- English (UK)

Summary

- Fiscal 'Non-Event': Reeves & Co are attempting to make the 'Spring Statement' as much of a low-key affair as possible, with no fresh policy announcements on the cards

- OBR Forecasts: However, the OBR will issue an updated economic outlook, albeit not an assessment of whether the fiscal rules are being met, though headroom has likely increased by virtue of the fall in Gilt yields

- Risks Remain: The 'Spring Statement', though, is unlikely to materially change the political backdrop, with risks to Starmer's premiership remaining elevated, and a spring leadership challenge still overwhelmingly likely

An Uneventful Statement

While we have come to associate UK fiscal events with major policy announcements, and typically elevated market volatility too, this time is likely to be different. Tuesday’s statement should be a considerably more low-key affair than we’ve become used to, with the Government having already indicated that the statement will contain little, or even no, new policy announcements.

In fact, calling this a ‘fiscal non-event’ is probably more accurate, considering not only that the statement comes just three months after last year’s Budget, and with the Treasury having hopefully learnt their lesson in terms of how much damage pre-Budget uncertainty did to the economy in the second half of last year.

OBR Forecasts In Focus

Although Reeves & Co are seeking to play down the importance of the Spring Statement, the OBR will nonetheless be issuing an updated round of economic forecasts, albeit one that does not include an assessment of the ‘headroom’ that the Chancellor has against the fiscal rules.

Despite that, recent news on the fiscal front has been relatively positive. A record budget surplus was recorded in January, albeit largely as a result of a surge in CGT receipts amid worries over future tax increases, though this nonetheless meant that, as of January, FYTD borrowing was running around £8bln below the level forecast by the OBR.

This, however, will have a relatively limited impact on the broader fiscal outlook, given that the fiscal rules are judged against the forecast for the 2029/30 fiscal year. Of considerably more importance on this front will be the recent decline seen in Gilt yields, with the benchmark 10-year having recently fallen to its lowest since December 2024. Even if the OBR shan’t issue their own estimate of the Chancellor’s headroom, it seems plausible that the 20-odd bp decline in Gilt yields since the autumn will amount to somewhere between £4-5bln in additional headroom.

_10_2026-02-26_10-23-07.jpg)

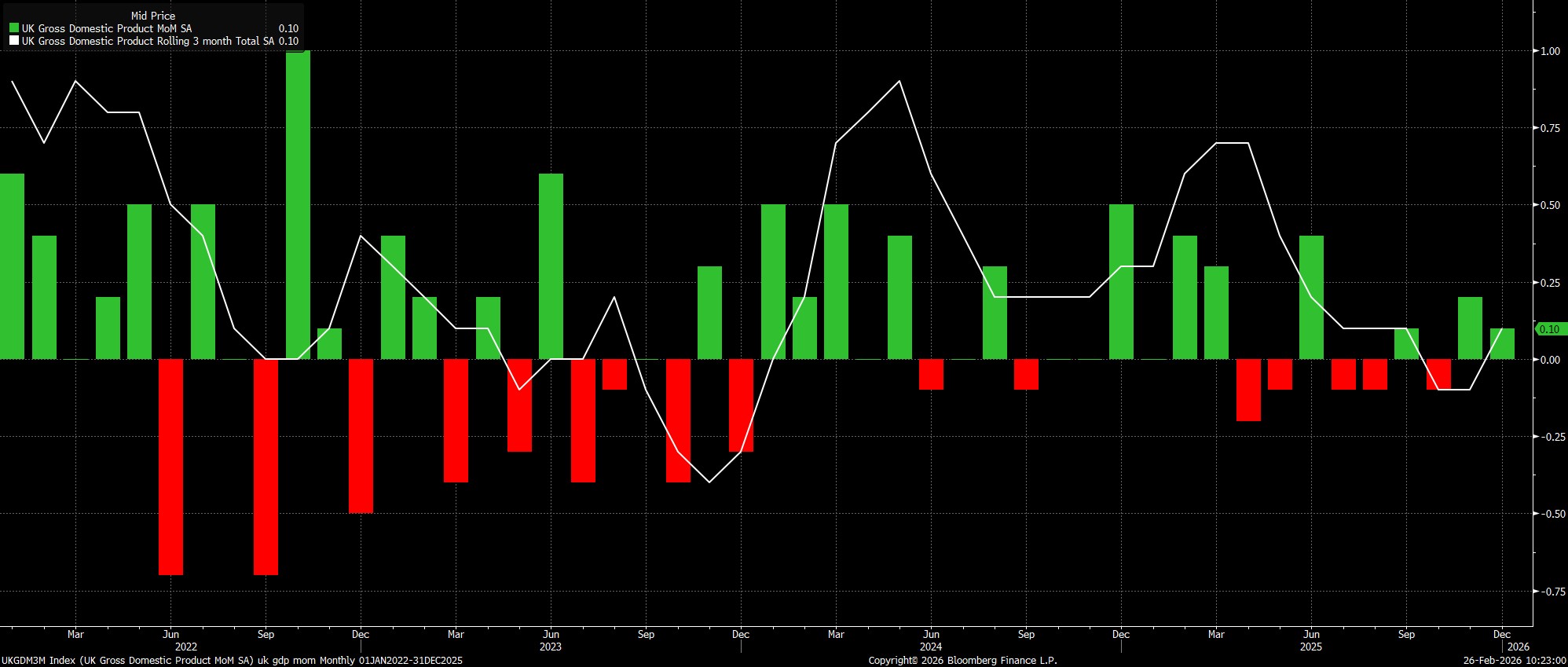

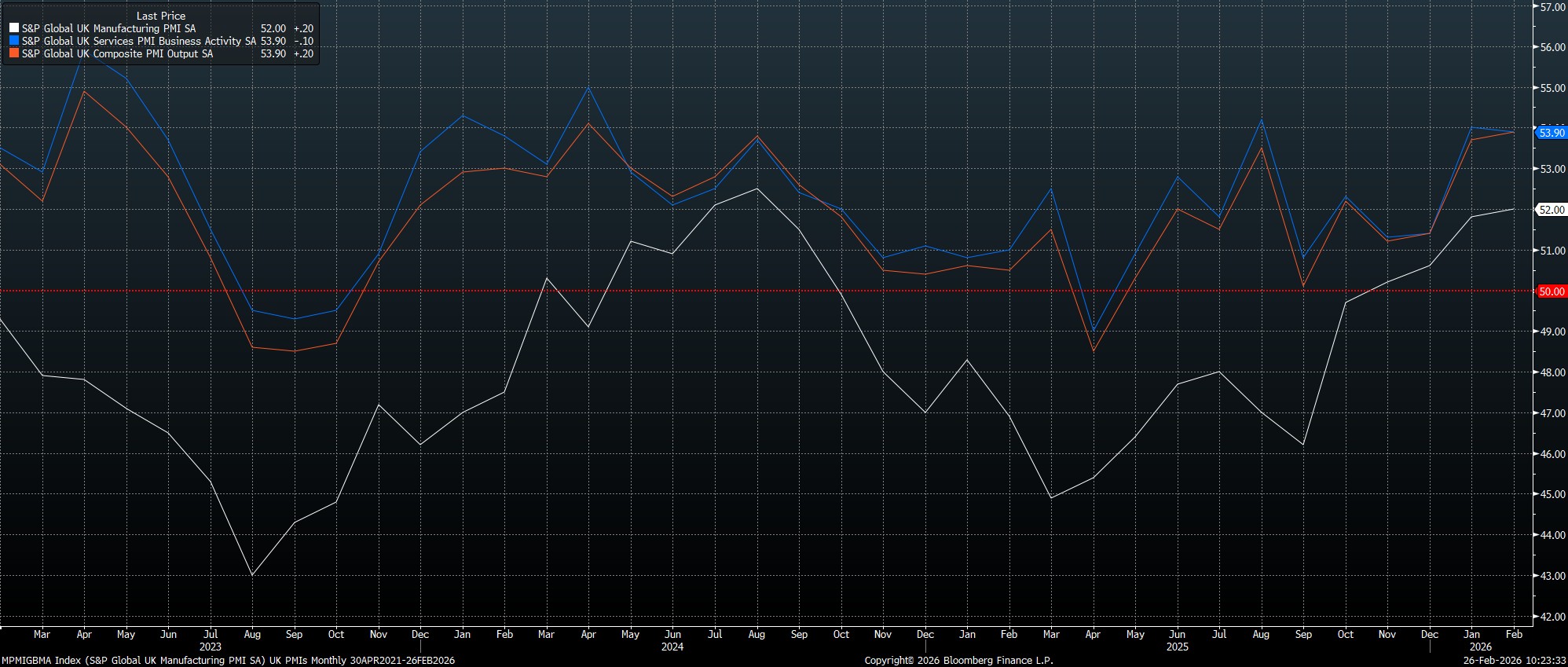

Not A Macro Gamechanger

Taking into account the lack of any fresh policy announcements, it seems highly unlikely that the ‘Spring Statement’ will be any sort of game-changer in terms of the broader economic outlook.

While the alleviation of pre-Budget uncertainty has led to a largely mechanical rebound in economic activity as this year has got underway – taking the composite output PMI to a near 2-year high – it remains questionable the degree to which this momentum can continue. These question marks, primarily, emanate from the dismal state of the labour market, with headline unemployment having risen to near 5-year highs in the three months to December, and with a margin of slack rapidly emerging.

Though this does further reduce the (already slim) risk of price pressures proving persistent, and raises the likelihood that the BoE will return Bank Rate to a neutral level around 3% this year, a sustained improvement in labour conditions seems relatively unlikely, barring a change in government policy. Not only has the cost of hiring been increased (higher employer NICs, higher minimum wage, etc.), but the risk associated with doing so has increased too (workers’ rights bill), combined leading to a broad-based reluctance to hire unless, and until, either of those dynamics were to change.

Gilt Remit

Along with the OBR’s forecasts, the year-ahead Gilt issuance remit will also be in focus.

Consensus expectations are not yet available, however recent reporting via the FT indicates that issuance is likely to be in the region of £250bln for the year from April. If realised, such a figure would be the lowest such figure in four years, though how this issuance is split across the curve is of considerably more importance than the absolute number, with the DMO likely to continue to lean heavily towards the front-end, as structural factors (e.g. falling number of DB pension schemes) continue to reduce participation at the long-end.

_10_2026-02-26_10-23-48.jpg)

Political Uncertainty Persists

No matter the content, or lack thereof, within the Spring Statement, it seems highly unlikely that political uncertainty will materially lift any time soon.

At the time of writing, the Gorton & Denton by-election result is not yet known, however the moment of ‘maximum danger’ for PM Starmer remains the 7th May local elections, given the high likelihood of a terrible result for Labour, meaning that a leadership challenge through late-spring and early-summer remains my base case. Though Starmer could be on the ballot in such a contest, it seems highly unlikely that he would prove victorious, with a considerably more left-wing challenger likely to win out.

Market Implications

Considering that rather toxic combination of both lingering political risk, as well as mounting expectations of a considerably looser fiscal stance after an inevitable leadership challenge, the market outlook clearly tilts bearish for UK assets.

Though the FTSE 100 should prove insulated to domestic political concerns, given the huge concentration of overseas revenue earners in the index, risks clearly tilt to the downside for the GBP – most significantly in the crosses – and to the downside at the long-end of the Gilt curve, where steepeners remain my preferred play.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.