- English (UK)

January 2026 UK Jobs Report: Slack Persists Ahead Of Energy Shock

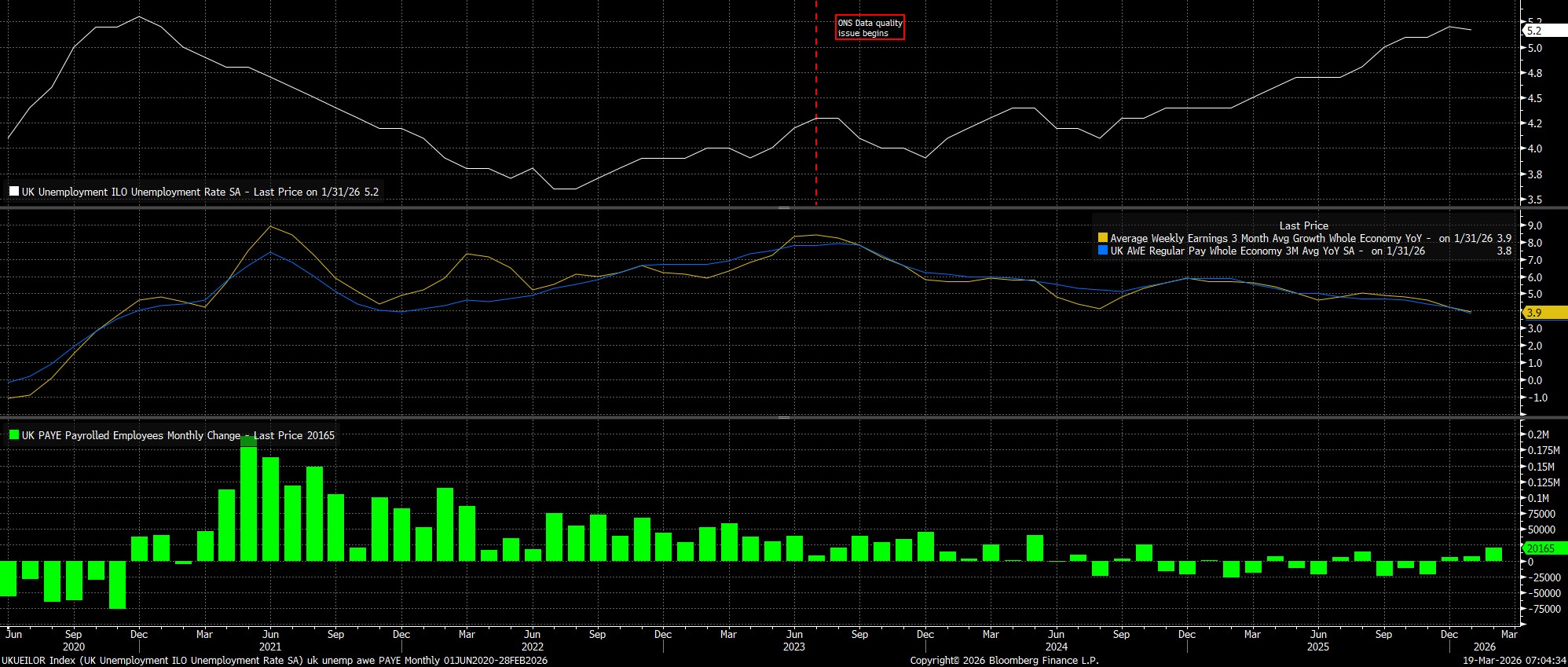

Unemployment, in the three months to January, held steady at 5.2%, unchanged from the level seen in December, albeit still at a post-pandemic high.

Meanwhile, pay pressures continued to ease. Overall earnings rose 3.9% YoY, the slowest pace since November 2020, while regular earnings rose 3.8% YoY, also the slowest pace since November 2020. Digging into the data, private sector earnings growth is now essentially at target-consistent levels, having risen 3.3% YoY in January, though public sector earnings growth continues to run at almost double that level, albeit being skewed by base effects to some degree.

As for the more timely PAYE payrolls metric, data pointed to employment having risen by 20k in February, the first monthly increase in six, though the data should be taken with a bit of a pinch of salt, given how prone to revisions the series appears to be.

Zooming out, the data will have little-to-no immediate impact on the BoE policy outlook. MPC members will have had advance sight of the report on Monday, but the 'Old Lady' is highly likely to stand pat on policy this lunchtime, maintaining Bank Rate at 3.75%, adopting a 'wait and see' approach in light of the uncertain economic outlook amid conflict in the Middle East, and the ongoing surge in energy prices. Such a decision is likely to have come by virtue of a 7-2 vote.

That said, this morning's data does imply that a significant margin of labour market slack is continuing to emerge. This, in turn, leads to there being a relatively low risk of energy-induced inflation leading to second-round effects, which could cause prices pressures to become more persistent. This means not only that the 'hump' in headline inflation should prove short-lived, but also that the greater risk is of present events having a detrimental impact on demand, which would be worsened by the BoE adopting too-tight a policy stance.

Hence, with the proviso that all calls are held with relatively low conviction right now, and assuming that greater geopolitical clarity has emerged by the time of the April MPC, data of today's ilk should allow the MPC to resume easing once more, with a majority of policymakers 'looking-through' any temporary energy-induced inflation, and instead focusing on sustainably achieving the 2% inflation aim over the medium-term, while also cushioning against the risks of a broader demand shock.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.