Spread bets and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72% of retail investor accounts lose money when trading spread bets and CFDs with this provider. You should consider whether you understand how spread bets and CFDs work, and whether you can afford to take the high risk of losing your money.

- English (UK)

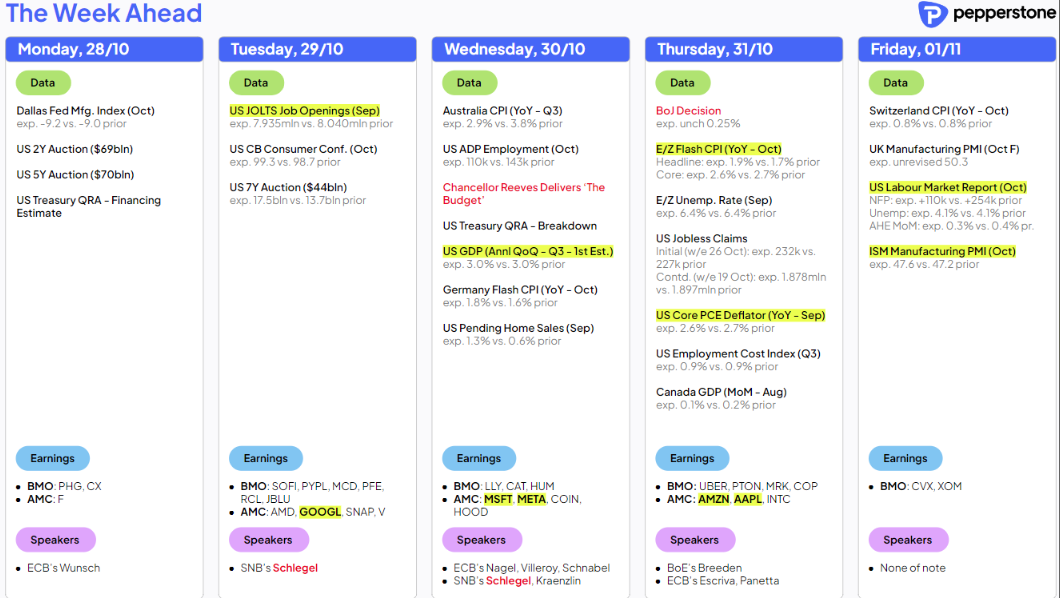

A Traders’ Week Ahead Playbook – Taking some chips off the table

While much ink has already been spilt outlining the measures likely to be heard from Wednesday’s UK budget, the prospect of a fiscally tight budget looms large. While JPY and JPN225 traders deal with the fallout from Japan’s Lower House election, they also look to Thursday’s BoJ meeting. We get PMI data in China and GDP prints in EU and Canada.

It seems whether we’re looking at political developments, tier 1 economic data or influential company earnings, there are landmines all over the shop for traders to navigate their positions over – Remaining vigilant, dynamic, and open-minded to changes in price action will subsequently serve any trader well this week.

The Risk Manager – Drilling down into the key event risks

The US election is now just 8 days away and while it may be an event many want out of the way, if anything the noise will only increase through the week, as will its impact on the trading environment. Trump remains well ahead in the betting markets, and ahead – but within the margin of error - in all 7 swing states (source: RealClear Politics) and this position has been consistent for long enough to make many think it is a real possibility.

After another strong week for the USD, many attempt to quantify the degree to which potential Trump tariff risk is priced into USD, as they do for equity indices, gold, and Treasuries. With leveraged FX players having added $25b in broad USD positioning over the past two weeks, it is logical to think some of this USD positioning has been placed in alignment with Trump’s perceived prospects of becoming president - although visibility on that call is unclear, given we can also argue that strong US economic data and a sharp reduction in Fed rate cut expectations has been the dominant driver of USD upside.

A far clearer visual of market election risk hedging is through the options volatility space, where there is a clear premium in the implied volatility (vol) for options expiring on 6 November (TLT ETF, S&P500, Russell 2k, NAS100) over the implied vol in options expiring 4 November. This implied vol premium is even more pronounced in the FX vol space, with USDMXN, EURUSD and USDCNH 2-week implied vol at the widest premium to 2-week realised volatility since the 2020 US election.

A rapid build in USD positioning

What’s clear is that this sizeable build in USD positioning is entirely justified on a number of fronts, and it does suggest that some may refrain from further chasing USD upside here, even increasing the risk that players who have been set long of USDs since early October, will either be tightening up their stops or taking some chips off the table and looking to reload into the trend at lower levels.

US data comes in heavy this week, with the Fed’s preferred inflation gauge (core PCE) and the US labour market in full view – JOLTS job openings, ADP, employment cost index, weekly claims, and nonfarm payrolls all under the spotlight. Payrolls are so important for market pricing, but this read will be messy, so gaining a true signal that could drive the US rates market, and the USD may be more of a challenge than in prior months given the hurricane-related impact, and port disruptions, and we see that with the consensus call for 110k jobs to have been created in October.

USDJPY trading higher with the LDP Party losing its majority in the Lower House

USDJPY was the big mover in G10 FX last week, with the spot rate hitting a high of 153.18, and we can already see buyers in the mix in interbank FX trade. While liquidity is always a factor on a Monday open, the spot rate is back above 153.00 trading the fallout from Sunday’s Japan Lower House election, with the LDP and coalition partner Komeito party falling short of a majority – this now raises the possibility of a change in Prime Minister before the Upper House election in 2025 and throws into question Japan’s fiscal position, where Japan is already running deficits comparative to that of the US at around 6% of GDP.

A messy political situation beckons, with traders trying to price next steps and the probability of a further expansionary budget, at a time when deficits are high and the BoJ have cut back hard on its JGB buying. Given the political developments, it certainly muddies the waters for this Thursday’s BoJ meeting and Gov Ueda’s presser, so in theory, the meeting shouldn’t be overly impactful on the JPY, even if market pricing suggests the BoJ could hike rates in either December or January.

EURUSD makes for interesting trading this week with spot hitting the double top target and having not just the US data flow to content with this week, but EU CPI will also be a factor. With 35bp of cuts priced for the Dec ECB meeting, a 50bp cut is now seen as a lineball call. With EU-US relative interest rate differentials driving EURUSD, both US and EU data matter for the exchange rate, so managing position with due care over news is essential this week.

Aussie Q3 trimmed mean CPI in focus

AUDUSD heads into the new trading week with shorts feeling good about their position, with the trend firmly lower, and the spot rate closing below the 200-day MA and eyeing a push below 0.6600. The FX rate has lost any correlation with industrial metals, Chinese/HK equity and the S&P500 and even screens cheap vs AUS-US 2-year forward interest rate expectations. Relationships come and go, but there is a trade-off between the flow of capital (the technicals) which argues for further downside, and the classic drivers of the exchange rate, which suggests the sell-off is perhaps overdone. Wednesday’s Aussie Q3 CPI could influence the AUD and Aussie interest rates, with headline CPI eyed to come in at 0.3% q/q / 2.9% y/y and the trimmed mean measure of CPI eyed at 0.7% q/q and 3.5% y/y.

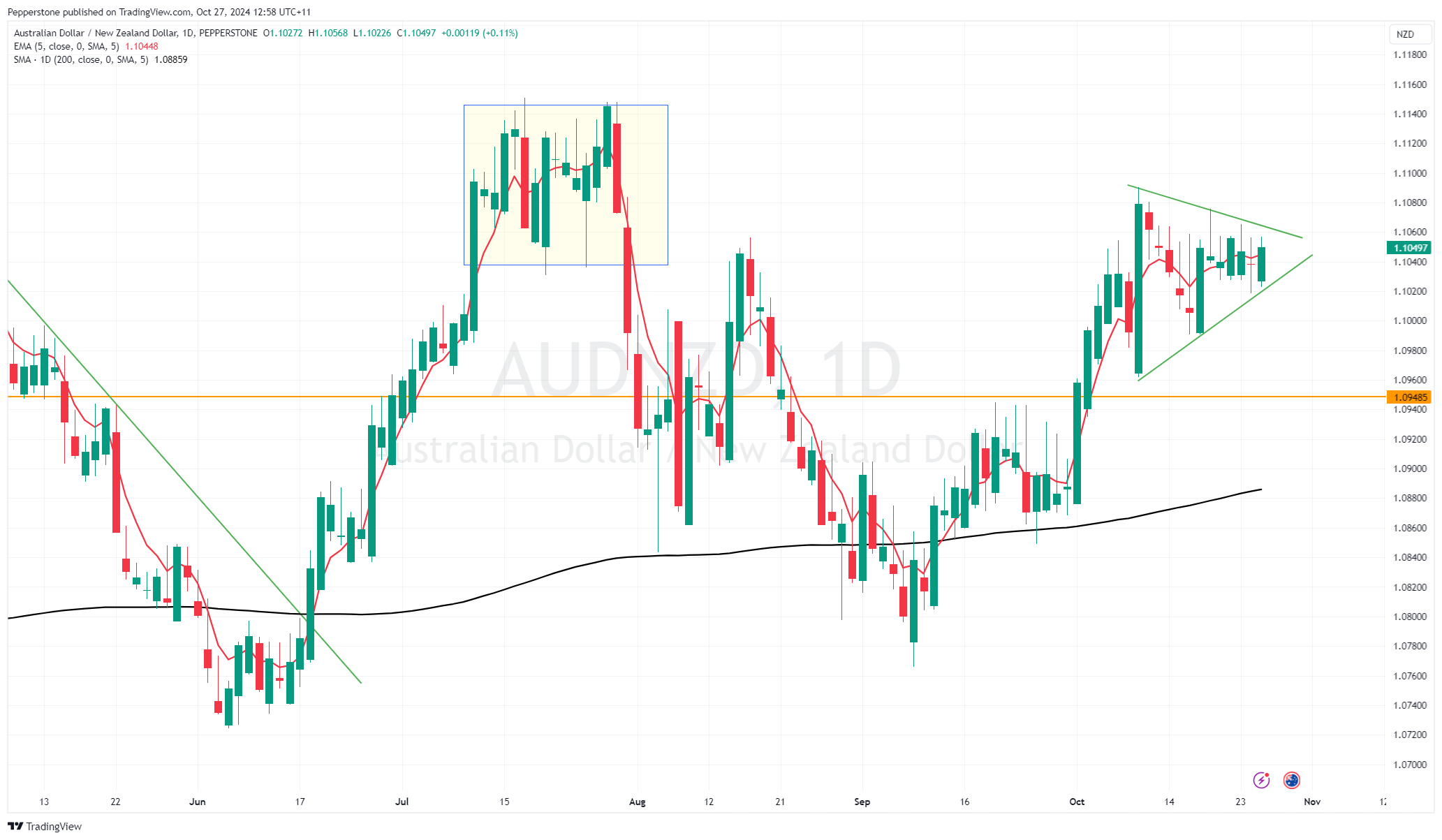

With a full 25bp cut not priced into Aussie swaps until April 2025, a trimmed mean CPI print below 3.3% y/y could see expectations of a cut in February increase. Conversely, a TM CPI print above 3.7% would see any remaining pricing of RBA easing in 2024 taken out of the rates pricing and may even result in a small degree of hiking expectations priced for the 5 Nov RBA meeting. AUDNZD is a cleaner expression of Aussie CPI and rate differentials, where on the daily we can see the consolidation in the price action – a break above the triangle consolidation would get me interested in renewed upside potential in AUDNZD.

The UK budget poses risks for GBP traders

A UK budget is never one many outside of the UK really give too much consideration to, but this week’s UK budget may be the exception. While many will refrain from assessing the intricacies of fiscal policy, this time the budget is a potential volatility event for the GBP, as it is for many of the companies in the FTSE100 that have high domestic sales. Chancellor Reeves will want to keep volatility in the UK gilt market in check, and there are signs that the measures could be gilt-friendly, which, in turn, may weigh on the GBP…. We shall see, but the budget is unfortunately a risk to manage.

Chinese equity markets looking towards PMIs and next week’s NPC meeting

Chinese/HK equity gets further attention this week, with traders looking to get set for the NPC meeting set from 4-8 November, with building expectations that the announcements will be far more defined on actions to drive demand and consumption. With the meeting having been tactically scheduled over the US election, one suspects we won’t know the fall substance and clarity of the finer points until the us election result is known, so the Chinese authorities have the chance to manage any fallout in the yuan or to curb outflows from domestic equity markets should Trump get in, and even more so should the GOP sweep Congress.

The hesitation to put money to work in China/HK equity can be seen clearly in the HK50 index, with the triangle consolidation pattern (on the daily) in play - which way this index breaks could set a trend through the week.

The big week for US company earnings

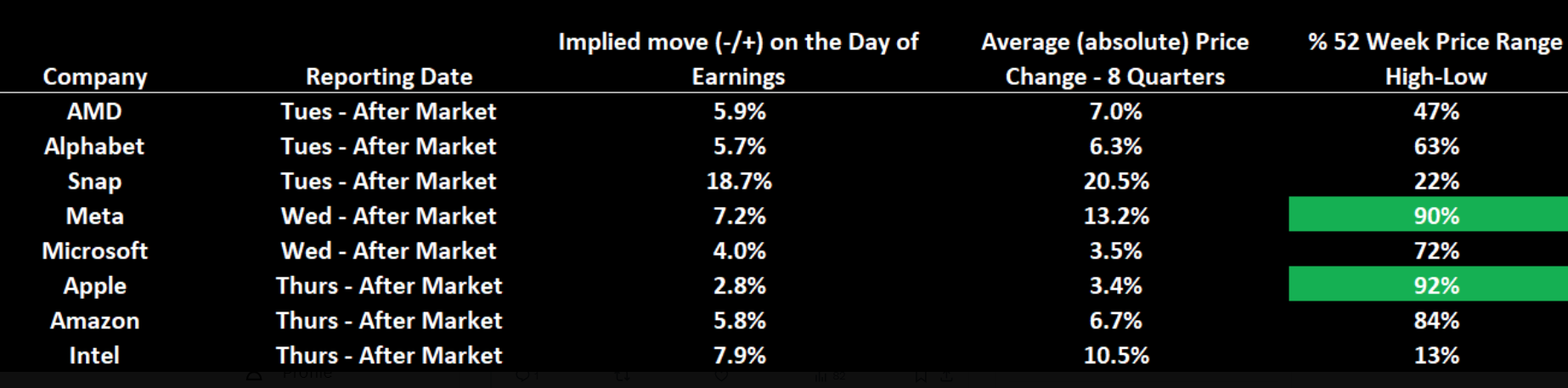

US Q3 earnings have thrown up some big moves in individual names and notably in Tesla (+22% w/w) and Newmont Mining (-16% w/w). It’s been a reasonable reporting period thus far, with 36% of S&P500 companies having reported quarterly earnings and 77% of these names having beating consensus EPS expectations by an average of 6%. 50% of these names have beaten expectations on the sales line, which is in line with the historical average. This coming week though, over 40% of the S&P500 market cap is due to report, with earnings likely to rival the US election news flow and the US data flow as a driver of sentiment.

Traders will be drawn to numbers from Alphabet, Meta, Microsoft, Apple, and Amazon, although AMD, Snap, Caterpillar, McDonalds, and Visa could kick onto the radar too. Meta is one of the most crowded longs in the equity space, so there is a high bar to please the market and with an implied move of -/+7.1% on the day of reporting, this could be one to put on the radar.

At an index level, the S&P500 closed the week -1%, and we see sideways chop and consolidation on the daily chart suggesting longs would want to see S&P500 futures hold above 5830, or we could see some of the weaker hands look to take some off the table. The Russell 2k (-3% over the past 5 days) and Dow (-2.7%) with the latter dragged lower by 3M, McDonald’s, and IBM. Let's see how traders work this through the week.

Good luck to all.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.