It’s not exactly controversial to say that the G10 FX market has been pretty dull of late.

This week has been a pretty solid example of that. Besides the JPY, which has softened a chunk amid two dovish nominations to the BoJ board, the rest of the complex has been very turgid and moribund indeed, with ranges tight, and weekly changes minimal, at best.

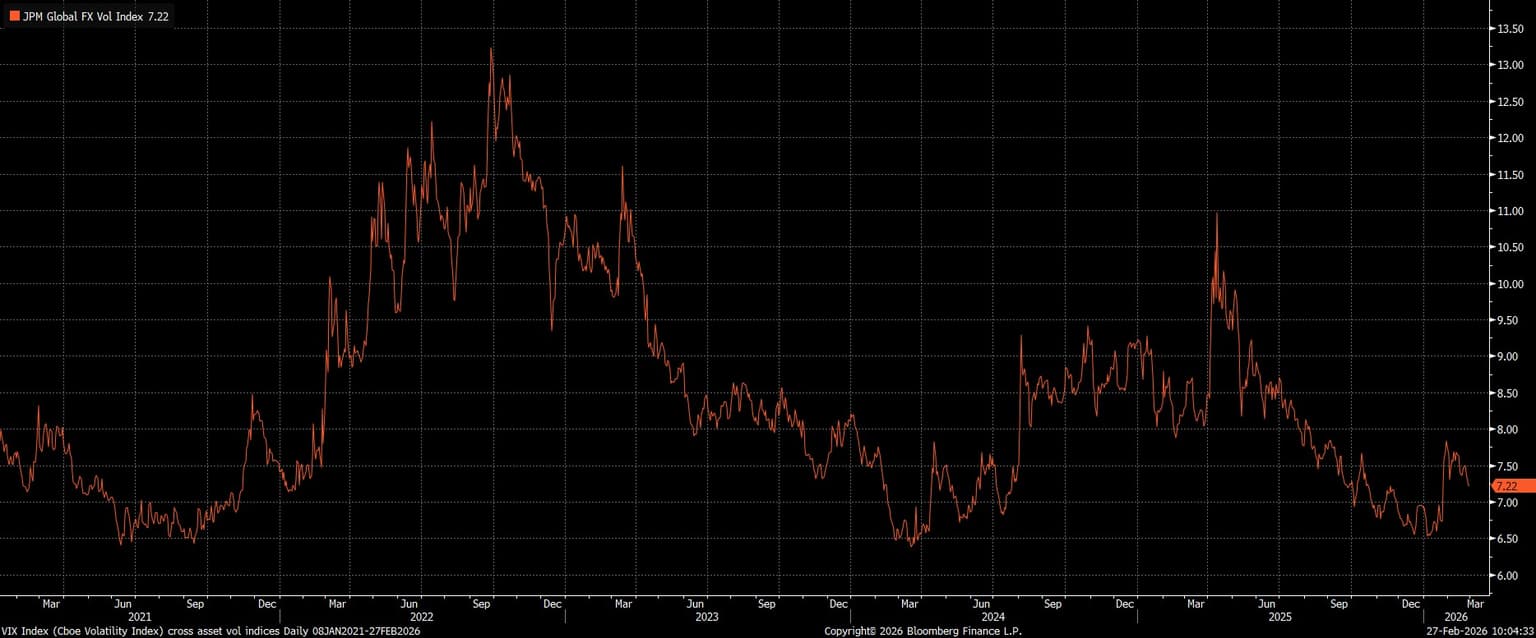

Given the pitifully low levels of realised vol, it’s not exactly surprising that implied vol is on the floor too. one-week implieds across G10 are well within the bottom 25th %ile of their 52-week ranges, while JPMorgan’s gauge of G7 FX implied vol trades at a six-week low.

What’s Caused Vol To Decline?

The first obvious question that this prompts is what’s triggered this drop-off in market activity, with volumes having also been relatively light.

Clearly, this is not for want of catalysts. Over the last week we’ve not only had a SCOTUS ruling striking down the IEEPA tariffs, but also plenty of headline noise on the geopolitical front, as US-Iran talks remain ongoing, and as the US military buildup in the Middle East continues. At the same time, political risk has resurfaced here in the UK, as PM Starmer’s premiership looks on even shakier ground after the Gorton & Denton by-election result. Meanwhile, outside the G10 space, the PBoC appear increasingly concerned at the appreciation in the CNY/H, after cutting the FX reserve ratio to 0%.

In many ways, I wonder if this plethora of catalysts is one of the main reasons why conditions have become so turgid. Put simply, there are too many moving parts – before even considering ongoing concerns over Fed independence, and the Trump Admin’s policymaking volatility – which in turn leads to a relatively broad-based lack of conviction, as noise drowns out signal, resulting in participants preferring to wait things out on the sidelines.

Another consequence of that is there being no obvious narrative for participants to latch onto, and trade off. H1 25 was ‘sell America’ as the dollar dived and markets adjusted to ever-changing tariff policies, but since last summer there has not been a single, dominant, durable narrative running the show. Japanese FX jawboning provided a modicum of interest last month, though it’s since turned out that the majority of JPY vol actually came as a result of a seemingly random ‘rate check’ initiated by Treasury Sec Bessent. Once a market participant, always a market participant…

What May Cause Vol To Pick-Up?

None of that is to say that there is nothing interesting going on. Far from it, in fact.

Typically, the main driver of the FX complex is macroeconomic divergences, often on a yield basis, with that in turn stemming from differing growth, inflation, and central bank outlooks. Right now, there is plenty of divergence out there! For instance, here in the UK, the labour market is weakening at a rather worrying rate, with the BoE consequently likely needing to ease policy faster than markets currently discount. Concurrently, expectations persist that the FOMC will adopt a more dovish approach once Chair designate Warsh takes the helm, albeit only if further disinflationary progress has been made by the spring. At the other end of the spectrum, money markets expect that each of the RBA, RBNZ, and BoJ will hike rates at least once before the year is out. This is hardly an era of co-ordinated monetary policy across DM!

Despite those policy divergences, from a growth perspective the story is different, with stateside growth continuing to vastly outpace that seen in DM peers, when one removes the effects of last year’s government shutdown. Though the ‘sell America’ trade has a catchy ring to it, there is no chance at all of the greenback losing its reserve status, and in fact given how bearish sentiment and positioning have both become, risks arguably now tilt towards dollar upside, if policy noise can be dialled down to an extent where participants are again able to re-focus on those underlying fundamental drivers.

In fact, I think that’s the broader point here. A return to any sort of trend in the FX space likely needs the ‘noise/signal ratio’ to tilt much further back in favour of ‘signal’ once again, else there seems little prospect of any of the tight ranges with which we’ve become familiar breaking down any time soon. All the time that headline noise remains deafening, as it does right now, conditions are likely to remain choppy, and ultimately rather messy.