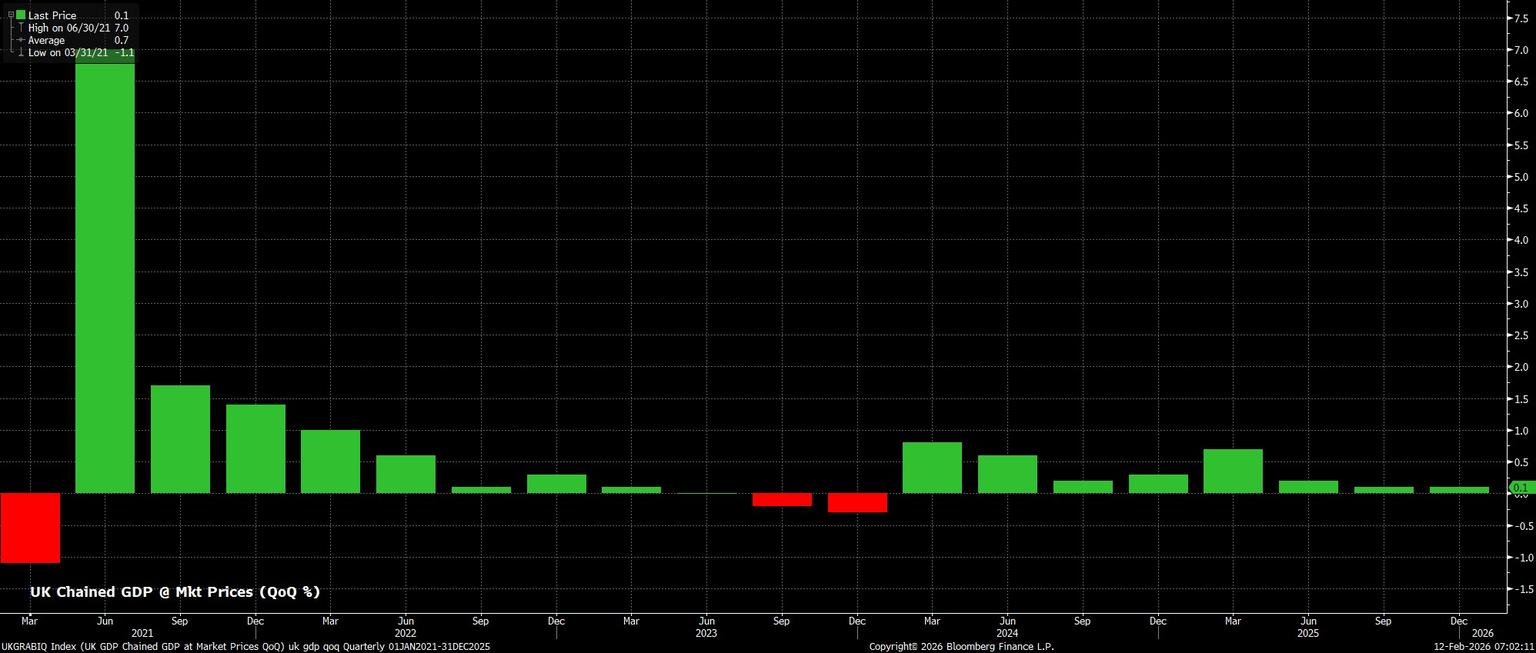

The economy grew by 0.1% QoQ in the final three months of 2025, below the 0.2% pace that both markets and the Bank of England had expected. Furthermore, such a pace of expansion is still very anaemic by any reasonable measure, and underscores how the UK economy's performance has now been subpar for some considerable time - quarterly growth hasn't been more than 0.5% QoQ for a year, and hasn't been above 1% QoQ since the beginning of 2022.

One must also consider that a significant chunk of the rebound in economic activity in the fourth quarter was mechanical in nature, owing largely to the resumption of auto production at Jaguar Land Rover, which had been impacted by a significant cyber-attack in Q3. In addition, risks to the outlook continue to tilt firmly to the downside, not only amid the fragile nature of growth at present, but also considering that political uncertainty is on the rise once more, as evidenced by this week's pantomime in Westminster. Said uncertainty threatens to put the brakes on any momentum that recent 'soft' data, such as January's PMI surveys, may have been pointing towards.

In any case, the Q4 GDP data shan't materially alter the BoE policy outlook. After delivering a triple-whammy of dovishness last week - in the form of a super-tight vote split, dovish guidance, and forecasts pencilling in a return to the 2% inflation target from April onwards - policymakers have laid the groundwork for a rate cut as soon as the next meeting, in mid-March. Delivery of such a cut will require the present gradual disinflation process to continue but, providing it does, further cuts, returning Bank Rate to a neutral level around 3% by the end of summer, remain likely.

That said, it will be developments surrounding the inflation outlook, as well as the degree of labour market slack which emerges, that will be the main determinants of both the timing, and extent, of future rate reductions, as opposed to incoming activity figures.