- English

- عربي

Analysis

The ‘wall of worry’ that riskier assets must climb is a large one – including a range of factors such as the fallout from the debt ceiling resolution, the possibility of further Fed tightening, slowing economic momentum, slower earnings growth, and many more issues besides. However, thus far at least, the stock market has been able to deftly navigate these potential hazards.

Having been trapped in a relatively tight range since last summer, the S&P has finally made a closing break above 4,200, holding the level on a re-test, implying that we may at long last be about to breakout of what has been a painfully long rangebound spell.

The tech-heavy Nasdaq tells a similar story of breaking out of the range that has held for some time, with the index having embarked on a rather aggressive uptrend, albeit one that looks to have begun consolidating just shy of longstanding resistance at 14,500.

Despite the unarguably bullish price action, supported by the aforementioned technical breakouts, there are plenty who don’t want to believe the rally. Chief among the bears’ concerns appears to be the lack of breadth – i.e., the idea that the rally is being fuelled by a small number of stocks, with the majority of an index’s constituents not joining in with the headline gains.

The S&P’s performance evidences these concerns, with just 179 of the 503 constituents (approx. 35%) having delivered a positive return over the last three months, despite the broader index having gained 6% over that period. A similar theme is evident on a year-to-date basis, with the S&P’s outperformance over an equal-weighted version of the index being the vastest since the late-90s.

_Daily_2023-05-31_15-52-54.jpg)

As with the last time similar concerns were raised over narrow market leadership, we again see ‘big tech’ leading the way higher, with the sector having gained almost 35% YTD, along with a 32% gain for communications, compared to a roughly 10% gain for the index as a whole.

Of course, there are some idiosyncratic factors at play here. Nvidia, for instance, the S&P’s best performer this year, has been seized upon by traders as the best way to capitalise on the AI frenzy currently sweeping financial markets, having now become only the 9th firm in history to eclipse $1tln in market cap. Although Q1 earnings were, once digging into the release, rather subpar (revenue down 13% YoY, EPS down 22% YoY), the buying frenzy has continued.

_Da_2023-05-31_15-38-23.jpg)

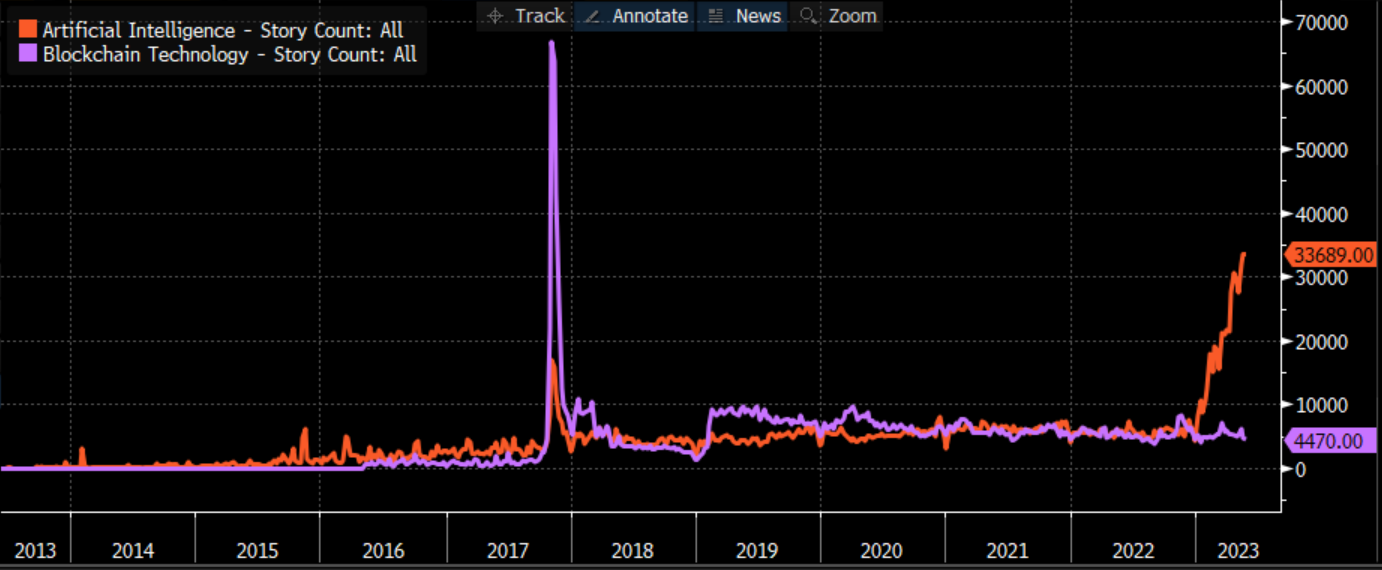

The AI mania, which kicked off with the release of ChatGPT last November, has some similarities with the blockchain frenzy from a few years ago. In terms of media traffic, at least, we are still some way off that particular episode, though the utility of each is probably similar at this stage.

For traders, however, the key question is whether narrow market breadth poses a major risk to the broader market rally. Markets have been able to shrug off periods of minimal upside participation in the past, and look set to do so once more.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.