- English (UK)

Summary

- Polling Day Looms: 7th May marks the biggest set of UK elections since the general election in 2024, amid local elections in England, and elections to devolved parliaments in both Scotland & Wales

- Expectations: Polling points to the likelihood of substantial gains for the Greens and Reform in England, while both Labour and the Conservatives will likely lose hundreds of council seats

- Downside Risks For UK Assets: After polling day, focus will turn to PM Starmer's future, with any Labour leadership challenge posing substantial downside risks for both the GBP, and Gilts

Britain Heads To The Ballot Box

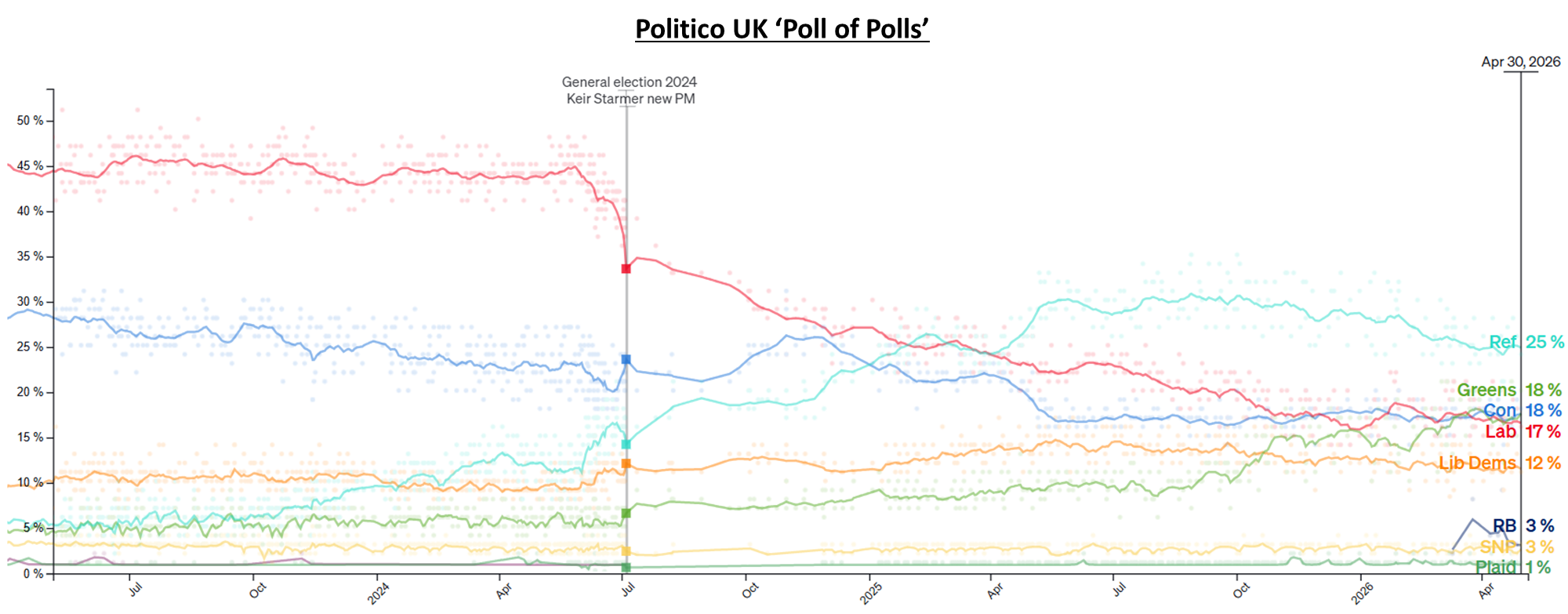

Political events are back in focus once again here in Blighty, as the nation prepares to go to the ballot box in what will mark the biggest set of elections since the 2024 general election. The local elections come amid a backdrop of increased dissatisfaction with PM Starmer, both within and without the ruling Labour Party, and at a time when support for both Reform, and the Green Party, continues to rise.

In England, voters will elect around 5,000 councillors in 136 different local councils, with a handful of mayoral elections in the mix as well. Meanwhile, north of the border, elections will also be held for all 129 MSPs in the Scottish Parliament, while elections will also take place for 96 representatives in a reformed Senedd (the Welsh Parliament), which is being expanded from 60 seats in the biggest shake-up to the body since it was formed in the late-90s.

Expectations

While one cannot directly translate national voting intention polling into a potential local election result, given the idiosyncratic issues that often factor into voting decisions in such a poll, they nonetheless provide some degree of steer, and allow us to work out a base case for the upcoming vote.

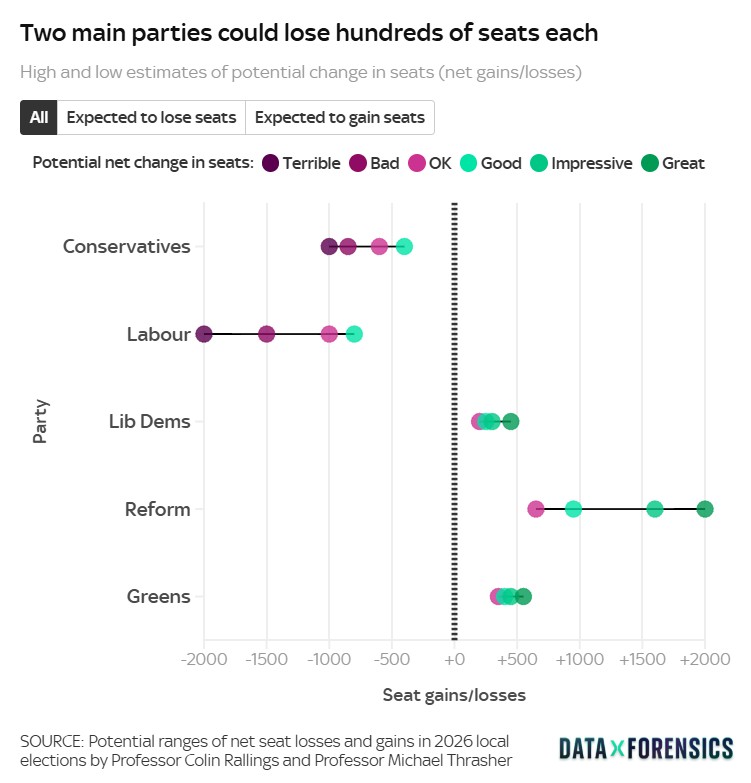

The working assumption must be that the upcoming local elections in England will see a significant surge in support not only for Reform, but also for the Green party, with projections indicating that the former could gain over 1,000 council seats, and the latter may gain around 500 seats. In direct contrast, both Labour and the Conservatives are likely to experience steep losses, more so for the former, where some modelling points to the potential loss of between 1,500 and 2,000 council seats.

An important factor to note, though, is that due to the UK’s ‘first past the post’ voting system, these seats could well be flipped on very low vote shares – i.e., it is possible, and highly likely, for a candidate to win a seat, without winning a majority of votes in their seat; put simply, the candidate with the highest number of votes in a constituency, is the one who wins, regardless of their precise level of support. As the political landscape becomes increasingly fragmented, FPTP produces increasingly disproportionate results, something that is highly likely to also be a factor at the next general election, whenever that may come.

Outside of England, opinion polling points to a comfortable victory for the SNP in Scotland, albeit one that may not be sizeable enough for the party to obtain an outright majority. In Wales, opinion polls put Reform and Plaid Cymru roughly neck-and-neck, with the majority of modelled seat projections pointing to a hung parliament being the likely result. That said, if the SNP were to govern in Scotland, and Plaid to govern in Wales, this would, along with Sinn Fein in Northern Ireland, mean that for the first time the largest party in each of the devolved administrations would advocate for independence from the UK.

Assessing The Results

In contrast to a general election, local election results typically take considerably longer to be published, with many councils not even beginning to count until the Friday morning following polling day. Added to which, there is no nationwide exit poll the moment that polls close, as we have become accustomed to on election night.

With this in mind, it likely won’t be until mid- to late-afternoon on Friday until the full results of the local elections become clear, with some counts likely even to drag on into Saturday as well, particularly in some London boroughs.

Once the results have become clear, particularly in terms of the scale of what seems an inevitably significant defeat for the Labour Party, attention will very quickly turn to the Sunday newspapers, for any signs of MPs beginning to call PM Starmer’s future into question.

Political Fallout

Speaking of which, the PM’s future will be the primary, if not only, issue that financial markets and the ‘Westminster bubble’ are likely to focus on in the aftermath of election day.

Dissatisfaction with Starmer among Labour MPs has been growing for some time now, not only as a result of a seemingly-endless series of policy U-turns, but also as the party flounders in opinion polls, and seems to have no broader political direction at all. Added to which, the PM’s personal judgement has increasingly been called into question in recent months, not least in the aftermath of the scandal surrounding the appointment of Peter Mandelson as US Ambassador.

Many, including me, have been working on the assumption that a Labour leadership challenge is likely in the aftermath of 7th May. It is logical that not only would a prospective leader want the current leader to ‘own’ a disaster at the ballot box, but also that such a disaster would be a logical catalyst for those seeking a change to ‘strike while the iron’s hot’.

With that in mind, comments from those thought to be in the running to replace Starmer, including Health Sec. Streeting, Energy Sec. Miliband, and former Deputy PM Rayner, as well as their surrogates, will be worth watching very closely indeed in the aftermath of polling day. Manchester Mayor Burnham, despite having been talked of as a potential leadership challenger, is at present not an MP, hence would not be eligible to stand in any contest.

Market Implications

The best-case outcome from the local elections for UK assets would be a relatively contained Labour defeat, which allows PM Starmer to stumble on for a short while longer. Though such a scenario may lead to a relief rally in the GBP and in Gilts, any such move is likely to prove relatively short-lived, considering that the present political inertia will likely continue. In fact, for markets, under this scenario, the question would likely rather quickly become one of when sticking with Starmer, and a Government that is struggling to govern, is a worse outcome than changing leader?

That said, markets in the here and now are likely to react adversely to the prospect of a Labour leadership challenge, and the ousting of PM Starmer, for a couple of reasons.

Firstly, as we all know, markets hate any sort of uncertainty, especially in the political realm, and particularly with the UK having endured more than its fair share of Westminster upheaval in recent years, having already had six different Prime Ministers in the last decade. Clearly, an uncertain political backdrop not only makes it considerably harder for market participants to accurately discount the future policy path, but is also likely to lead to corporates delaying hiring and investment decisions, in turn posing a headwind to economic growth at large.

Secondly, while a leadership challenge would be a drawn out and uncertain process, it’s overwhelmingly likely that such a challenge would ultimately result in whoever the new leader is replacing Chancellor Reeves with their own choice. Although market participants have, generally, taken something of a dim view of Reeves’s endless ‘tax and spend’ policies, the prevailing opinion remains that Reeves is the ‘least bad’ option among Labour MPs, accounting for her adherence to strict fiscal rules. Any replacement for Reeves is not only likely to tear up those rules, but also to embark on a much looser fiscal stance, considerably increasing government spending, public borrowing, and running an even-larger budget deficit. Any tax hikes announced to fund those measures would at this stage be counter-productive, with the tax burden already on its way to a record high.

Combined, then, UK assets would have to deal with a rather grim combination of near-term political uncertainty, coupled with relative certainty of a further fiscal deterioration over the medium-term. This, quite clearly, poses substantial downside risks to the GBP, as well as to long-end Gilts, which are already on very fragile ground indeed, with the benchmark 10-year yield trading north of 5%, and the 10yr UK-US spread having recently printed new cycle wides at 66bp.

_10_2026-05-05_10-29-48.jpg)

Returning to polling day itself, and the immediate aftermath, a GBP/USD straddle expiring next Monday prices a move of around +/-0.9% (to 1 standard deviation of confidence), while a comparable long Gilt option implies a move of approx. +/-13bp – both of these, to me, seem a little conservative.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.