- English (UK)

Japan Snap Election: Why PM Takaichi Is Seeking a Stronger Mandate and What It Means for the Yen, JGBs and Nikkei

Japan’s snap election scheduled for 8 February is best understood not as a tactical political reset, but as a deliberate attempt by Prime Minister Sanae Takaichi to consolidate authority at a time when fiscal, monetary and market dynamics are becoming increasingly intertwined. The decision reflects Takaichi's political calculation of strong personal approval ratings, the opposition remains fragmented and the policy window to reshape Japan’s fiscal trajectory may be narrowing.

At its core, this election is about converting popularity into power to pass legislation. While Takaichi commands broad public support, her ability to govern has been constrained by a slim majority in the Lower House and an unfavorable configuration in the Upper House. That imbalance has introduced friction into budget negotiations, limited the scope of fiscal initiatives and increased the political cost of compromise. Calling a snap election is an attempt to remove those constraints before macro conditions or voter sentiment deteriorates.

Why the timing matters

The timing is also important as Japan is approaching the fiscal year-end with unresolved questions around the supplementary budget, consumption tax policy and the medium-term path of government borrowing. From Takaichi’s perspective, entering this phase with a slim majority mandate would risk policy paralysis. Securing a stronger majority offers a chance to anchor expectations and move decisively on her economic agenda.

Coalition arithmetic and opposition weakness

The current LDP–Japan Innovation Party JIP arrangement has been workable but narrow, offering stability rather than strength. Polling suggests the LDP could secure a simple majority on its own with the potential to approach a two-thirds threshold when combined with JIP. That upside risk is meaningful, particularly given the lack of momentum behind the opposition’s attempt at consolidation.

The formation of the Centrist Reform Alliance CRA was intended to present a credible alternative but early indications suggest limited voter enthusiasm. Support appears soft, especially among undecided and younger voters and the alliance has struggled to articulate a compelling counter-narrative to Takaichi’s growth-focused message. This fragmentation materially increases the probability that the election strengthens the incumbent government’s position.

Why a two-thirds majority changes everything

From a market standpoint, the distinction between a simple majority and a two-thirds supermajority is highly important. A decisive result would allow the government to override the Upper House and pass legislation without prolonged negotiation. That would reduce political uncertainty but it would also remove an institutional brake on fiscal expansion. Markets generally welcome clarity, but they are less comfortable when policy ambition is unconstrained.

The policy agenda if Takaichi succeeds

If Takaichi emerges with a two-thirds mandate, the policy direction is unlikely to be subtle. The focus would be firmly on fiscal support, hoold relief and strategic spending, even as the Bank of Japan edges toward gradual normalisation. The most contentious element of this agenda is the proposed abolition of the foodstuffs tax. Politically, the measure is popular and easily communicated, but fiscally it is problematic.

At present, there is no clear funding mechanism for potential tax cuts. Absent offsetting measures, implementation would almost certainly require additional government debt issuance. That raises immediate questions about debt sustainability at a time when Japan’s primary balance is already under pressure and ultra-long yields have become increasingly sensitive to supply dynamics.

Market implications: yen, bonds and equities

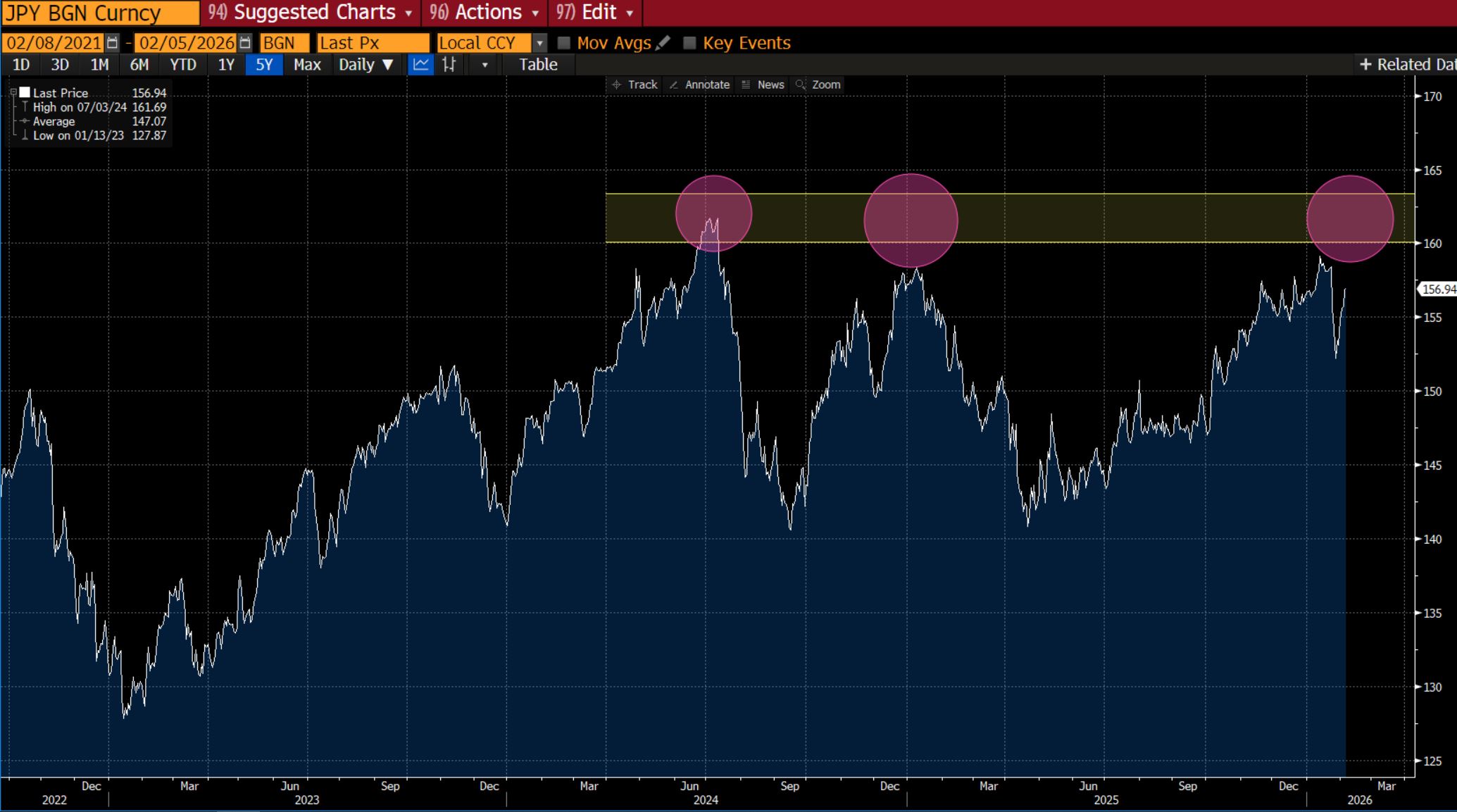

This is where market reactions become more complex, a strong LDP victory would likely revive at least initially. Equities would be supported by expectations of fiscal stimulus, policy continuity and a weaker currency. At the same time, the yen would likely face renewed depreciation pressure as investors reassess the balance between fiscal expansion and monetary tightening.

Japanese government bonds, particularly at the long end, would be the key pressure point. Unfunded tax cuts and the prospect of a larger deficit would argue for a steeper yield curve, with long maturities bearing the brunt of adjustment. Recent episodes of volatility suggest that this part of the curve is increasingly sensitive to fiscal signals, and a supermajority outcome is likely to amplify that sensitivity.

Some argue that even with a strong mandate, Takaichi is likely to pass the existing budget largely unchanged in the near term, with more ambitious spending measures deferred to the second half of 2026. Under this interpretation, post-election moves in markets could prove short-lived particularly given the proximity to the fiscal year-end.

The monetary policy overlay

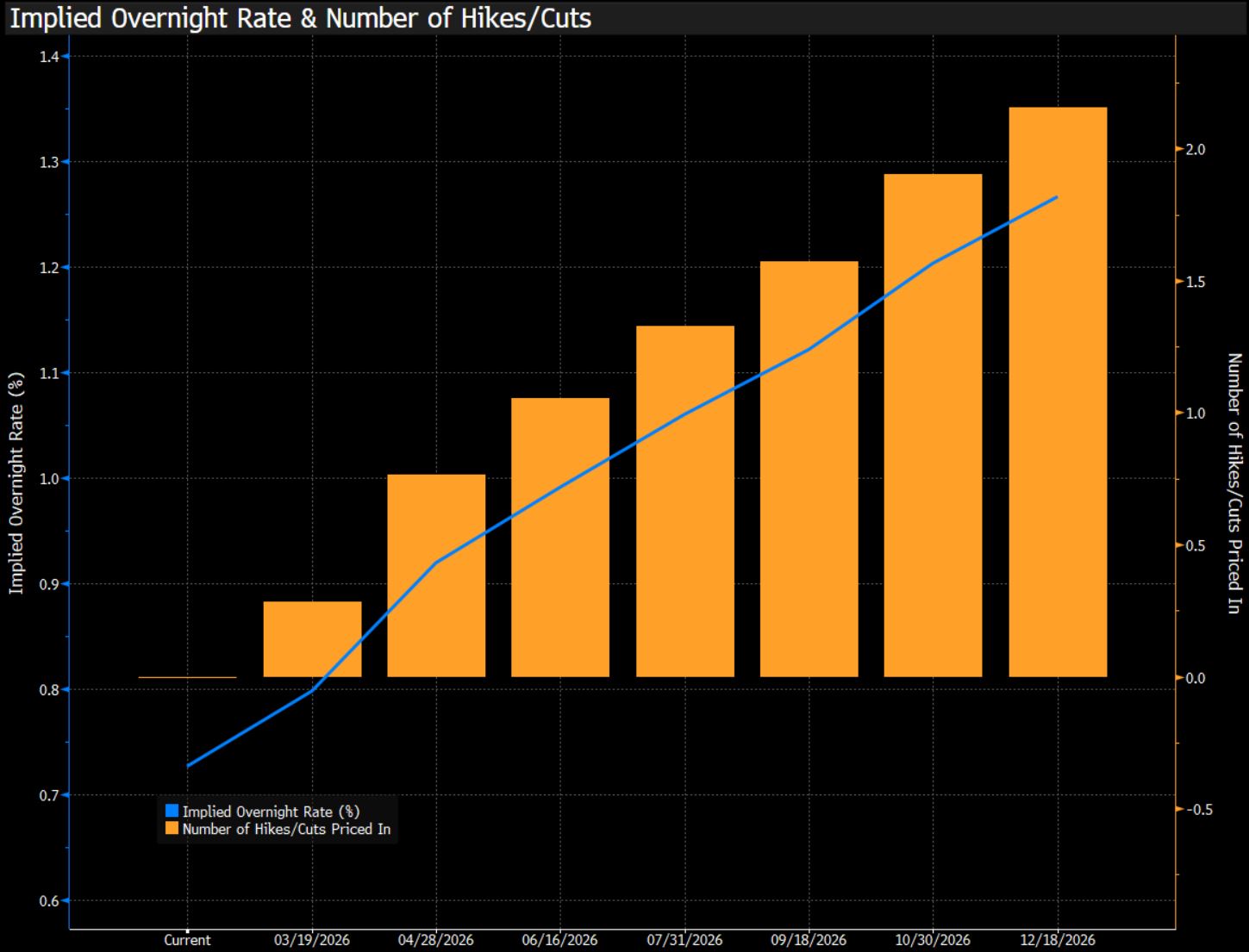

A clear electoral victory that weakens the yen and lifts inflation risks could ultimately force the Bank of Japan to tighten more than currently expected, near two implied hikes of 25bp each by year-end. Conversely, a less decisive outcome or an outright loss would likely strengthen the currency, flatten the yield curve and delay policy normalisation as BOJ reassess fiscal plans.

The most likely scenario

The most probable scenario remains an LDP-led victory that strengthens Takaichi’s hand in the Lower House. A two-thirds supermajority is not assured but it is a credible upside risk. Such an outcome would tilt the balance toward further expansionary fiscal policy, place pressure on the yen and long-dated government bonds, and remain broadly supportive for Japanese equities.

In this sense, this election is less about political survival and more about mandate expansion. Takaichi is effectively asking voters to endorse a more assertive fiscal stance in exchange for growth and stability. Markets are responding by weighing the benefits of decisiveness against the risks of unfunded ambition. The outcome will shape Japan’s political landscape and the relative performance of its key asset classes in the months ahead.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.