- English

WHERE WE STAND – A choppy day on Friday, with participants having little by way of major news or data catalysts to digest, and price action itself providing little by way of useful signal.

The pound was the most eye-catching in the G10 FX world, though, with cable sinking back towards the $1.26 handle after October’s GDP figures pointed to a second straight 0.1% MoM contraction, largely a result of the significant pre-Budget uncertainty seen during the reference period. Things, though, look like they’re only set to get worse here, particularly with the full impacts of the Budget yet to be felt, namely in terms of the National Insurance changes.

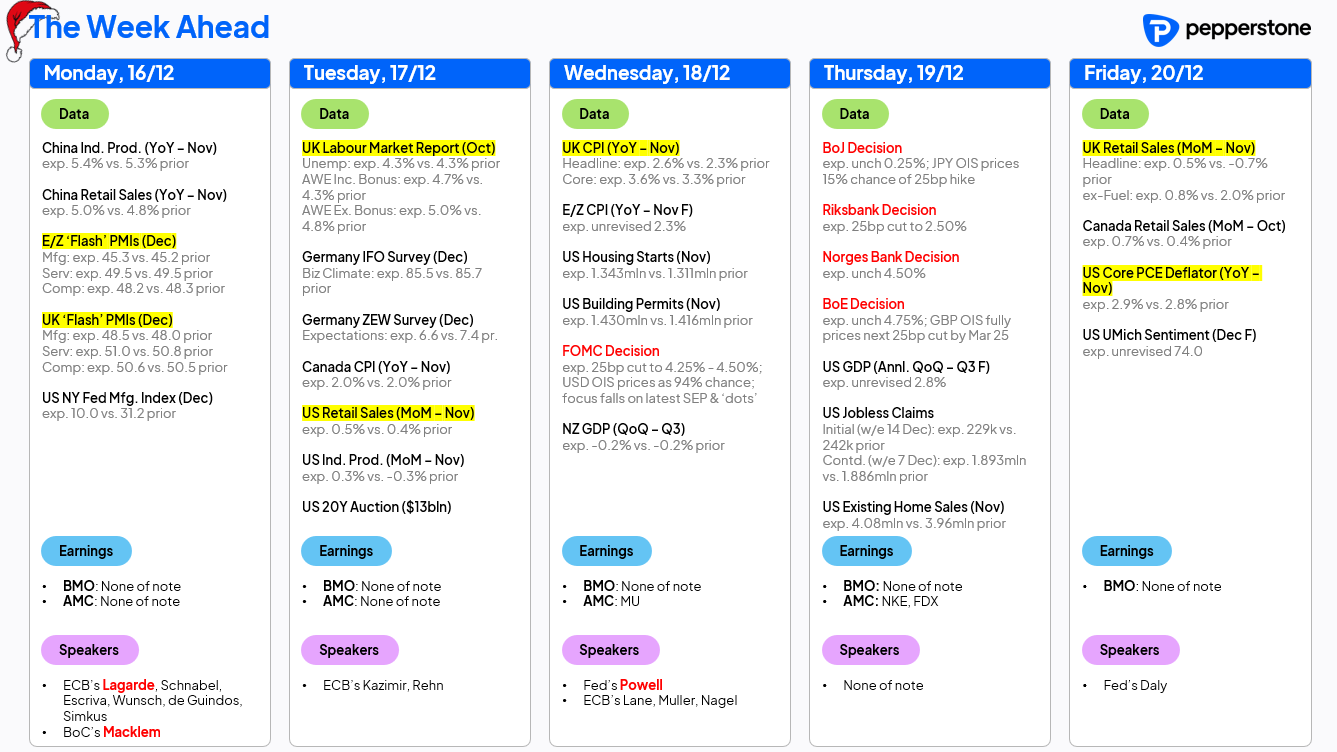

Chancellor Reeves’ plan to get the country growing again has thus far seen HM Treasury relentlessly talk down the economy during the summer, before then slamming the brakes on the recovery in the autumn via the biggest tax raising Budget ever, in nominal terms. A big week for the UK economy awaits – with the latest PMIs, jobs, inflation, and retail sales figures all due – though it’s tough to imagine any of those providing much cause for optimism, or deterring the BoE from holding Bank Rate steady at 4.75% on Thursday.

Elsewhere, the JPY also caught the eye, after further sources reports, this time from Kyodo, indicating that the BoJ are likely also to keep policy steady this week, instead delaying the next 25bp hike until early-2025. Predictably, the yen softened, as USD/JPY shot towards the 154 figure, with further JPY weakness the path of least resistance for the time being. This is especially the case considering that the BoJ’s window to tighten further is rapidly slamming shut, though I’d be reluctant to pile back into carry trades just yet, especially with vol likely to be considerably higher next year, as Trump returns to the White House.

Other G10s had a quiet end to the week, with the greenback meandering around the 107 figure, while the EUR chopped around $1.05, as participants were predictably unperturbed by the usual post-decision deluge of ECB speakers. EUR OIS pricing a 50/50 chance of a 50bp January cut seems about fair for now.

Away from FX, it was a ‘day of two halves’ on Wall Street, with solid overnight gains after impressive Broadcom earnings fizzling out as the day progressed, seeing the S&P 500 close flat, as the index notched its first weekly loss in three. I remain an equity bull, with seasonality of course also favourable at this time of year, though would question the degree of conviction that participants may have in buying the dip at this juncture, with the S&P up 30-odd% YTD, and with just a handful of trading days left this year.

That sort of environment can be a febrile one for ‘weird’ market moves, and that is exactly what we presently see in Treasuries. Friday was another day of selling pressure across the curve, with the belly underperforming. Still, it’s the long-end that’s particularly interesting, with benchmark 30-year yields having risen 30bp over the last week, north of 4.60%, for seemingly no reason at all.

At risk of spuriously pinning a narrative to the price action, perhaps this is some of the ‘Bessent Bid’ being unwound, with soft auctions perhaps also helping the selling along. Whatever the catalyst, with a hawkish 25bp cut likely on the way from the FOMC this week, bond bulls might not find any relief soon.

That Treasury sell-off, though, has been bad news for gold, which once again appears to have lost its shine. The yellow metal slipped over 1% on Friday, having failed once again to break above the November highs around $2,720/oz. Hence, we return to playing the range between the 100-day moving average to the downside, and the 50-day moving average to the downside, albeit amid signs that the bears are trying to obtain the ‘upper hand’.

LOOK AHEAD – Here we are then, the last ‘proper’ trading week of the year – we made it!

Don’t celebrate just yet, though, as the week ahead is a monster one, as the below calendar shows. Five G10 central bank decisions lie ahead – the FOMC should cut 25bp while building more flexibility into the policy outlook for 2025; the Riksbank will also cut 25bp, keeping time with the ECB; while, the Norges Bank, BoE, and BoJ will all hold rates steady.

On the data front, it’s a busy one here in the UK, as alluded to earlier on, with the figures all likely to reinforce the ‘stagflation-esque’ backdrop that seems set to dominate next year. More broadly, the latest US retail sales report stands as the calendar highlight, with risks to consensus expectations likely tilted to the upside, owing to indications of spending having been particularly strong over Thanksgiving. PMIs, a boat-load of eurozone sentiment surveys, plus CPI and retail sales from Canada, are also worth a look over the next five days.

Then, once we’re through all that, we can finally all put our feet up.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.