- English (UK)

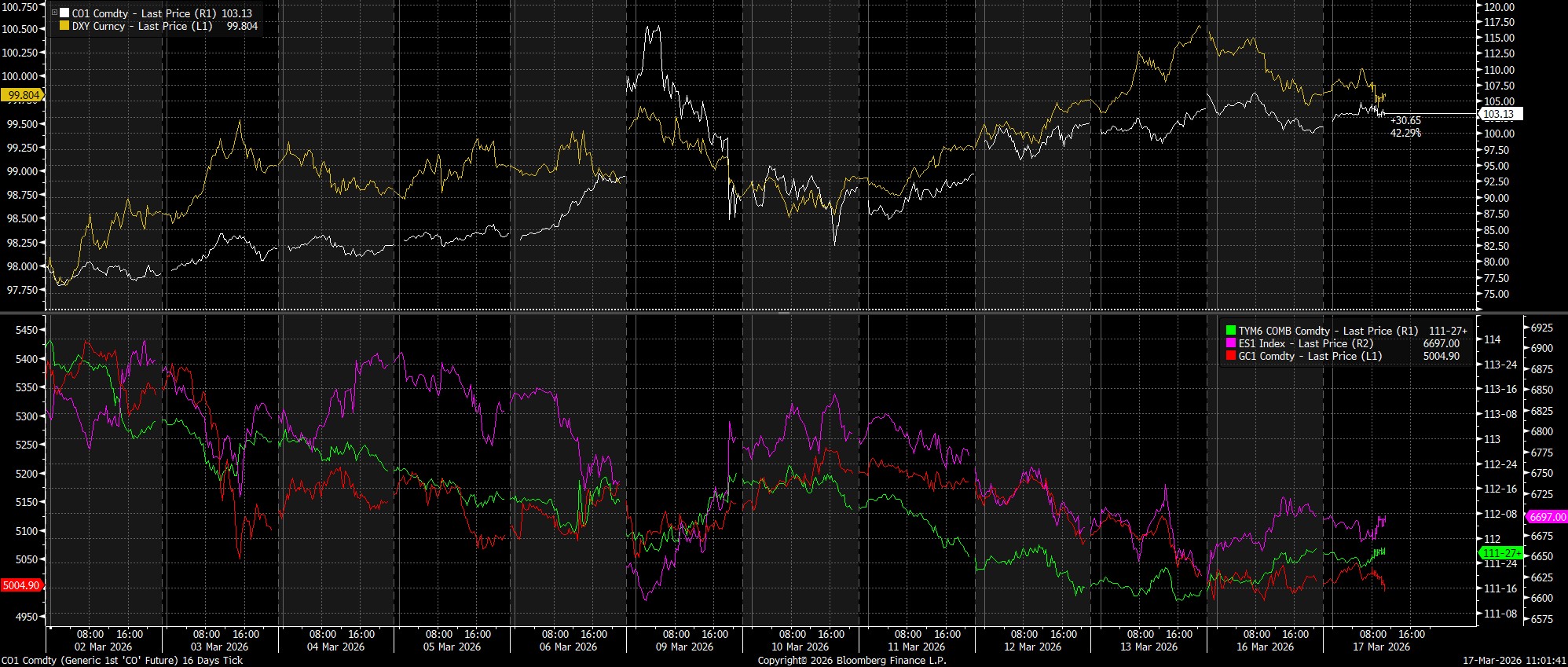

Cross-Asset Correlations Remain At 1 With Crude Still In The Driving Seat

Somewhat calmer tones have begun to prevail over the last day or so, with market participants seemingly becoming, to a degree, desensitised to headlines regarding developments in the Middle East.

To be clear, this is not in any way to diminish the human suffering that continues to be inflicted, as kinetic action continues, with the US and Israel continuing to strike various Iranian targets, and Iran retaliating with strikes not only on military bases in the region, but on energy infrastructure in the Gulf too.

However, as is often the case with events such as this, there is a diminishing return when it comes to incoming news flow, with participants having now discounted the idea that, sadly, conflict is likely to wear on for some time. This means that, in order for a headline to have the same negative market impact that it had a fortnight ago, it must be several orders of magnitude more severe than when the conflict begun.

That said, it remains the case that, as of the time of writing, there is little-to-no sign of any material de-escalation, or any ‘off-ramps’ being taken. While President Trump has again expressed a belief that the war will end “soon”, Trump has also stated that such an end will not come this week. Furthermore, the Strait of Hormuz remains essentially impassable to the vast majority of traffic, tightening commodity supply day-by-day, and exerting continued upward pressure on energy prices.

It is this aspect that the market remains squarely focused on, given that the magnitude, and duration, of the ongoing energy price shock is essentially the sole factor that will determine how high headline inflation spikes, and how significant a growth headwind may emerge.

In light of this, we remain in a market where, for all intents and purposes, cross-asset correlations are at 1. Put simply, where crude goes, everything else will follow.

Given how pivotal energy prices are to the outlook at large, it seems plausible that such a tight relationship will continue, until material signs of de-escalation emerge, or Hormuz transits normalise.

Consequently, for the time being at least, it seems fairly self-explanatory as to what the over-arching market biases are likely to be. When it comes to risk assets, participants are naturally likely to come at things from a relatively cautious standpoint, though I would stress that we have already seen risk levels taken down considerably over the last couple of weeks which, when combined with a continued desire not to get ‘caught short’ in the event of what many see as an inevitable Trump ‘U-turn’ could well put a floor under equity prices to a certain degree. Still, risk levels are unlikely to be dialled up again in significant fashion until light begins to appear at the end of the proverbial tunnel.

As for havens, the dollar is really the only thing that ‘works’ for now. The Swissie can’t be bought for fear of SNB intervention, while the JPY is counted out due to Japan being a huge energy importer. Meanwhile, gold continues to trade more like a high-beta risk asset than anything else, while buying Govvies as a haven in an inflationary environment is a fool’s errand.

One other thing to consider, is whether there are market levels that might force the ‘TACO’ moment that many are waiting for. While there may be a view that short-term market turbulence is a price worth paying for a more stable geopolitical environment in the long-run, I’d imagine that spoos under 6,500 and/or the 30-year Treasury north of 5% would provoke concern in the White House, not least given the potential for those eventualities to slam the wealth effect into reverse, thus presenting greater downside risks for the US economy at large.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.