The FOMC are set to stand pat at the March meeting, not only in light of having adopted a ‘wait and see’ approach at the first confab of the year, but also as a huge degree of uncertainty clouds the near-term outlook, after the outbreak of conflict in the Middle East, and subsequent energy price shock, which tilts near-term inflation risks to the upside.

Summary

- Standing Pat: The FOMC will hold rates steady at the March meeting, though two or three dovish dissents seem likely

- Forecasts in Focus: Updated projections will likely pencil in higher inflation, and marginally slower growth, in the short-term, though again project a return to the 2% inflation target by the end of the horizon

- Cuts Postponed Not Cancelled: Geopolitical uncertainty, and the ongoing energy shock, lead to cuts being postponed for now, though further easing, under Chair designate Warsh, is likely assuming disinflation resumes in H2 26

Policy On Hold

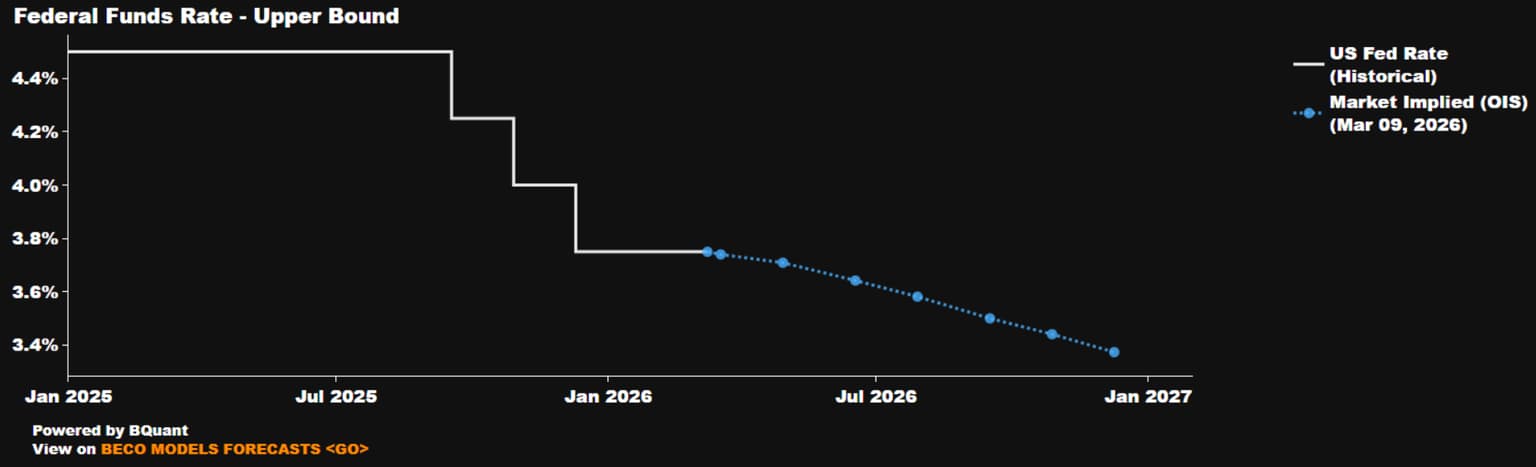

As noted, the FOMC are set to maintain the target range for the fed funds rate at 3.50% - 3.75% at the conclusion of the March meeting. Money markets, per the USD OIS curve, price no chance of any policy action this time out, while also not fully discounting the next 25bp cut until September, largely a function of the recent hawkish repricing on the back of the aforementioned commodity price shock.

The decision to stand pat, however, is unlikely to be a unanimous one.

Governor Miran, in what may be his final meeting at the Fed, is almost certain to dissent in a dovish direction, likely for a 25bp cut, given his view that the labour market requires more policy support, as well as a belief that the oil price shock could exert downwards pressure on core inflation if it were to harm demand. Governor Waller, meanwhile, also seems likely to dissent for such a move, having recently remarked that there is little reason for the Fed to ‘sit on its hands’ if the labour market is weakening, while having also shrugged-off the potential for higher energy prices to lead to sustained inflationary pressures. Governor Bowman has also sounded dovish in recent remarks, noting her preference for 75bp easing this year, also referencing a need to provide further support to the labour market.

Familiar Guidance Repeated

Though the vote split may provide some degree of intrigue, the accompanying policy statement seems unlikely to do so.

In terms of economic commentary, the Committee’s assessment of underlying economic conditions is likely to be broadly unchanged, noting that job gains ‘remain low’, unemployment continues to show ‘some signs of stabilisation’, and that inflation remains ‘somewhat elevated’.

There is, however, likely to be reference made to recent geopolitical events, potentially mirroring the language used in the March 2022 statement, after Russia’s invasion of Ukraine, where the Committee noted that ‘the implications for the U.S. economy are highly uncertain, but in the near term…[events] likely to create additional upward pressure on inflation and weigh on economic activity’.

As for the monetary side of things, guidance here is likely to be little changed despite heightened uncertainty, with the Committee set to reaffirm their preparedness to ‘adjust the stance of monetary policy as appropriate’, while also alluding to the ‘extent and timing’ of additional rate changes moving forwards.

Forecasts In Focus

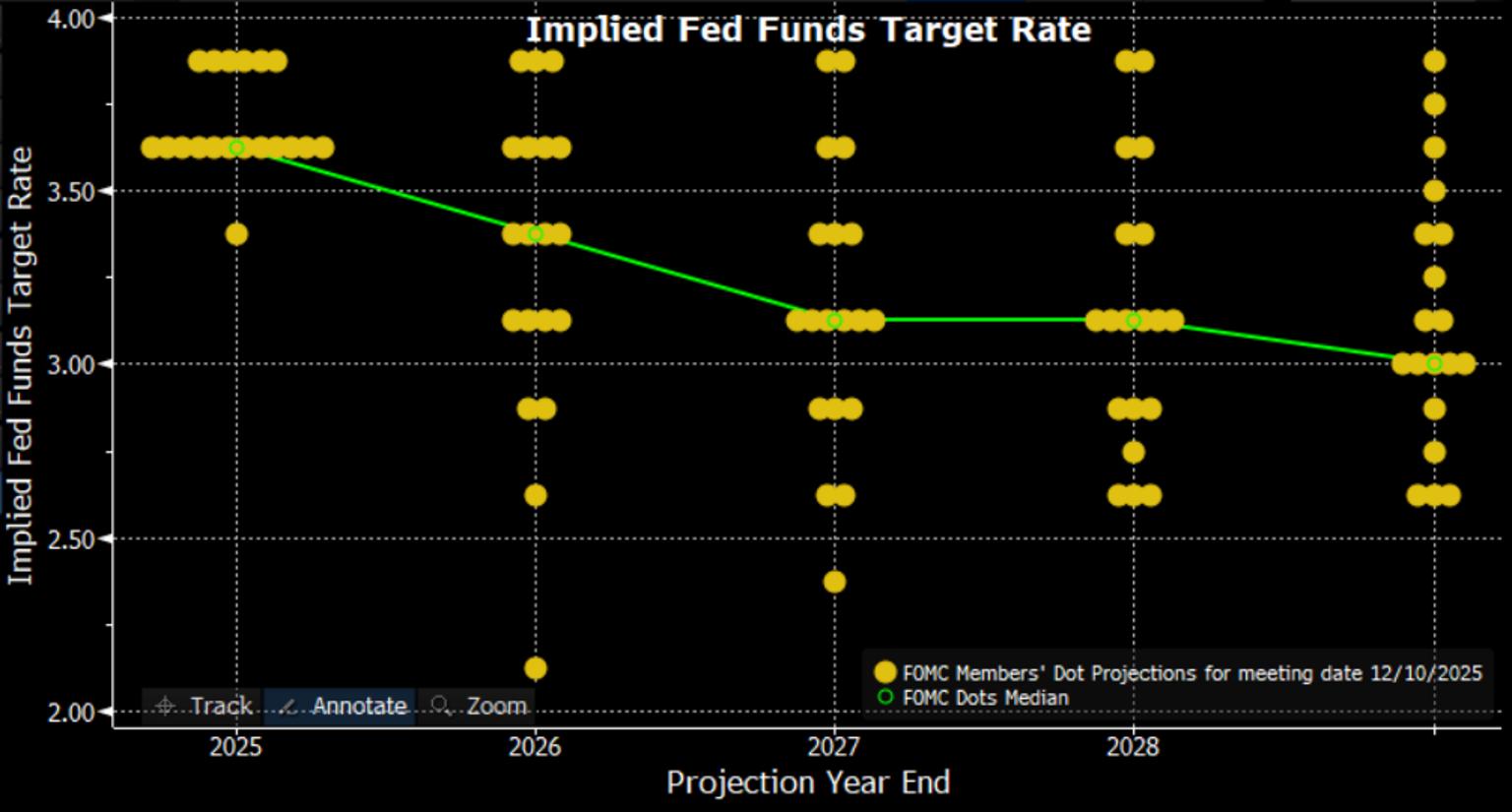

Along with the updated policy statement, the FOMC will also release an updated round of economic projections, including a fresh ‘dot plot’. The SEP, though, is almost certain to have a very short shelf life indeed, given the ever-changing geopolitical backdrop, while the projections will also be shrouded in a much greater degree of uncertainty than is typically the case.

That said, beneath the uncertainty which now clouds the outlook, the US economy remains relatively resilient, with the economy having continued to grow at a solid clip – excluding the impacts of the Q4 25 government shutdown – albeit while the labour market remains in ‘no hire, no fire’ mode, with the 3-month moving average of job gains sitting at a meagre 6k.

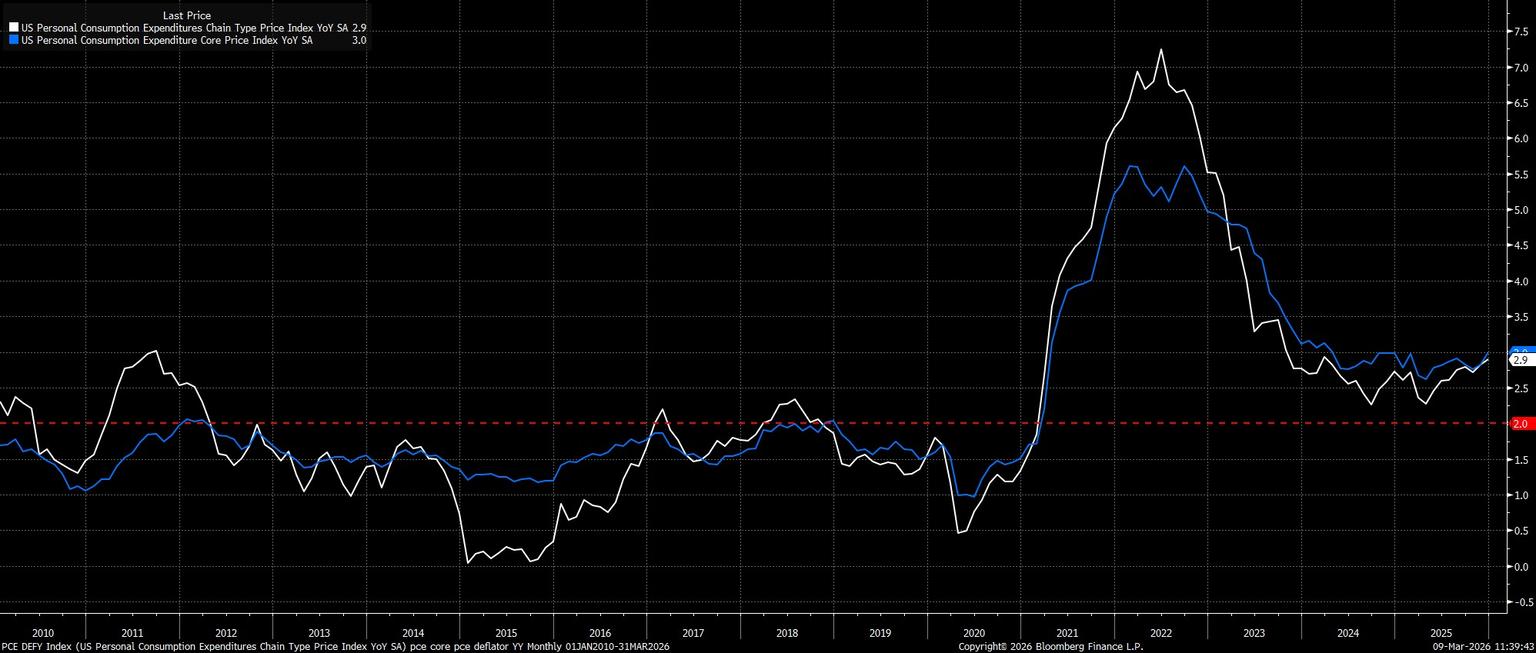

Still, in the near-term, the macroeconomic impacts of higher energy prices are fairly obvious. Namely, a boost to headline PCE, and a modest headwind to GDP growth, with the duration of the commodity shock determining how severe those impacts might ultimately prove to be. In any case, the Committee seem unlikely to project much by way of second-round inflation effects, in turn continuing to project a return to 2% core PCE by the end of the forecast horizon. Importantly, as a net energy exporter, the inflationary impulse from any energy shock is likely to be more contained in the US, than elsewhere.

Dots Could See Hawkish Revision

Taking into account the rapidly shifting geopolitical backdrop, participants would be wise to place even less stock in the ‘dot plot’ than usual, with Chair Powell likely to further downplay its importance at the post-meeting press conference.

Still, the ‘dots’ will be published as usual, and the median 2026 dot could well see a hawkish revision, to signal no further rate cuts this year, given that it would only take three Committee members nudging their ‘dot’ above the December median at 3.375% to cause the March median dot to be revised 25bp higher. One shouldn’t read too much into such a move, especially when the ‘longer-run’ dot should remain unchanged at 3.00%.

Powell Presser In Focus

Taking into account the highly uncertain backdrop, and how the FOMC continue to face risks to both sides of the dual mandate, Chair Powell’s penultimate press conference will attract even more attention than usual.

Powell, though, is likely to play things with a ‘straight bat’, not wanting to be drawn into any concrete policy commitments, or be ‘boxed in’ when it comes to the policy path. As a result, the furthest that Powell is likely to go is to reiterate that policy is not on a ‘preset’ course, with the Committee continuing to take a ‘meeting-by-meeting’ approach, while likely also noting that the normal course of action for a central bank would be to look through a ‘short-lived’ energy price shock.

As for other matters, Powell is still unlikely to be drawn on his future plans after May, and whether he intends to remain a Governor until the end of his term in January 2028, while likely also making no comment on ongoing legal matters surrounding the Fed, or regarding Kevin Warsh’s nomination to succeed him. On the whole, Powell is likely to stress a message of remaining patient amid heightened uncertainty.

Conclusion

That uncertainty will keep the FOMC on hold for the time being, as the Committee seek further clarity on the degree of upside inflation risk that is now present, while also seeking to prevent second-round effects form emerging, ensuring that the commodity shock indeed remains a ‘short-lived’ inflationary hit.

Providing that this does indeed prove to be the case, and that the disinflationary process resumes later in the year, further rate reductions remain on the cards, not least considering the relatively fragile labour market backdrop, with the pace of hiring still subdued. Geopolitical events, then, are likely to prove a case of cuts ‘postponed’, as opposed to cuts ‘cancelled’. Those cuts, though, are much more likely to be delivered under Chair designate Warsh, than under Powell, barring a material deterioration in labour, or financial, conditions between now, and the April meeting.