- English

.jpg?height=93&quality=30)

Bank of England (BoE):

I’ll kick off proceedings with one of the more recent factors which threw markets a big curve ball, namely the BoE. Volatility was the name of the day as GBPUSD slumped circa 1.5% and 2Y Gilts dropped as much as 25bps (a 6 sigma move) immediately after the news broke. Governor Bailey and other key MPC members had actively encouraged the markets’ pricing of short term UK rates with their rhetoric leading up to the November meeting. I think what was so frustrating for FX and rates traders was that the market hadn’t priced a rate hike overnight – it was a build-up through September and October, yet the BoE not once tried to lower the temperature. This has damaged their credibility rightly so and created significant uncertainty around their forward guidance. How should traders react now to a messy central bank reaction function? What I’m more sure of is, expect more volatility and I think data will become increasingly important as central banks’ credibility remains questionable. Looking at the below chart we can see GBPUSD wears a higher volatility with its 1-month implied volatility only bested by the high beta, commodity AUDUSD, coming in at 7.0775. The higher volatility creates more opportunities for traders to exploit..png)

(Source: Bloomberg Chart of 1-month implied volatilities for FX pairs - Past performance is not indicative of future performance.)

Speaking of data, the major reason for the BoE’s lack of action was due to preferring to be patient and wait for additional labour data after the expiry of the furlough scheme (October data will arrive just in time for December meeting) in order to assess the absorption rate of unemployed workers back into the labour force. Unofficial survey data is looking solid on this front with vacancies high and redundancies low. ONS data from last week indicated 87% of those furloughed have now returned to their jobs as well as very low redundancy rates. If the official data continues on this strong footing then a December rate rise becomes likely. The market is pricing just shy of a 15bps hike currently for the December meeting (see chart below). However, I’d caveat this with the fact that there were only 2 dissents at the November meeting (would have made December hike more probable if it was 5-4, instead of 7-2) and since the BoE gained independence they’ve never hiked at Christmas. So will pound traders be disappointed again?

Carry Potential:

The medium-term carry prospects for the pound aren’t looking too peachy. The BoE pushed back against a terminal rate of 1% by the end of 2022 via their inflation forecasts being below the 2% target. Essentially, they’ve placed a cap on the hiking cycle by doing this – the result will be a flatter Sonia curve further out. Additionally, the curve inverts around 2024, meaning the market sees rate cuts returning (policy error) based on the market’s current rate expectations. This also acts as a quasi-cap on how high rates can go, because if 1% by the end of 2022 is going to lead to a slowdown in growth and a U-turn in monetary policy then how will the economy handle even higher rates? This clearly eliminates the pound as a good candidate for the carry trade - diminishing its longer term bullish prospects. Minimal hikes combined with punchy inflation will push real yields lower – sending traders in search of yield pickup elsewhere.

.png)

(Source: Bloomberg Chart of UK money market pricing - Past performance is not indicative of future performance.)

Geopolitical - Brexit:

Article 16 of the Northern Ireland Protocol is back in the headlines once again. Traders have been consumed with central bank policy and rates markets, but maybe it’s time to dust off the old Brexit playbook once again. We’ve been here before though with the screeching and threats only for it to be resolved with some sort of fudge. However, Brexit fatigue and complacency may cause a blind spot for GBP traders if things really escalated. So what are the issues? The higher administrative burdens (checks) are causing issues for Northern Ireland businesses as well as the role of the European Court of Justice being a red line for the UK. I always feared when the original deal was signed that the agreement on NI was unsustainable and would lead to problems down the road.

Essentially, there are two paths this can take. 1) There’s some sort of compromise and technical changes to the existing agreement – GBP neutral to positive or 2) Both parties can’t resolve the issues and the nuclear option of Article 16 is invoked. There are concerns this could collapse the entire trade agreement all together i.e. trading on WTO terms and lead to a tit for tat trade war. This would very likely see a Brexit risk premium discounted into GBP crosses, causing price to move lower.

Natural Gas Exposure:

Given natural gas comprises circa 38% of the UK’s total energy consumption, they are unfortunately adversely exposed to swings in the price of this commodity. As we head into winter, if it is particularly cold, this could be another headwind for sterling. Russia supply has been tepid at best and if there isn’t a ramp up in this soon then we could see another squeeze. This will only add to the inflationary pressures the UK economy is already experiencing.

Stagflation Risk:

Many were left stumped when sterling failed to appreciate as much as one would normally expect in response to the aggressive tightening in front end rates. My interpretation of this boils down to the type of environment in which the rate hiking cycle takes place. Hiking rates to curb inflationary pressures while damaging the growth profile isn’t exactly positive for any currency. Additionally, monetary policy isn’t the correct medicament for blunting supply side inflation caused by supply chain bottlenecks, worker shortages and surging energy prices. In fact, it would probably exacerbate the growth slowdown. JPM created a misery-index, which measures the stagflationary risk across economies. The UK is the 2nd worst economy globally, highlighting the difficult position it finds itself in. The budget held on October 27th wasn’t incredibly expansionary for the economy either as spending was offset with tax rises. Recent GDP estimates from the BoE highlighted the deceleration in growth with 7% for 2021 (7.25% prev), 5% for 2022 (6% prev) and then falling to 1.5% in 2023 and 1% in 2024.

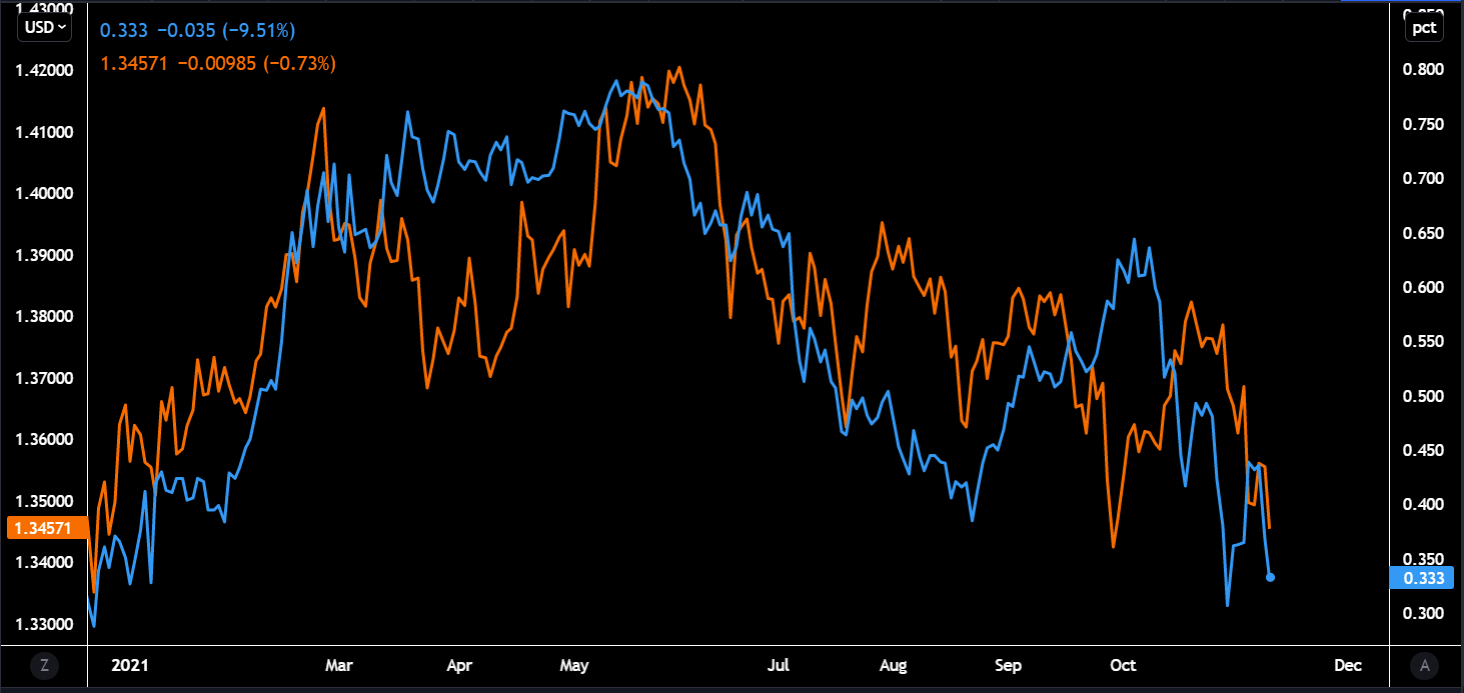

Correlated factors - S&P500, Oil, UK2s10s Curve:

Gains in the US equity market usually are positive for the quid, given it’s a barometer for global risk sentiment. However, although still important this factor’s importance has waned a tad as FX traders re-focus on rate differentials. The UK exports a significant amount of oil, so higher prices here lead to better terms of trade and can have a small beneficial impact on the currency, however, if this is a result of soaring gas prices then the net effect will be negative for the pound. Lastly, the most correlated variable with GBPUSD is the UK 2s10s yield curve. What we tend to see is when the gilt curve steepens it usually boosts GBPUSD and vice versa for a flattening of the curve. However, with policy error fears being priced in we’ve seen a flattening of late and this has been a headwind for GBPUSD. The curve steepened very briefly as the front end repriced lower post BoE meeting, but has now flattened again unfortunately for sterling bulls.

(Source: TradingView - Chart of GBPUSD and UK 2s10s Yield Curve. Orange line - GBPUSD and Blue line - 2s10s curve, Past performance is not indicative of future performance.)

Sentiment:

Net specs positioning had built up quite a decent net long into the BoE meeting. Most of these would have been liquidated during the aggressive sell-off. Given the headwinds from a macro-economic perspective, there is plenty room for shorts to proliferate and apply pressure on the pound. Taking a gander at risk reversals further reveals soured sentiment as all tenors are deeply negative. This means puts are trading at a premium to calls (more demand for one over the other), meaning the markets are expecting lower prices to prevail.

GBPUSD:

I think the dollar will strengthen against the pound for a couple of idiosyncratic reasons. On the monetary front/rate differentials, in my opinion the US has an under-priced money markets curve with asymmetric risks for a repricing higher on the basis of stronger economic data surprises turning the Fed more hawkish. Growth is stronger in the US than the UK. Additionally, the Fed Funds futures curve is steeper than the Sonia curve (better longer-term carry prospects). The US is not as exposed to soaring natural gas prices like the UK is. Lastly, a Brexit risk premium if priced in would invariably weaken the pound against the dollar. A potential risk for the dollar which is now on my radar is the potential for Jerome Powell to be replaced by uber dove Lael Brainard (she was seen at the White House the other day). Betting markets still see Jerome as the horse to back with a solid probability of re-election.

GBPUSD is eyeing the 1.34 support level with the lower line of the descending channel just below. A break of this level, sees next major support at 1.33. The RSI has rolled over and moving towards oversold (could help hold the 1.34 level). All the moving averages are pointing downwards, not a great sign trend wise. Price rallies look like they're going to be used to add shorts to for the time being, with plenty of resistance above - 21-day EMA, 50-day SMA and horizontal lines. Zooming out to a longer time frame such as the monthly chart, we see what could be a double top pattern. If this plays out the projected target would be around the 1.20 level.

EURGBP:

Even with a more dovish BoE, they will still be outdone by the ECB who are very unlikely to even lift rates until 2023. This should help send EURGBP in a southerly direction over the medium-term. An escalation in Brexit though could keep the euro stronger against the pound, acting as a floor for EURGBP.

(Source: TradingView - Past performance is not indicative of future performance.)

EURGBP saw a massive spike recently, tagging the 200-day SMA as well as the upper trend line of the descending channel. The 200-day SMA should cap rallies as we've seen previously and may be a good zone to look at shorts. Right now price needs to either break above the 200-day SMA or below the 50-day SMA as it gets squeezed by the two moving averages. Targets to have on the radar would be - 0.857-0.86 (200-day SMA). On the downside, the 50-day SMA around 0.851 and the horizontal support at 0.85 (also 21-day EMA).

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.