- English (UK)

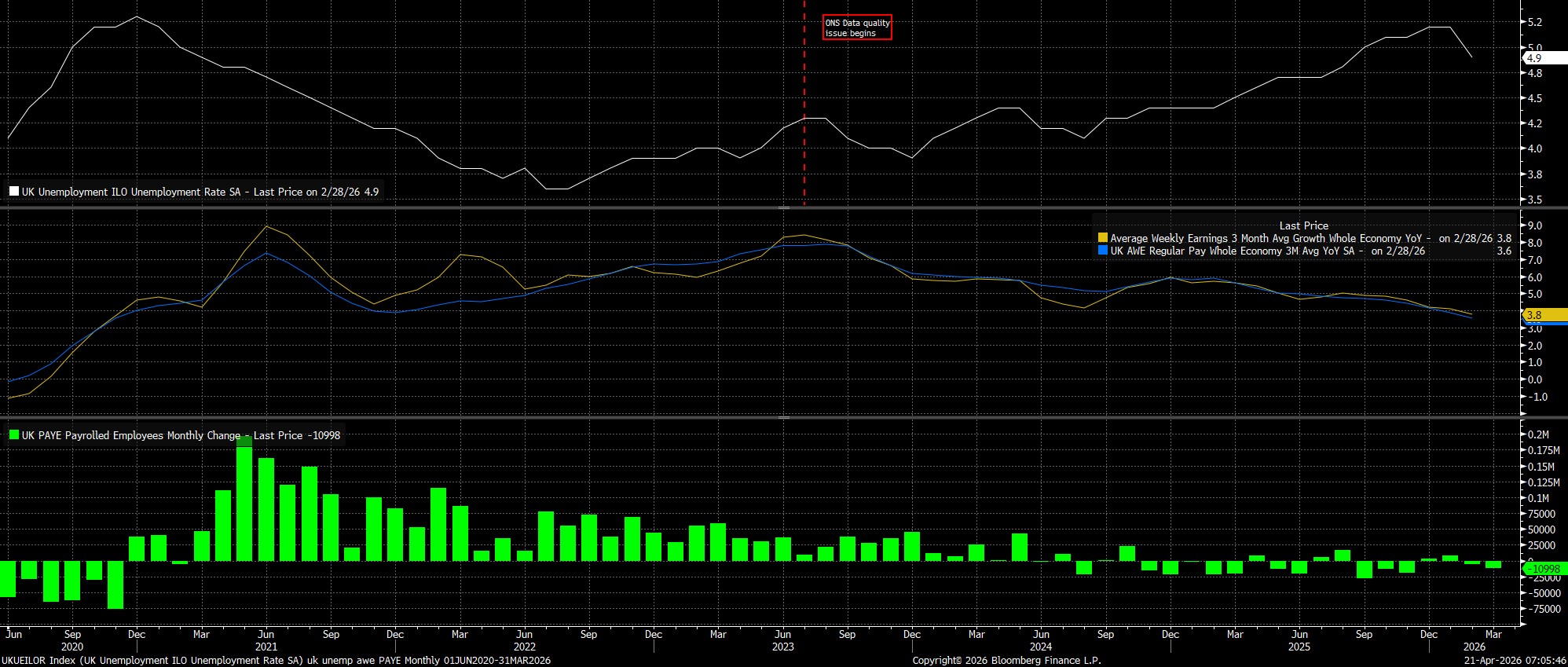

Headline unemployment unexpectedly declined to 4.9% in the three months to February, the lowest level since August last year, though any excitement should be tempered by this data having been compiled before conflict broke out in the Middle East, and by the economic inactivity rate having climbed by 0.2pp over the same period, to 21.0%.

As for earnings, pay pressures continued to ease across the board. Overall earnings rose 3.8% YoY in the same period, the slowest pace since the tail end of 2020, while regular earnings rose 3.6% YoY, also the slowest pace since the pandemic. That said, and while pay growth continues to moderate towards target-consistent levels, there remains a notable divergence in the pace of earnings growth across the economy, with private sector earnings having risen 3.2% YoY, but public earnings having risen by 5.2% YoY. Although a base effect is skewing this data, to an extent, such a divergence is clearly unsustainable over the longer-run

Meanwhile, turning to more timely indicators, the report pointed to PAYE payrolls having fallen by 11k, in March, marking a second straight decline after a downwardly revised February figure, but also pointing - potentially - to early signs of employers having adopted a more cautious stance amid increased geopolitical uncertainty, and the surge in energy prices.

Although the data is, by and large, somewhat stale in referencing the pre-conflict period, there is still some signal that market participants and policymakers alike can gleam from the report. Chiefly, that labour market momentum in the UK remains weak, and that a notable margin of slack continues to emerge.

Of course, this comes as risks to the labour market, moving forward, tilt clearly and heavily to the downside, with conflict in the Middle East, and the associated broader economic uncertainty, likely to result in employers remaining cautions in terms of their hiring plans, and thus labour demand likely remaining soft for some time to come. Various changes to 'day one' workers' rights, which have begun to be implemented since the start of April, are also likely to give corporates further reason to remain reluctant on the hiring front.

For the Bank of England, today's data likely does little to 'move the needle' overall in the short-term, with the MPC remaining focused squarely on the inflation outlook for the time being. Still, that focus is less on the level to which spot headline CPI rises as a result of the recent surge in energy prices, and instead on the degree to which that surge poses a risk of price pressures proving persistent, as well as the potential for 'second-round' effects to emerge.

Given the weak, and weakening, labour market backdrop, it remains the case that both employees have little bargaining power, thus limiting the potential for a 'wage-price spiral' to develop, and that corporates have limited pricing power, to pass on higher input costs in the form of price hikes.

With this in mind, the base case remains that the energy price shock is likely to result in a short-lived 'hump' in headline inflation, as opposed to anything longer-lasting. Consequently, the MPC are likely to retain their 'wait and see' approach for the time being, standing pat at the April meeting, though there remains a path to one, or two, rate reductions still being delivered in the second half of the year, providing that the MPC have obtained sufficient confidence in price pressures proving temporary. In turn, that is likely to permit a modest degree of loosening, in order to provide some support against the negative demand shock that higher energy prices will likely trigger.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.