- English (UK)

Gorton & Denton By-Election In Focus

Thursday sees a pivotal by-election taking place in Gorton & Denton, a constituency which has traditionally been a safe Labour seat, but where both the Green Party, and Reform have a real chance of causing an upset. Of course, such an upset couldn't come at a more inopportune time for PM Starmer, whose premiership is already hanging by a thread after the Mandelson affair a fortnight ago, and ahead of local elections being held across the UK in May.

Risks To Starmer’s Leadership Are Numerous

Clearly, the best result for Starmer would be a Labour victory in the by-election, likely giving the PM some ‘breathing space’ to muddle through until those local elections. On this front, the stakes could not be higher, with the PM having not only recently visited the constituency (very rare for a by-election), but with Starmer’s allies on the Labour NEC having also blocked Manchester Mayor, and potential leadership contender, Andy Burnham from standing in the seat. To handpick a candidate, then campaign personally for said candidate, only to lose the seat, would at the very least be highly embarrassing, while again calling Starmer’s political judgement and nous into question.

Were Labour to lose the seat, it matters less in the grand scheme of things who voters send to Westminster, and more where Labour end up placing, with there being a major risk of Labour coming third behind the Greens and Reform. In a constituency where a Labour MP has been returned in every election since 1935, this would again be a political wound Starmer may find it highly difficult to recover from, thus further raising the likelihood of a leadership challenge at some stage this year.

My base case remains that such a challenge is most likely to come after the May local elections, with any potential successor likely wanting Starmer to ‘own’ those results, before positioning themselves as the solution to turning around the party’s electoral fortunes.

Market Implications

For UK markets, there are two implications here.

The first is that political uncertainty is highly unlikely to dissipate any time soon, as internal Labour manoeuvring continues, and the potential for a probably messy leadership contest increases. The second is that the fiscal outlook is likely to remain incredibly cloudy, with any potential successor almost certain to run on a much more left-wing fiscal platform, in order to appeal to Labour members, with a new Chancellor likely to tear up Reeves’s fiscal rules as one of their first acts in office.

Consequently, all roads seem to still lead towards a steeper Gilt curve from here on in.

The front-end should remain relatively well-anchored, with there potentially even being some room for further gains, as disinflation becomes increasingly embedded within the economy, and a greater margin of labour market slack continues to emerge, allowing the BoE to take Bank Rate towards a neutral level, around 3%, by the end of summer. However, at the same time, mounting fiscal and political risks should not only result in gains at the long-end being capped in the near-term, but also pose notable downside risks once a leadership campaign gets underway in earnest in the spring.

_10_2026-02-25_09-06-29.jpg)

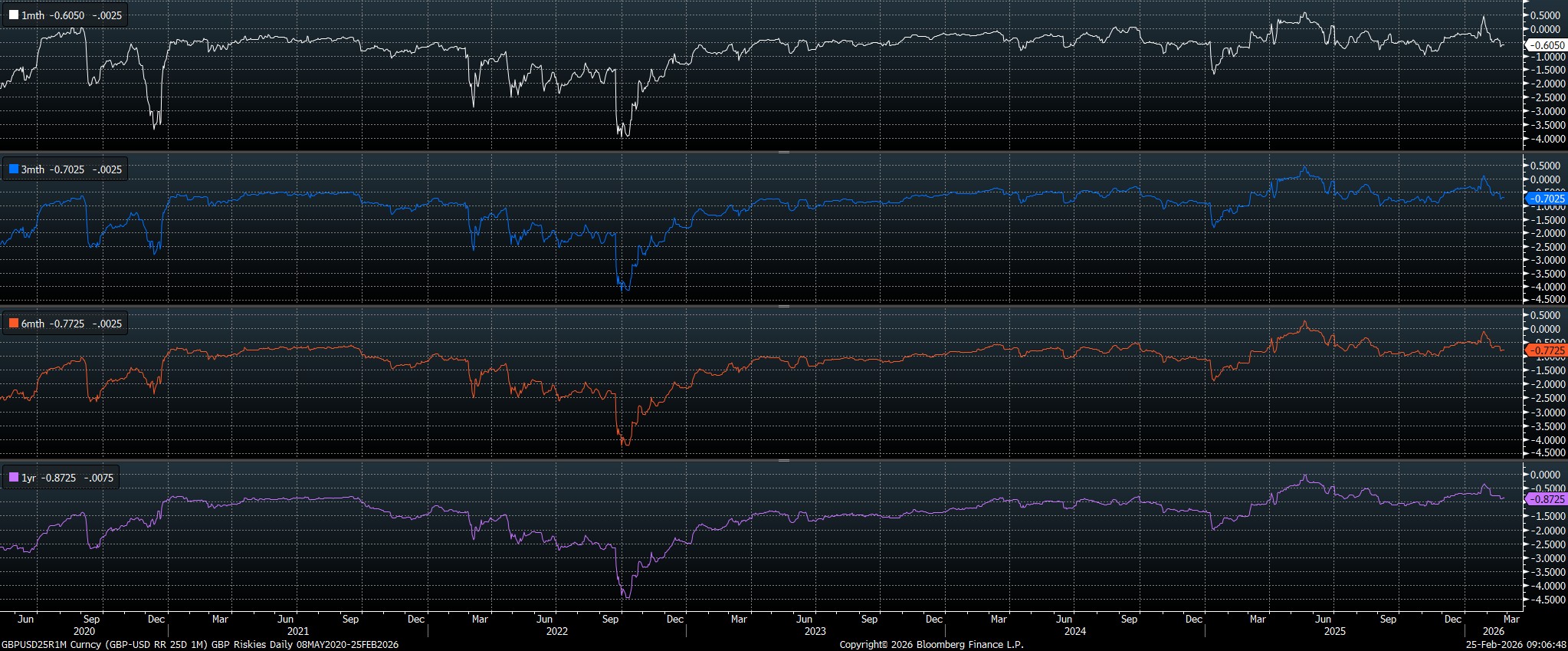

As for the pound, those same downside risks also dominate the near- and medium-term outlooks, though it must be said that sentiment towards sterling is already relatively soft, with cable risk reversals across a host of tenors trading at their most negative since mid-November last year.

In fact, given the relatively dour sentiment towards the US at present, amid ongoing policy volatility in Washington DC, any GBP weakness may well be more likely to emerge in the crosses, though the 8750 level in EUR/GBP is proving an incredibly tough nut to crack for the time being.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.