- English (UK)

Rates Unchanged

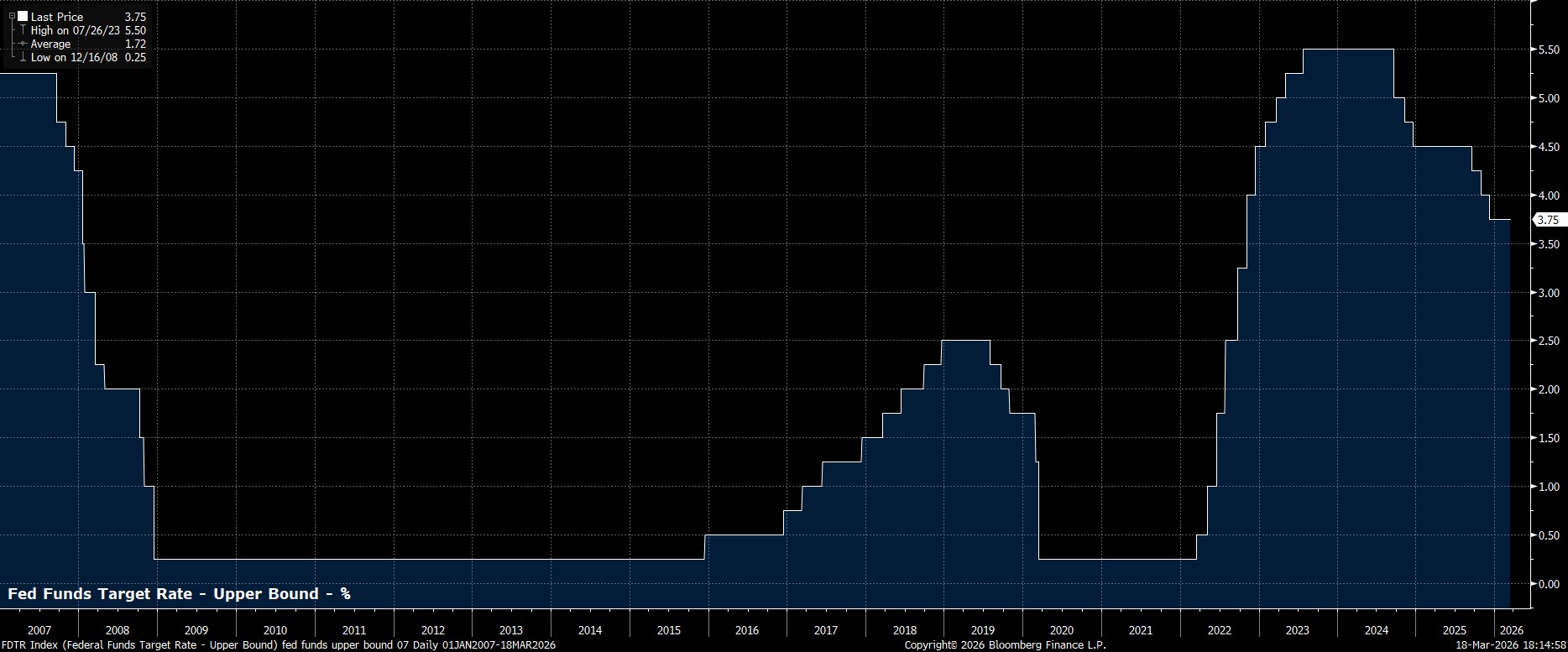

As expected, and bang in line with market pricing, the FOMC maintained the target range for the fed funds rate between 3.50% - 3.75% at the conclusion of the March meeting, extending a ‘pause’ in the easing cycle which began in January, amid an increasingly uncertain economic outlook in light of ongoing conflict in the Middle East, and the subsequent sharp rise in energy prices.

Committee Remains Divided

Despite no policy changes being made, the Committee remained divided as to the appropriate rate path, continuing what is now a long-running theme of disunity among policymakers, with the last unanimous rate decision having been in June 2025.

This time around, however, only Governor Miran dissented in favour of a 25bp rate reduction, in line with his well-known uber-dovish views, as Governor Waller joined the majority once more, reversing his January dovish dissent.

Policy Statement Reflects Uncertain Outlook

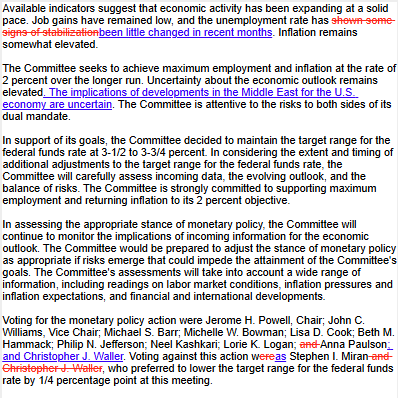

Meanwhile, the accompanying policy statement was tweaked to reflect recent geopolitical events, explicitly noting that the ‘implications of developments in the Middle East for the U.S. economy are uncertain’.

Besides that adjustment, the remainder of the statement was little changed from that issued last time out, with the Committee again noting that job gains have ‘remained low’, that unemployment has ‘been little changed’ of late, and that inflation remains ‘somewhat elevated’.

Revised Projections Have Short Shelf-Life

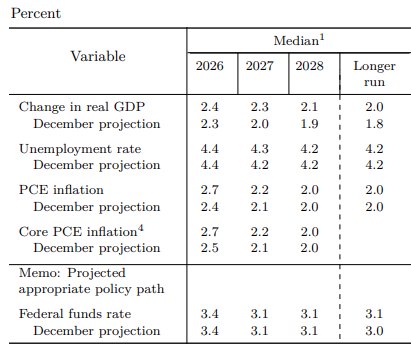

The March confab also brought with it an update to the FOMC’s quarterly Summary of Economic Projections (SEP). It should be noted, though, that the projections are likely to have a very short shelf-life indeed, given the fluid geopolitical environment, while the forecasts are also shrouded in considerably more uncertainty than usual, owing to the same factor.

That said, the updated projections pointed to a modestly higher inflation profile in the short-term, with both headline and core PCE seen at 2.7% this year, up 0.3pp and 0.2pp respectively from the December forecast round, as well as a quicker pace of economic growth both this year and next. Importantly, though, the median unemployment projection was largely unchanged, while both PCE metrics are seen returning to the 2% target by the end of the forecast horizon in 2028.

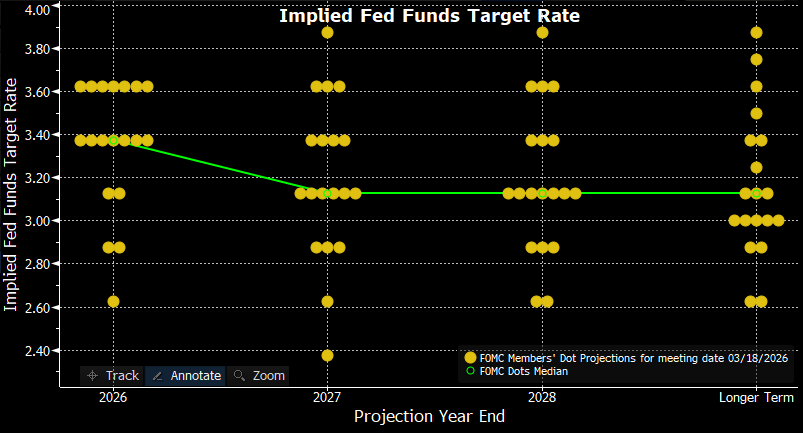

Despite those updated projections, the Committee’s new ‘dot plot’ was little changed from that issued at the end of last year. Consequently, the median dot continues to signal one 25bp cut this year, and in 2027, before rates are held steady, though the ‘longer-run’ dot was nudged higher from 3.00%, to 3.125%, a very minor shift in the grand scheme of things.

As with the forecasts themselves, though, the dots should be taken with a bucketful of salt, given that they tend not to be the most reliable indicator of the policy path at the best of times, and have almost no utility at all at a time as uncertain as this.

Powell Strikes A Noncommittal Tone

Reflecting on this, at his penultimate post-meeting press conference, Chair Powell struck something of a non-committal tone, clearly seeking not to be ‘boxed in’ to any particular policy path. Still, Powell noted that ‘looking-through’ energy price shocks is ‘standard learning’ for central bankers, but that the Fed’s precise response to the energy shock will depend largely on inflation expectations.

Elsewhere, in the presser, Powell was at pains to stress that the Fed ‘don’t know’ what the effects of present Middle East conflict will be, while also noting that the US economy is ‘doing pretty well’ despite prevailing uncertainty.

Finally, Powell offered some long-awaited clarity on his future plans. Powell plans to remain as a Governor at the Fed until the DoJ investigation is “well and truly over”, and that he would serve as ‘Chair Pro Tem’ if Warsh were not confirmed by the Senate in good time. As for once that investigation has concluded, Powell noted that he has not yet made a firm decision regarding his plans.

Conclusion

Zooming out, the overall message from the FOMC right now is one of watching, and waiting, to obtain greater clarity on the macroeconomic backdrop, amid the incredibly fluid geopolitical situation.

For the time being, it seems likely that the Committee will sit on their hands until the magnitude, and duration, of the energy price shock becomes clearer, in order to ensure that inflation expectations remain well-anchored to the 2% target. Still, policy tightening seems off the cards for now, with the Committee likely to look-through the temporary ‘hump’ in price pressures on the back of higher commodity prices, especially given the fragile balance that the labour market is in at the current juncture.

Consequently, rate reductions remain on the cards as the year progresses, once disinflationary progress resumes, and particularly if labour conditions materially worsen. Those cuts, though, of which I still pencil in two 25bp moves by year-end, likely in the second half of the year, once Kevin Warsh is at the helm.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.