- English

- عربي

Today will be a far more insightful day though, with markets having now converged and we should get a better gauge on whether traders continue to liquidate. If I look at the A50 futures, we see price 1% higher than yesterday’s China A50 index cash (CN50 on MT4/5) market close, suggesting a modest gain for Chinese markets, while USDCNH has tracked sideways through US trade and we should see a fairly stable CNY fixing.

We also see S&P 500 futures and Aussie SPI futures up smalls from the ASX 200 close, so we should see Asia open on flat note, although I still feel the moves in copper and crude lend to traders fading the open. We shall see, but its day of watching the RBA and US politics, and I focus on these below in 10 things that have caught the eye this morning.

1) Crude is clearly not buying the better feel to equities, closing 2.8% lower at $50.11 and pulling into a technical bear market. Scuttlebutt that China’s demand for oil will fall by some 3 million barrels a day (or 20%) at the heart of the move. Talk now that OPEC, and Russia, will confirm an emergency meeting to address supply is not supporting.

2) Copper is also not finding any love either, with CME copper -0.3%, while the Bloomberg commodity index looks to be closing at the lowest levels since 2016. Not great for inflation expectations, which are falling.

3) The S&P 500 may have rallied 0.9% but vol traders are still expecting reasonable moves in price, with the VIX index at 17.9%, while AUDJPY 1-week implied vol remains above 10%

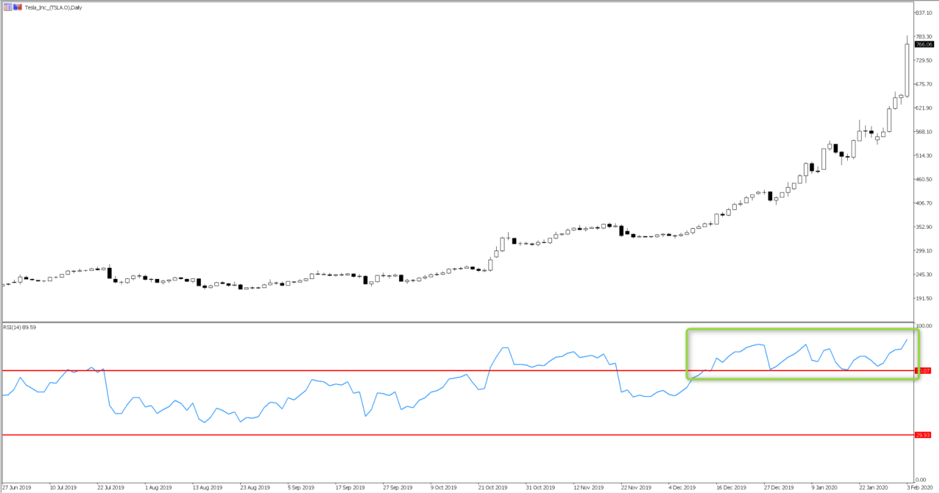

4) Despite the moves in commodities, the S&P 500 materials sector is the star performer +1.5%. That said, at a single stocks level, all the focus has been on Tesla, with the stock having its best day since 2013, currently up 19%, with traders compelled by several bullish upgrades to price targets. News from Panasonic has also inspired, with the firm saying they had turned profitable in their jointly owned (with Tesla) battery plant. Tesla is up 161% since the gap higher on 24 October and showing why an RSI above 70 is never a reason to short an instrument in isolation.

5) GBP sellers delight, with the pound sold vs all G10 currencies. Traders not feeling the love between Britain and the EU as they discuss the future relationship. GBPUSD is eyeing a bearish daily reversal, offered into 1.2983, and eyeing a test of 1.2960 horizontal support.

6) Petro-currencies (non-LATAM) are also attracting good sellers and moving into key levels – USDNOK eyeing a firm break of the 29 October high of 9.3056. USDCAD into the 1.3300/50 supply zone

7) The USDX is gaining 0.43%, with the USD gaining against all G10 currencies on the day. US ISM manufacturing index printed a six-month high at 50.9 vs 48.5 expected, with new orders smashing consensus at 52.0 (vs 47.7). Good numbers, but can the trend last given the likely impact of the Coronavirus?

8) Moves in the US bond market were led by the front-end, with US 2-year Treasury +4bp, resulting in a slight flattening of the 2s vs 10s curve. The implied probability of a cut at the April FOMC meeting has fallen from 58% to 42%.

9) AUDUSD remains largely unchanged, tracking a range of .6707 to .6682 on the day and eyeing a closing breach of the October low of 0.6671. All eyes on the RBA meeting at 14:30 AEDT and while the market puts a 19.7% chance of a cut, the question is whether they open the door for a move in March. With RBA governor Lowe speaking tomorrow, I would be looking to sell into rallies into 0.6730.

10) US politics takes focus, with the Iowa Democrat caucus due to take place through Asian trade. It's unclear when the results will actually materialise, as there seem to be issues with the phone app they are using for counting the votes. Bernie Sanders remains the massive favourite to take Iowa and the frontrunner to take the Democrat Nominee. Whether this event is a volatility event is unclear, but I do feel the market is under-pricing a Sanders nominee.

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.