- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

Analysis

News that Congress had miraculously pushed out the govt. shutdown for 45 days should be welcomed by risky assets and there is modest gapping risk for the open. Perhaps cynically, the agreement highlights that the US political system is not always completely inept. Also, while we revisit the saga in mid-November, a protracted shutdown, when considered in combination with auto strikes, and student loan repayments would have been the trigger to negatively impact US Q4 GDP and that may have led to some de-risking.

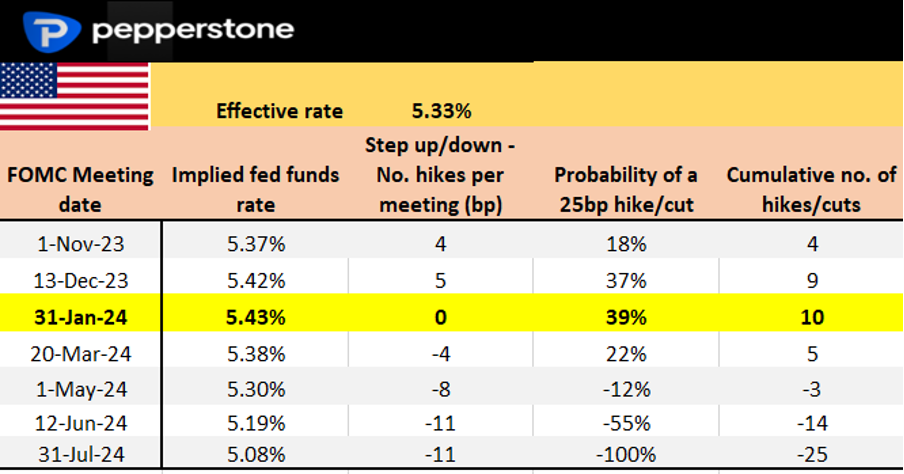

We also now have a firm understanding that the US Labor Department will release nonfarm payrolls data this Friday, as well as the US CPI report (on 12 Oct), which may have not been the case had the govt. shutdown. This puts the 1 November FOMC meeting back on the table as a potential venue for a further 25bp rate hike.

With US swaps pricing just 4bp of hikes for the 1 Nov FOMC meeting, one could argue the market had discounted the idea the Fed wasn’t going to be privy to this important data to make an informed call on a November hike. We should see these rate hike expectations lift a touch.

Profit taking (in USD longs) aside, one asks where else would you park your capital in G10 FX? The AUD and NZD have stood up of late, but this will take a far better tone on China, and with the Chinese capital markets closed this week for Golden Week that may be an early call. The weekend China PMIs, with manufacturing moving into expansion for the first time since March, will certainly offer a tailwind for these China proxies.

However, once again the markets will likely be held hostage by the direction of US bond yields, USD exceptionalism and positioning.

Tactically, I like crude to consolidate here below $96, and with it CAD and NOK trades should also lack momentum. Gold is at the mercy of the USD and real rates, but after a huge down week, the bulls will be looking at buy limits into $1810 and hoping for a bit more of a flush out. While price has closed below 4329 support, the US500 holds channel support and I’m warming to longs for 4400/50, with a stop below 4230.

Let's see what October brings, but it's encouraging that we’ve seen a pulse in the markets of late.

The marquee event risks to navigate this week:

US nonfarm payrolls (6 Oct 23:30 AEDT) – With Congress miraculously averting a government shutdown US nonfarm payrolls (NFP) becomes a risk event for traders to manage. The consensus for NFP is 165k jobs (the economist’s range sits between 250k to 105k), which would be modestly above the 3-month average of 150k jobs. The U/E rate eyed is expected to tick down to 3.7%, although the participation rate will again play a role in that outcome. Average Hourly Earnings (AHE) are expected at 4.3% YoY/0.3% MoM. Simplistically, a NF payrolls print below 140k should see the USD under pressure – above 200k, should see USD buyers, although the extent of the move will be determined by AHEs and the U/E rate.

US swaps pricing per meeting

US ADP payrolls (4 Oct 23:15 AEDT) – the consensus sits at 150k jobs in the ADP payrolls report (from 177k in August), with the economist’s range of estimates set between 228k and 102k. The market typically responds to the ADP report when we see an outsized beat to consensus (such as we saw in the July and May prints), but with NFP back in play as the highlight this week the ADP report gets somewhat less focus.

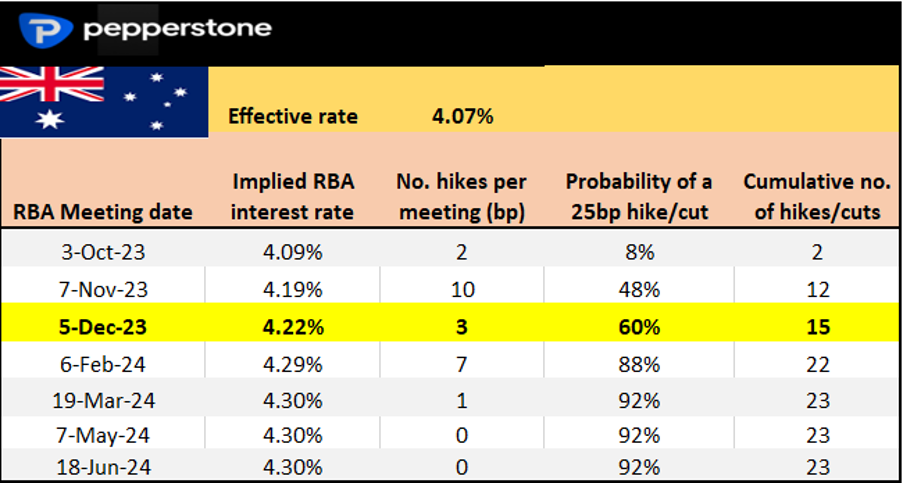

RBA meeting (3 Oct 14:30 AEDT) – it would be a huge surprise if the RBA hiked rates at this meeting and we see interest rate futures placing a lowly 8% chance they lift to 4.35%. More importantly, we see 12bp of hikes priced – a 50% probability - for the November meeting, so the market will marry the RBA’s statement and the guidance for rates against that pricing. A hawkish hold seems the likely outcome here, with modest AUD upside risks at RBA gov Bullock's first meeting at the helm. AUDCHF has been a momentum beast rallying in 11 of the past 12 days – happy to hold longs until price closes below the 8-day EMA.

AUD rates pricing per meeting

RBNZ meeting (4 Oct 12:00 AEDT) – The RBNZ will almost certainly hold rates at 5.5%, but like RBA, market expectations have swung to a 50% chance of a hike in the November RBNZ meeting. Commentary and guidance that suggests they retain the optionality to hike again could drive the NZD. NZDCAD longs look interesting, having broken the 0.8100 to 0.7950 consolidation range – can this kick higher?

US services ISM (5 Oct 01:00 AEDT) – we should see some cooling in the services index, with the consensus at 53.5 (vs 54.5 in August) – 53.5 would still be a healthy level of growth in services and reinforce the US exceptionalism trade. Would expect a solid USD sell-off on a print around/below 50, and an outsized rally above 55.0.

US ISM manufacturing (3 Oct 01:00 AEDT) – the consensus view is we see the diffusion index coming in at 47.9, which would be another contraction, but a modest improvement from the August print of 47.6. A number below 45 would be a shock and could see USD longs look to reduce, likely taking the DXY towards Friday’s low of 105.65. A print above 50.0 would also be a surprise and likely spur a renewed leg higher in the USD, where we should see USDJPY into 150

US JOLTS job openings (4 Oct 01:00 AEDT) – The market looks for 8.83m job openings in August (from 8.827m). Consolidation in job openings after a strong decline from 12m openings in March 2022 seems highly probable.

UK Decision Makers Panel (5 Oct 19:30 AEDT) – the market eyes 3-month (inflation) output prices 20bp lower from the last call at 4.7% and 1-year price expectations to fall to 4.6%. GBP swaps pricing holds 19bp of hikes priced by Feb 2024, so a downside outcome to the DMP outlook could reduce market rate expectations and further weigh on GBP. I personally can’t help but sit in the camp where the BoE are done hiking. GBPAUD and GBPNZD downside looks attractive, even though both pairs have been sold hard through September.

UK Global/CIPS services PMI (4 Oct 19:30 AEDT) – this is a final read in the UK September services PMI release, although the market is not looking for a revision from the announced 47.2 print for the diffusion index. GBPUSD holds a regression channel (drawn from the 13 July high) – for momentum accounts, sell-stop orders through 1.2180 make sense.

Canada employment report (6 Oct 23:30 AEDT) – with one eye on crude, CAD traders will be looking at FX exposures over the Canadian job report. Leveraged funds hold a sizeable CAD long position and they will be ‘hoping’ for a blowout jobs report to put a rate hike (at the 25 Oct BoC meeting) in play, where the swaps market places a 28% chance of a hike at this meeting, and a 56% chance of a hike at the December meeting - the jobs data could influence market expectations, as it would the CAD. The consensus is we see 20k jobs created in September, with the unemployment rate expected to tick up to 5.6%.

Korea exports (1 Oct 11:00 AEDT) – expectations of a 9.3% decline in Korean exports in September will be monitored, especially for signs of trade flows to China. USDKRW has been a strong momentum long and as we see has broken out to YTD highs – can this kick? Weak export data could see further USD upside in this pair.

- Powell & Harker (3 Oct 02:00 AEST), Williams, Mester, Bostic, Bowman, Goolsbee, Mester, Daly

- Catherine Mann, Broadbent

- ECB speakers – 16 speeches this week.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.