- English (UK)

January 2026 UK GDP: Downside Surprise As Geopolitics Clouds The Outlook

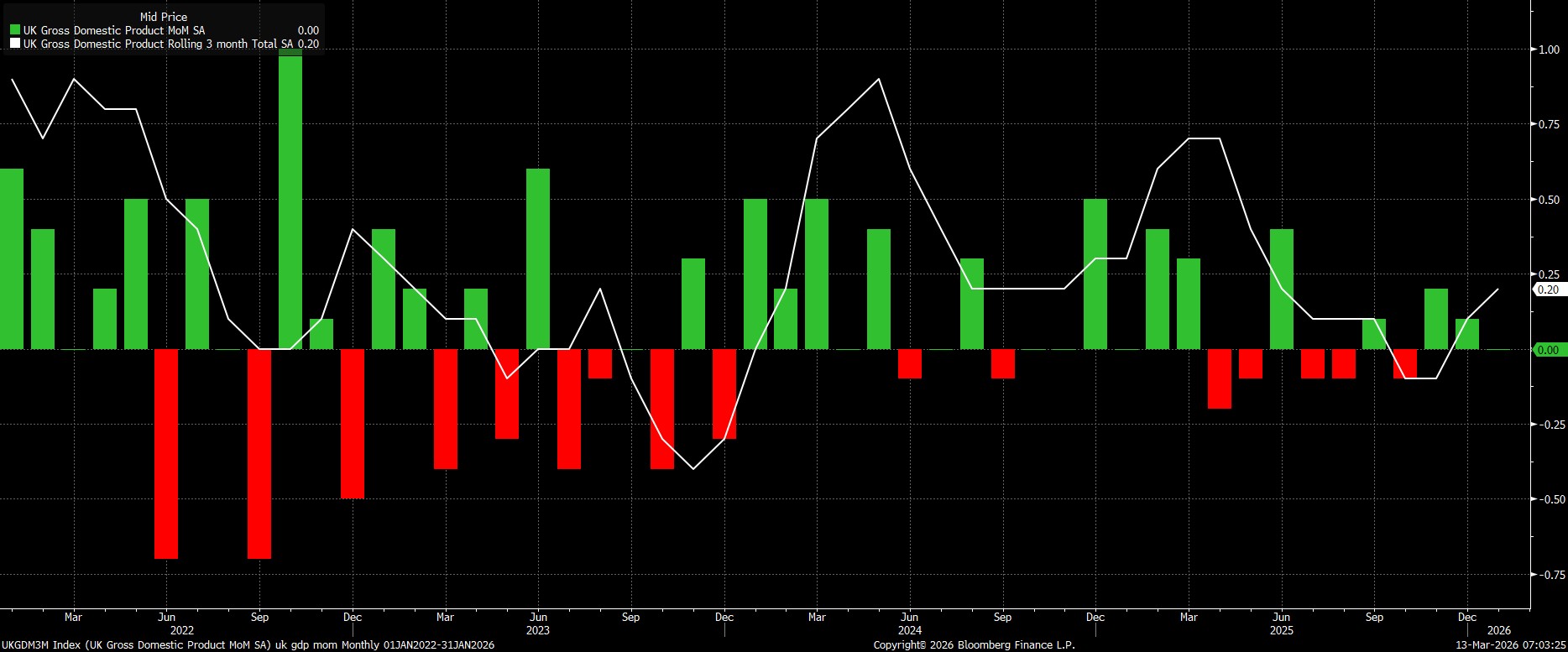

Data showed the economy having failed to grow at all in January, with GDP printing 0.0% MoM, the first time that the economy has not recorded a monthly increase in output since last October. Zooming out, the broader growth picture remains anaemic, with the economy having only grown by more then 0.5% MoM three times in the last two years, and not by a pace quicker than 0.2% MoM since last June.

Meanwhile, on a rolling 3-month basis, the economy grew by 0.2% 3Mo3M, largely driven by the monthly contraction seen last October falling out of the data.

Interestingly, the GDP data runs contrary to what other leading indicators had been signalling, with the pick-up in output indicated by data such as recent PMI surveys having not been confirmed by this morning's report, despite there likely having been some degree of pick-up in activity following the lifting of pre-Budget uncertainty which depressed activity to such a significant degree in Q3 & Q4 25. That said, the data is clearly now incredibly stale, especially in the context of recent developments in the Middle East.

Ongoing conflict in the Gulf, coupled with the effective impassability of the Strait of Hormuz, has triggered a significant commodity price shock, with nat gas prices having surged, and Brent crude having settled north of $100bbl for the first time in almost four years. While the precise impact of this shock depends almost entirely on its duration, which at this point is clearly highly uncertain, at face value one can assume that the surge in energy prices will result in higher near-term headline inflation, while also posing headwinds to economic growth.

With that in mind, the base case is now that the Bank of England's Monetary Policy Committee stand pat at next week's meeting, seeking further clarity on the evolving backdrop, as well as a full assessment of the impact of higher commodity prices as part of the April Monetary Policy Report. That said, with the potential for second-round inflation impacts rather limited, owing to the parlous state of the UK labour market, and with policymakers likely to 'look-through' any energy-induced inflation as temporary in nature, further rate reductions remain on the cards.

For the time being, assuming that commodity flows have begun to normalise, it seems plausible that the 'Old Lady' can deliver the next 25bp cut at the April meeting, with further cuts likely beyond then, taking rates to a neutral level (approx 3%) by year-end. That said, were the energy price shock to prove more sustained, the Bank would likely adopt a longer 'pause' in the easing cycle, though any rate hikes at this stage seem a very long shot indeed, not least considering that Bank Rate is still a fair way into 'restrictive' territory.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.