U.S. banks closed 2025 on a high note, with large players delivering robust performances despite a volatile macro backdrop. A year of still-elevated interest rates, resilient consumer spending, and buoyant asset prices fueled record earnings across Wall Street, with all six major banks reporting positive year-on-year growth in adjusted EPS.

However, concerns over Trump’s proposed 10% cap on credit card interest rates have persisted, leading to some divergence in bank stock performance following the earnings releases.

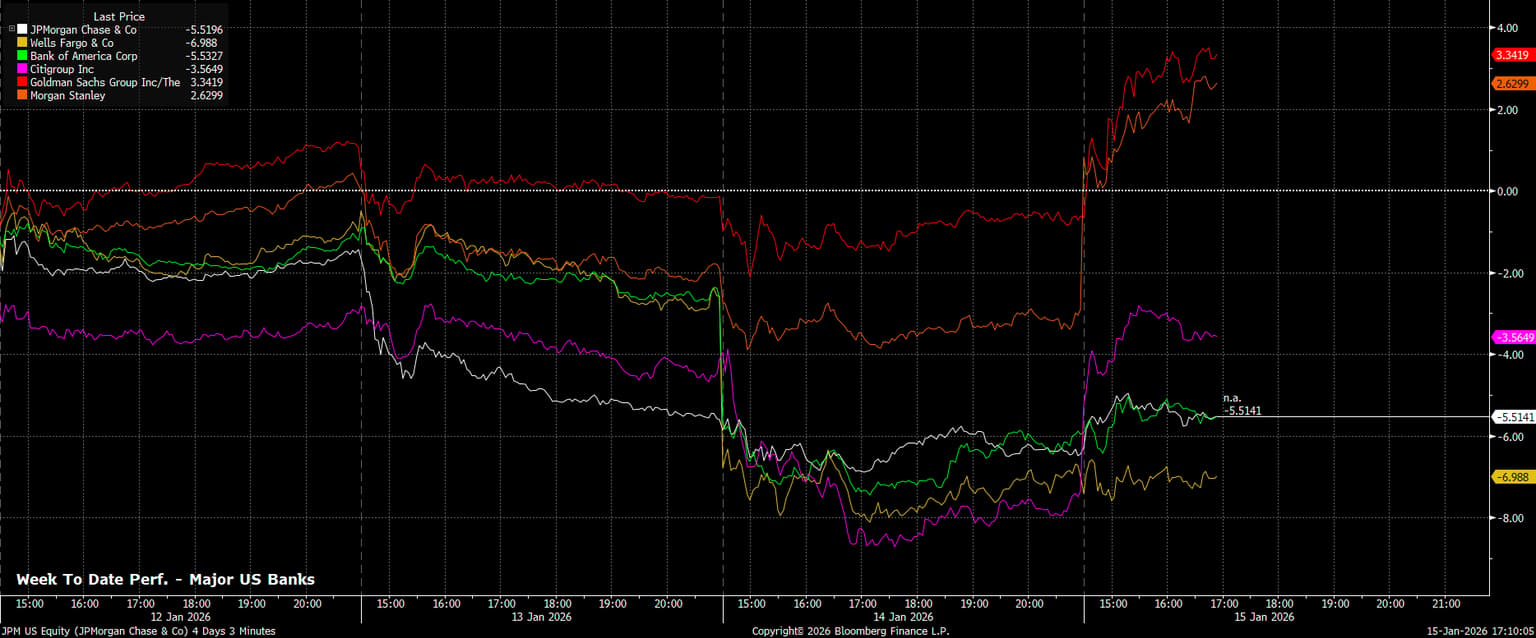

Divergent Performances Among Big Banks

Goldman Sachs and Morgan Stanley, less exposed to retail banking, led the pack, with Goldman notably posting $4.31 billion in quarterly equities trading revenue—a Wall Street record surpassing its own prior milestone. This underscores the continuing strength of investment banking and trading as profit engines, particularly when retail exposure carries additional regulatory and policy risk.

Traditional banking giants also delivered solid results, though with nuanced differences. Wells Fargo reported Q4 net income of $5.4 billion, up 13% year-on-year, supported by stable credit quality and disciplined cost management. More importantly, the removal of Fed-imposed asset caps and lifted consent orders now positions the bank to expand its balance sheet and pursue growth without regulatory constraints.

Wells Fargo’s $23 billion in shareholder returns and revised medium-term profitability targets signal confidence in a post-restructuring era.

Bank of America similarly posted a strong quarter, with net income of $7.6 billion, up 18% from last year. Revenue growth of 7% was driven by higher lending margins, expanding balance sheets, and a striking 23% increase in equities trading fees. Consumer banking and wealth management remained solid, reflecting both affluent client activity and resilient underlying demand.

Citigroup, while posting $2.5 billion in net income, missed forecasts partly due to a $1.2 billion loss from the forthcoming sale of its Russia unit. Nevertheless, its record revenues and operating leverage across multiple lines reflect underlying operational resilience, even amid announced layoffs as part of a broader restructuring.

Resilience and Strategic Focus Amid Policy Uncertainty

Overall, Q4 2025 earnings underscore the resilience of the U.S. banking sector. Profits are strong, shareholder returns substantial, and management teams are well-positioned to capitalize on opportunities in 2026.

Despite the uncertainty surrounding the proposed cap on credit card interest rates—which could tighten credit access for higher-risk borrowers, limit consumer spending, and challenge banks’ profitability—banks remain focused on their core strengths: maintaining operational efficiency, returning capital to shareholders, and leveraging strategic flexibility to expand their balance sheets.

This disciplined management approach, combined with diversified revenue streams, provides a solid foundation for sustainable long-term profitability.

.png?format=pjpg&auto=webp&width=1536&quality=75&branch=main)