- English

- عربي

A traders’ week ahead playbook – Will a calm descend after a cross-asset storm?

The crypto markets work through their MF Global moment, with investors running the ruler over the exchanges and many questioning if we see another run on an exchange early this week. It feels ominously like we will see some further big changes in the crypto exchanges, but whether this proves to hold systemic challenges through broad financial ecosystem seems remote. Over the weekend we’ve seen a heavy tape in crypto, with Bitcoin reaching 16,423 and in some capacity it’s a surprise it's not even lower – it's easy to think traders will be shorting into rallies early this week.

Crypto aside, it was a momentous week from a cross-asset basis – the combination of China announcing changes to its Covid zero policy, a below consensus US core CPI read and even news that Russia had pulled troops out of Kherson, were enough to cause some incredible moves – the USD caught the attention of clients, falling a monster 4% on the week, with the weekly declines on par with downside last seen in March 2009. It is a USD play though, and other G10 currencies are really moving as one, but at different speeds – pick your beta!

Are there more legs in the USD sell-off? It feels like the path of least resistance is lower, and some are targeting the 200-day MA in the USD index at 104.48 and many have noted the limited amount of tier 1 data to drive, and we must wait until 2 Dec to get the US payrolls report, and while we do see a raft of Fed speakers this week, they are largely reactionary – the data leads.

Importantly, US 5yr real rates have broken the bottom end of the 1.5% range, while the terminal fed funds pricing has pulled back to 4.9% - both are a USD negative but overlap the USD and the two variables suggest the USD move is a tad overdone. We also see the USDX having pulled 2.3% away from its 5-day EMA – a 4 standard deviations move over the long-term – so while the USD sell-off is justified, the prospect of mean reversion is elevated.

(Daily chart of USDCHF)

USDCHF gets less attention from clients than EURUSD, GBPUSD and AUDUSD, but this is where we’ve seen the big percentage change last week and price is in absolute freefall – the epitome of catching a falling knife. we can see the USD has pulled away much more aggressively – positioning will do that.

Equities are on fire – certainly, the GER40 and NAS100 – but China-sensitive plays, namely industrials are killing it, as you’d imagine given the tweaks from China on Friday. Consider that on Thursday we saw $1.7t added to the market cap of the S&P500, the third highest amount ever, and while much of this was shorts covering and position re-adjustment from systematic players, it feels like the mountain of cash on the sidelines is looking at the market and fearful of a further melt-up into a seasonally strong period - The pain trade is higher, although we do have options expiry on Friday and that may have implications on equity volatility.

The NAS100 is where clients are focused, with good attention on the HK50 too – the breakout in the NAS100 looks promising and some will be holding for 12k, with the 200-day MA a possible secondary target at 12,672.

After such a big move in copper, equity, and USD the chance of a pause to catch a breath is elevated – it makes for compelling trading conditions as new trends emerge and momentum takes hold. Markets are never dull, and once again having an open mind to change would have served you well.

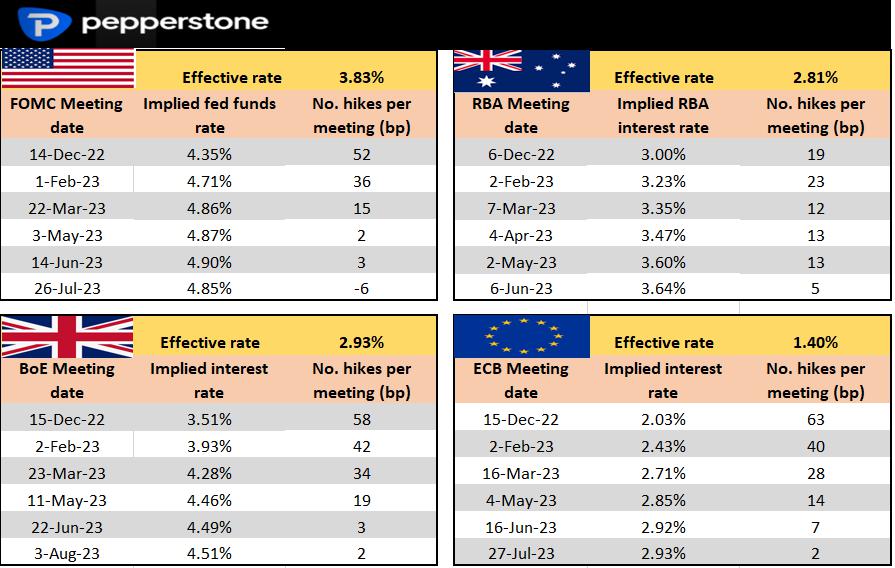

Rates Review – We see what’s priced the upcoming central bank meeting and the step up (in basis points) to the following meetings. For example, we see 52bp of hikes priced for the 14 Dec FOMC meeting and a terminal rate (June 23) of 4.9%.

Central bank speeches:

14 Fed speakers – the highlight for me will be VC Brainard’s speech on Tuesday (03:30 AEDT) as she discusses the economic outlook – a good chance to assess how Brainard sees policy given the lower core CPI print.

5 BoE speeches – notably BoE chief Bailey testifies to parliament (17 Nov 01:15 AEDT)

14 ECB speakers – notably ECB President Lagarde speaks on Thursday at 02:00 AEDT

Data to focus on above others (times in AEDT):

Monday

Tuesday

China high-frequency data (15 Nov 13:00 AEDT) - industrial production (consensus is 5.2%), retail sales (0.7%) and fixed asset investment (5.9%) – the market remains fixated on last week’s Covid pivot, with Chinese authorities making some key changes last week and showing a greater interest to support growth. Not sure these will be market moving, but it feels like traders are seeking out good news, so better numbers may resonate with AUD and HK50 buyers.

UK employment change and weekly earnings (18:00 AEDT) – The market expects the unemployment rate to remain at 3.5% and earnings to fall to 5.9% (from 6%) – shouldn’t move the dial on the UK100 or GBP too intently.

Wednesday

Aus – Q3 Wage Price Index (16 Nov 11:30 AEDT)– the market sees Aussie wages rising 0.9% in Q3, or 3% YoY – this is a big jump from the Q2 print (+2.6%), but it’s hard to see this moving the AUD too intently or moving pricing for the 6 Dec RBA meeting past 25bp. The AUD is moving more in alignment with equity markets and copper, which is up +16% in the past 6 days and testing $4.00lb and the 200-day MA – perhaps this is a level for scalpers to have on the radar.

UK – CPI inflation (16 Nov 18:00 AEDT) – the market consensus is for UK consumer prices to rise 10.7% YoY in October – the UK rates market prices 58bp of hikes in the Dec BoE meeting, so the inflation print can affect this pricing. GBPUSD is again trading as a risk barometer, and interest rates are having less of an effect – so as go equity, as goes cable. Clearly a solid breakout on the daily timeframe and while overbought, the GBP bulls will be long and strong for 1.2000. Clients are mixed on the near-term path for GBPUSD, with 56% of open positions held short.

Thursday

Aus employment report (17 Nov 11:30 AEDT) – the market sees 15k jobs to be created, with the unemployment rate expected at 3.6%. An unemployment rate above 3.7% may impact the AUD most vs the crosses, notably, on a higher unemployment rate we could see AUDNZD trade sub-1.0900. However, AUDUSD remains a play on the USD and global risk sentiment.

US – Oct retail sales (17 Nov 00:30 AEDT) – the consensus estimate is calling for 1% MoM and for 0.3% in the ‘control group’ element - the basket of goods that feeds directly into the GDP calculation. Retail sales is typically not a market mover, and while the market is more focused on the labour market and inflation, this time around a weak number could keep the downward pressure on the USD.

UK govt fiscal statement (17 Nov) – talk of a big fiscal tightening worth some £50-60bn annually over the coming five years has been widely discussed – this equates to just under 2% of GDP. Predominantly the expected measures from public spending, but there could be sizable tax hikes too – the market likes a more prudent govt, and it's unclear where this becomes a vol event for the GBP – perhaps a greater weight towards tax hikes could be a modest GBP positive as it would impact future growth less.

EU CPI (17 Nov 21:00 AEDT) – the market expects EU headline inflation of 10.7% YoY and 5% YoY on core (unchanged) – again, EURUSD is another risk play and tracks closely to the NAS100. Yet, while we see 63bp of hikes priced for the Dec ECB meeting, we’d need to see a big beat/miss to cause too much of a rethink on the pricing for this meeting – Perhaps one for the EUR crosses, but the cleanest reaction may be seen in the GER40, where we see real upside momentum in the EU equity markets – for example, we see the GER40 up 21% since the 3 Oct low. After this sort of a run, it's hardly a surprise to see 78% of open positions (held by Pepperstone clients) held short now.

Canada CPI (17 Nov 00:30 AEDT) – the market expects headline CAD CPI of 7% (from 6.9%) – markets currently price 32bp of hikes in the 7 Dec BoC meeting – the CAD has lagged other G10 currencies in the recent risk-on rally, with CADCHF shorts working well and testing solid multi-year support.

Friday

Japan – National CPI (10:30 AEDT) – the market sees headline inflation rising to 3.7% (from 3%) and core (ex food and energy) to 2.4% (1.8%) – while this would be the highest level of inflation since 2014 the BoJ should remain steadfastly dovish and should not lead to a change of heart on policy.

US – Oct leading Index (19 Nov 02:00 AEDT) – the market expects a reading of -0.4%, where a weaker print could push US bond yields lower and push USDJPY towards 137.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.