- English (UK)

Overview

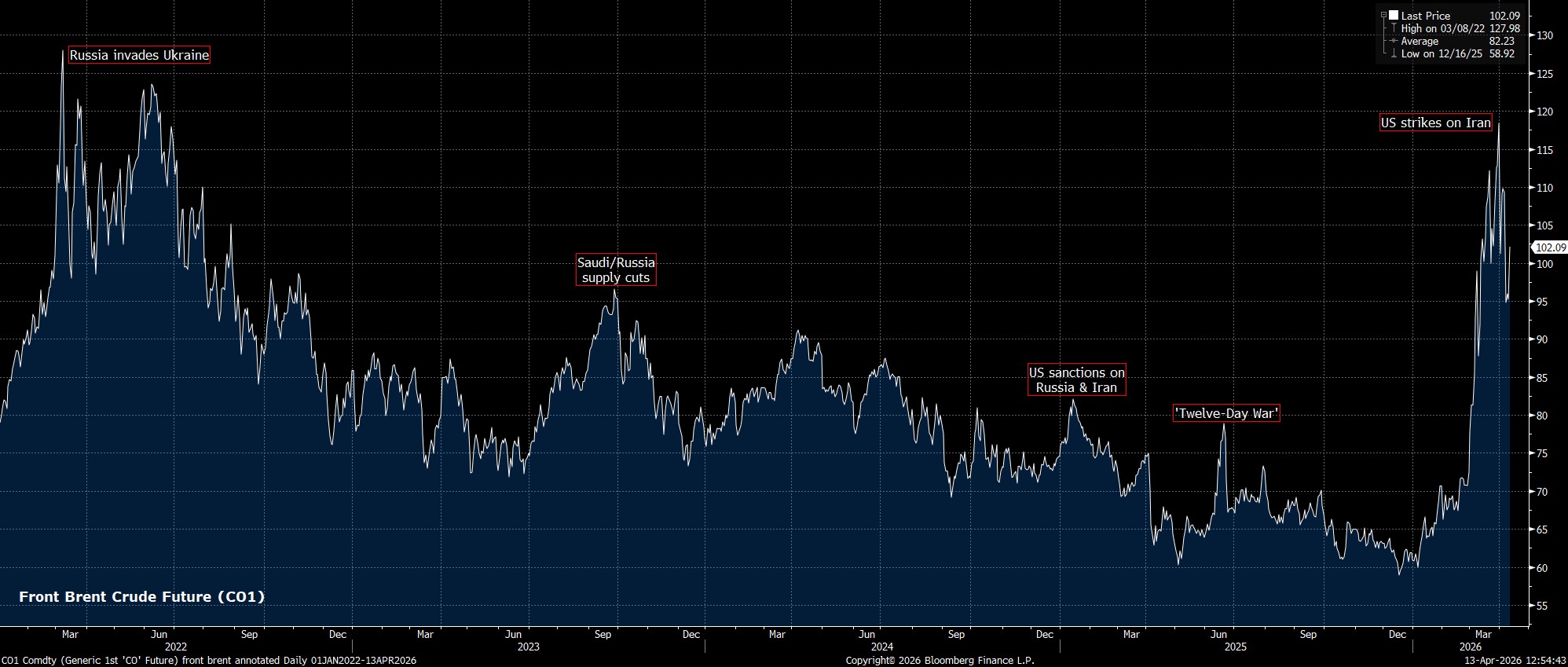

One may make the assumption that higher energy prices automatically leads to improved earnings for the energy sector. While that is true to some extent, the correlation is not necessarily perfect, with the move in Brent benchmarks north of $100bbl not simply being a boon for energy stocks on its own.

There are a couple of factors at play here. Firstly, given the breakneck speed of the recent rally in energy prices, oil majors will likely be forced to take notable paper losses on cargo hedges that were placed earlier in the quarter, before kinetic action in the Middle East begun, thus posing a headwind to earnings at large.

Secondly, while prices have surged, this has been entirely as a result of massive supply disruption, as opposed to an increase in demand. This supply disruption means that majors have, by and large, been unable to capitalise on these higher prices, having instead been forced to lower output considerably, and shut-in production in many cases, due to the effective closure of the Strait of Hormuz, and storage having been filled.

Both Exxon Mobil (XOM) and Chevron (CVX) likely lost as much as 6% of overall production in the first quarter as a result of this latter factor, which has come after just one month of the conflict. Logically, the longer the conflict wears on, and the greater the extent to which production must be cut, the more significant a hit to earnings that is likely to result.

Guidance In Focus

In many respects, however, these factors are priced in, not least considering Exxon having taken the extraordinary step of issuing pre-earnings guidance last week, ahead of the likely reporting date at the start of May.

As a result, focus for market participants is set to fall primarily on the guidance that oil majors issue for coming quarters. Over the longer-run, higher energy prices should be a positive catalyst for the sector, providing that production can be resumed, and more regular supply conditions prevail. In fact, numerous factors spring to mind that could keep energy prices underpinned for some time, including a structurally higher geopolitical risk premium post-conflict, as well as elevated demand due to a need to refill stockpiles that have been drawn down since war broke out in the Middle East.

On that note, participants will also pay close attention to the extent to which the ongoing conflict has damaged infrastructure in the region, the extent of repairs that may be required, and the timeframe for resuming pre-conflict output levels once the geopolitical situation calms once more.

Exxon Mobil (XOM – likely report BMO 1st May)

With as much as 20% of the firm’s production in the UAE and Qatar, Exxon is likely to have been significantly detrimentally impacted by the aforementioned supply disruptions which, coupled with having taken the unusual step of issuing downbeat pre-earnings guidance in recent weeks, has contributed to around a 15% pullback in XOM shares from the late-March highs.

As for the upcoming earnings report, consensus expectations point to revenue at $79.4bln in Q1 26, down around 4.5% YoY, which is in turn set to drag EPS lower to $1.44, around 18% lower than this time a year ago. Options on the stock price +/-2.4% over the upcoming report at this stage, though that implied move is likely to widen as the earnings date approaches. In any case, XOM has notched a daily decline following 2 of the last 3 quarterly reports, though some may argue that all of the bad news is already priced in, perhaps leaving limited scope for post-earnings downside this time around.

_2026-04-13_12-49-18.jpg)

Chevron (CVX – report 1st May, 6:15am ET/11:15am BST)

While Chevron has considerably lower exposure to the Middle East than XOM, with only around 5% of production in the region, this has not prevented the stock from also taking a lurch lower in recent sessions, with almost the entirety of the rally seen in the early days of the Middle East conflict having now been erased.

Still, Chevron remains a top-25 stock by weight in the S&P 500, while also being a constituent of the Dow Jones Industrial Average. Expectations point to CVX delivering revenue of $52.2bln in the first quarter, up almost 10% YoY, though profitability is still set to take a significant hit, with estimated EPS of $1.75 marking a near-20% YoY decline. The stock has rallied on earnings day following three of the last four quarterly updates, with options this time around implying a move of +/-2.2% on the print.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.