- English (UK)

November 2025 UK Inflation: Price Pressures Continue To Fade

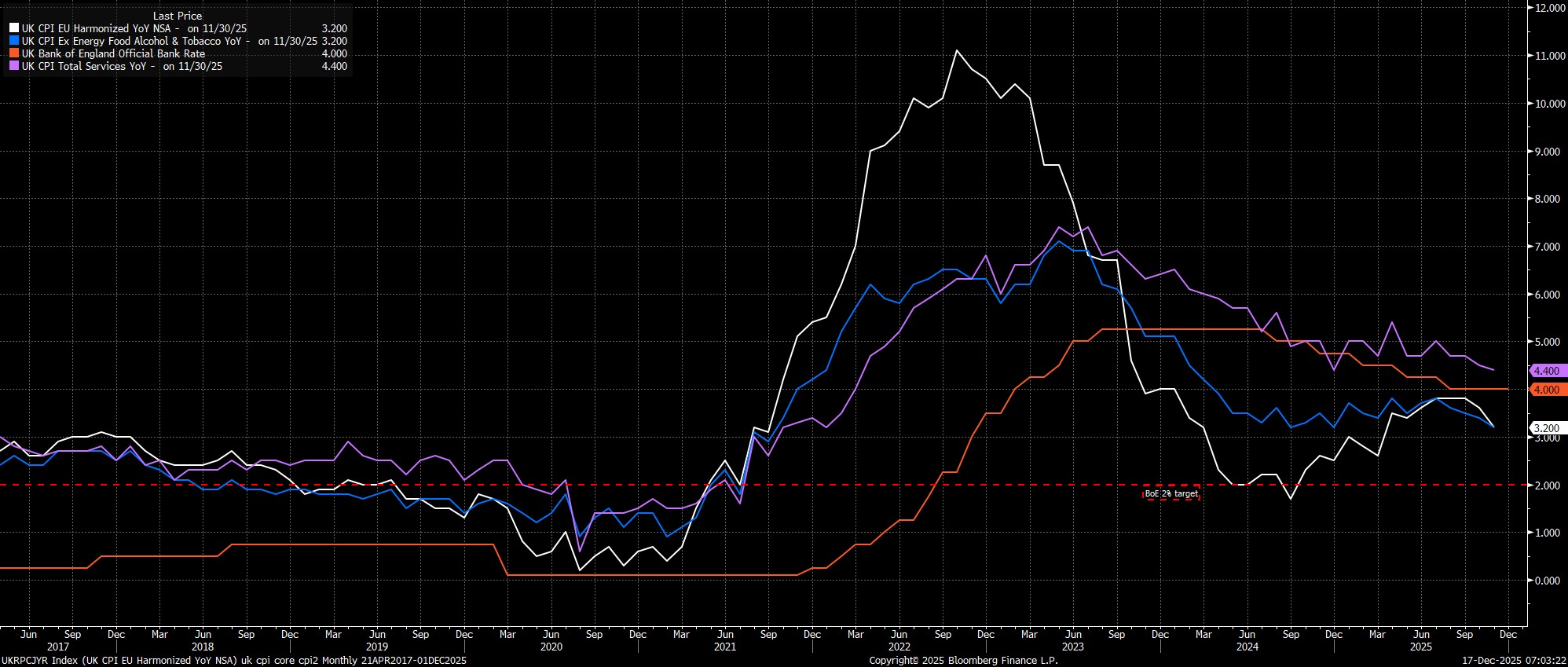

Headline prices rose just 3.2% YoY in November, not only considerably below the BoE's 3.4% forecast, but also the lowest headline inflation rate since March of this year.

Meanwhile, metrics of underlying price pressures pointed to an easing in price pressures, and the subsiding risk of inflation persistence. Core CPI, excluding the volatile food and energy components, rose 3.2% YoY last month, the slowest pace since last December, while services prices rose 4.4% YoY, also the slowest rate since the tail end of last year. Food inflation also remains a key focus for policymakers, given the impact that prices have on inflation expectations at large, and rose by 4.2% YoY last month, a considerable slowdown from the 4.9% YoY pace seen in October.

Overall, the data points to the UK economy having continued to make disinflationary progress as the fourth quarter progressed, with that progress now occurring at a more rapid rate than the BoE had pencilled in. Hence, the MPC remain overwhelmingly likely to deliver another 25bp Bank Rate reduction tomorrow, albeit likely via relatively narrow 6-3 vote among policymakers.

Further rate reductions from here, back towards a more neutral policy rate, remain on the cards, with there being the potential for another rate cut as soon as the February meeting, which may be prompted by a greater easing in labour market conditions, providing that further disinflationary progress, in line with the Bank's forecasts, continues to be made over the winter months.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.