Earnings season will soon be upon us once more and, while conflict in the Middle East continues to pre-occupy market participants for the most part, corporate commentary and guidance will nonetheless prove instructive, both in terms of how firms are dealing with increased cost pressures, and how consumer demand is holding up amid heightened uncertainty.

Expectations

Per FactSet, S&P 500 earnings growth is seen at 13.2% YoY in the first quarter which, if delivered, would mark the sixth consecutive quarterly rise. Nine of the index’s eleven sectors are seen notching an annual rise in earnings growth, with the Information Technology sector seen leading, and Healthcare lagging.

From a revenue perspective, the index is seen notching growth of 9.7% YoY, marking not only a 22nd consecutive quarter of growth, but also the best quarter since Q3 22, if delivered. All eleven GICS sectors are set to report annual revenue growth, again led by the Information Technology sector.

As for valuations, the recent sell-off since the outbreak of conflict in the Middle East has seen the S&P 500 cheapen, with the forward 12-month P/E now sitting at 19.8, below the 5-year average of 19.9, and down from 22.0 at the end of last year.. Still, historically speaking, it wouldn’t be fair to describe the index as ‘cheap’, given that we remain considerable north of the 10-year average 18.9.

Factors To Watch

First things first, it’s important to remember that the earnings themselves that will be released through reporting season are already somewhat stale. The macroeconomic outlook has flipped almost totally on its head since the start of March, as a result of conflict having broken out in the Middle East, in turn triggering a surge in energy prices. Naturally, this will bring with it not only inflationary implications, but likely also a significant negative demand shock, particularly if higher energy prices prove more prolonged than expected.

On that note, guidance issued by corporates over the upcoming reporting season will be pivotal, as participants are highly likely to focus much more on the near-term outlook, than they are on figures that reflect a period very different from the present economic reality. Specifically, comments around how firms are likely to deal with significant input cost pressures, as well as how corporates see consumer demand evolving in the months ahead. On these points, comments from Consumer Discretionary names are likely to be particularly instructive. Comments from ‘Big Oil’ stocks are also going to be of interest, especially in terms of how long it may take for commodity flows, and hence prices, to normalise.

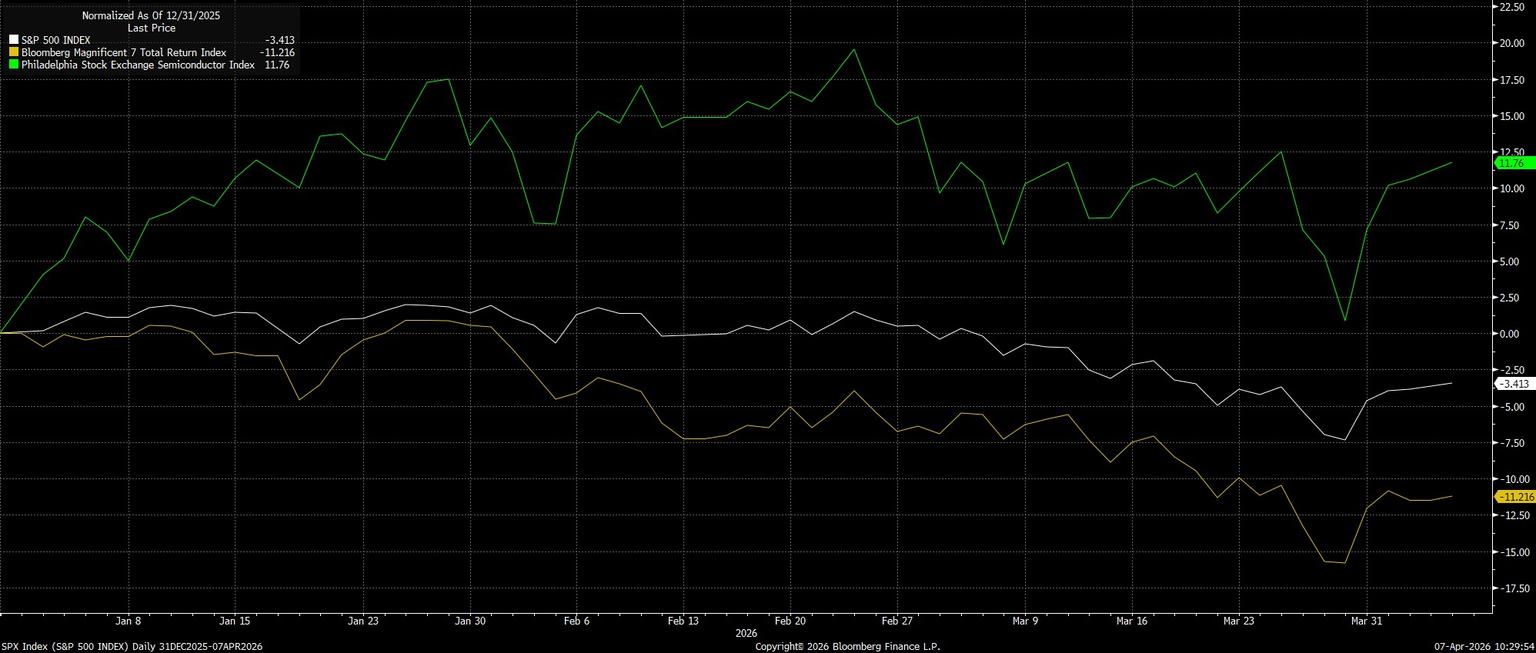

There will also be considerable interest in guidance issued by the ‘hyperscalers’, as well as by semiconductor names, and the ‘magnificent seven’ at large. While market attention has focused almost entirely on geopolitics of late, jitters over the broader AI theme haven’t gone away, whether they pertain to potential negative labour impacts from AI agents substituting for workers, or whether it be concerns over the increasingly circular nature by which deals in the space are being financed. Key for investors here will be guidance issued moving forwards, particularly in terms of capex for the coming quarters, with there being no sign of spending in the AI ‘arms race’ slowing any time soon.

Market Implications

Taking a step back, for markets at large, a solid earnings season, in line with, or exceeding, the consensus expectations outlined above, would underscore what remains a robust fundamental bull case, which continues to comprise solid earnings growth, a looser monetary & fiscal stance, as well as a relatively robust US economy.

That said, market participants may have some difficulty in mustering up the conviction to ‘buy the dip’ no matter what earnings season may bring, so long as geopolitical noise remains deafening. As such, with a degree of caution likely to prevail unless and until concrete steps towards de-escalation are taken in the Middle East, earnings season is probably best viewed as laying the foundations for a more durable rally once the war comes to an end, as opposed to being an overt positive catalyst in the ‘here and now’.