week risk – the risk bulls will naturally want the US500 to clear 4800 and the NAS100 through 17k, but with options expiry across the VIX, index and single stock plays this week (schedule below), one questions if we see a higher volatility post expiration. An obvious consideration for one’s risk management.

Good luck to all.

The marquee event risks for traders to navigate this week:

US markets closed for MLK Day (Monday) – partial trade in futures.

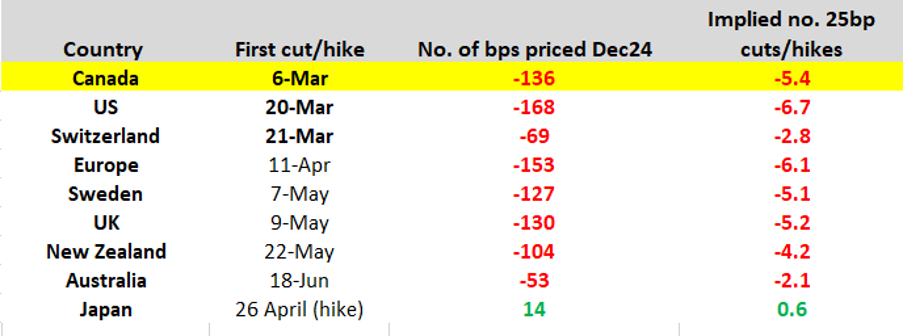

The markets anticipation for the start date for easing, and the magnitude of cuts priced into swaps

China 1-year MLF rate (15 Jan 12:20 AEDT) – we should see the PBOC cut the Medium-Lending Facility by 10bp to 2.4% (from 2.5%), with a chance they cut by 15bp to 2.35%. Anything less than a 10bp cut could weigh on CHINAH, CN50 and HK50. We also remain on watch for a cut to China’s bank reserve ratio requirement (RRR) as well.

UK employment and wages (16 Jan 18:00 AEDT) – on wages, the consensus is we see Average Weekly Earnings 3M/YoY moderate a touch to 6.8% (from 7.2%). The outcome will play into UK rates pricing, where the first 25bp cut is priced for May. GBPUSD seems to be finding good supply into 1.2800, so the GBP bulls will want to see a closing break here to add to longs. Favour EURGBP into 0.8560.

China Q4 GDP (17 Jan 13:00) – the economist’s median estimate has Q4 GDP growing 1% QoQ and 5.2% YoY (from 4.9% in Q3) – GDP by its nature is a backwards-looking data point but given the lack of confidence international money managers have in investing in China, I think the outcome of the China GDP report could impact market volatility.

China industrial production, fixed asset investment, retail sales, property sales (17 Jan 13:00) – the market looks for these data points to come in at 4.5%, 2.9%, 8% and -9.5% respectively. Certainly, the market will be closely watching the property sales data for further evidence that sales are troughing.

UK CPI (17 Jan 18:00 AEDT) – a potential vol event for GBP traders, so monitor exposures over the data point - the market sees headline CPI coming in at 3.8% yoy (from 3.9%) and core CPI at 4.9% (5.1%). GBPUSD 1-week implied volatility sits at 6.67% (the 17th percentile of the 12-month range), and pricing a -/+ 105-pip move from Friday’s closing level.

US retail sales (18 Jan 00:30 AEDT) – the median consensus is we see sales growing 0.4% mom, with the ‘control group’ element at 0.2%. The market picks and chooses to run with this data point, but I think a mom decline – should it come - could impact sentiment and promote good USD sellers.

Aussie employment report (18 Jan 11:30 AEDT) – the median estimate is we see 15k jobs created, with the U/E rate unchanged at 3.9%. Aussie interest rate futures price the June RBA meeting as the probable first cut, so this pricing may come into question, but it would take a move in the unemployment rate to do so.

Japan national CPI (19 Jan 10:30 AEDT) – the market looks for JP headline CPI to moderate to 2.6% (from 2.8%) and core CPI to print 3.7% (3.8%). After last week’s -3% decline in real wages, and falling inflation in Japan, coming at a time when other G10 central are expected to start a cutting cycle, it hardly incentivises the BoJ to lift rates.

Fed speakers – Waller (17/1 03:00 AEDT), Williams, Bostic, Daly

Other factors that could affect market sentiment:

US Corp earnings – It’s a quiet week on the US earnings front with c3% of the US500 market cap report - Goldman Sachs and Morgan Stanley garner attention, while we see several regional banks out with numbers, so put the KRE ETF on the radar.

US politics – On Monday we get the results from the Iowa Caucuses – Trump is almost certain to win the REP nomination, but could Nikki Haley gain some momentum to take into the New Hampshire Primary on 23 January?

US options expiry – US equity index expiry (16 Jan), VIX options expiry (17 Jan), equity options expiry (19 Jan).

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.