- English

- عربي

Analysis

Tick, tick boom... Could the USD be set to cause havoc to markets?

The bear trend in the USD has been in place since May and short USD exposures are a now such a huge consensus call. It's easy to see why, and when we look at the monthly chart of the DXY we see USD typically troughs after a seven-year decline. If the trend is to continue, then it suggests the USDX would be trading closer to 60 and one can only imagine the evolution of currency wars if EURUSD was trading north of 1.3500.

A weaker USD has had a lit a fuse under commodity markets, and along with short 30-year US Treasuries and equity markets (such as the JPN225) has been the go-to hedge against rising inflation expectations. In the bond market, we can look at the rise in longer duration US Treasuries, with the 10-year moving from 50bp in August to 111bp on Friday. This has been driven in part by a reduction in term premium which has risen to -18bp and if this momentum continues term premium may turn positive for the first time since December 2018.

We also see 10-year inflation expectations, or the so-called ‘breakeven’ rate, moving to 2.07%. This is effectively the difference seen between nominal 10-year Treasuries and 10-year TIPS (Treasury inflation-protected securities) – ‘breakevens’ measure expectations of average inflation over that defined period. At 2.07% the market is sensing impending inflation and this, in turn, has had a positive feedback loop into equities and commodities, and as equities have rallied then the risk-on vibe has pushed the USD lower.

Breakeven rates focus on CPI as opposed to core PCE (personal consumption expenditure) inflation, which of course the Fed set policy by as part of their policy mandate. However, the general rule is that PCE inflation typically sits around 30bp lower than CPI. So, if 10-year breakeven rate rises further to 2.30%, then it's signaling the market sees the Fed meeting its policy objective for average inflation over 2%. This would be a significant development and could get a lot more focus from Fed speakers, who may turn more hawkish at the margin. This would be a clear USD positive as it accelerates the view that the Fed could look to taper its asset purchase program in late 2021.

One suspects that 2.30% may be the high mark in breakeven rates, so the risk is that we may be getting close to peak inflation expectations. This is important because when we adjust nominal bond yields for the breakeven inflation expectations, we get the ‘real’ Treasury yield. This is one of, if not the most important, instruments to look at by way of its influence on global markets and falling real yields have been at the backbone of the reflation trade.

If nominal Treasury yields continue to gravitate higher, and we see inflation expectations (breakevens) flatlining or even falling then real yields are going to turn higher and I suspect this will be the case in the coming weeks and traders should be prepared for it.

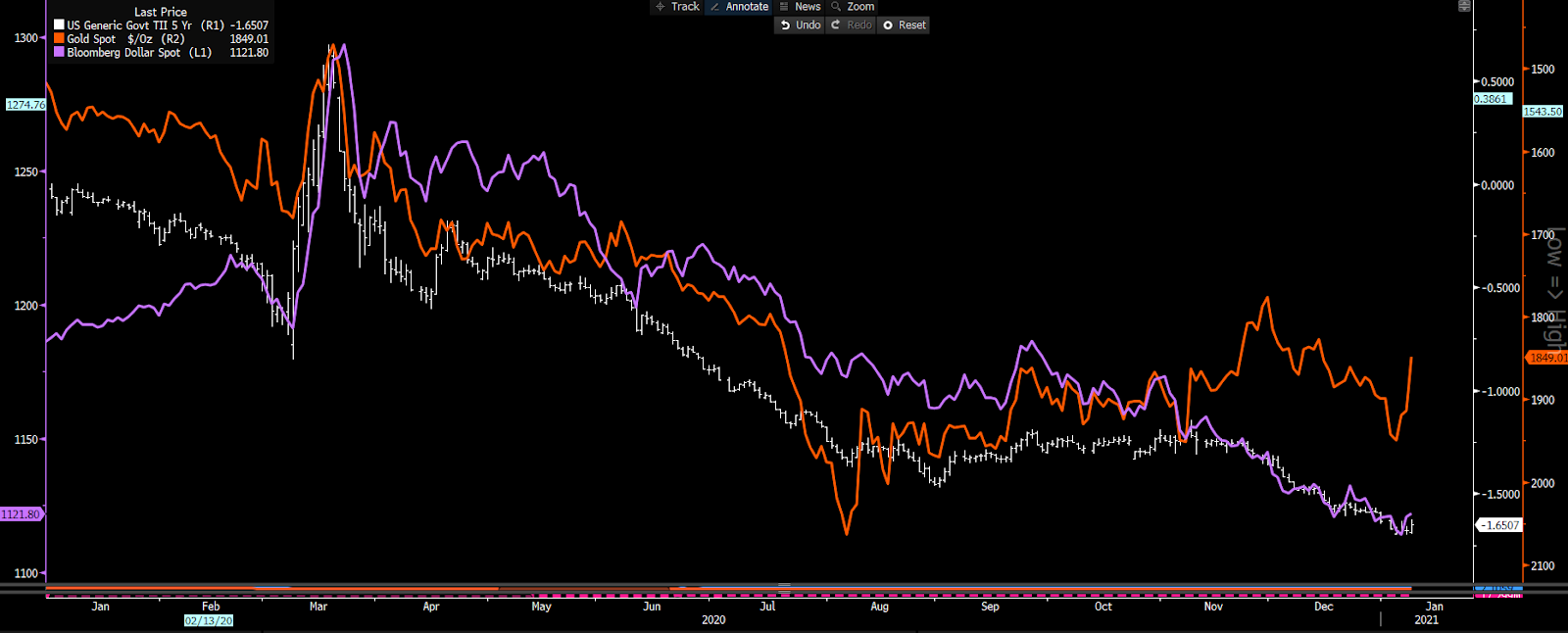

Purple – USD index, Orange – gold (inverted), white – US 10-yr real yields

A rise in real US Treasury yields would have a pronounced effect on the USD and would negatively impact the second derivatives of the weaker USD trade, and represent a temporary set-back for the inflation trade that has become a major consensus position.

Consider that sentiment towards the USD is currently shot to pieces and the USD simply cannot find a friend. Positioning is clearly skewed short in currency future and the daily sentiment index (DSI) has reached extreme readings. When this sentiment shifts it could be quite violent.

US exceptionalism to re-surface?

Let’s also address the US exceptionalism story and the idea that a further $1 trillion in fiscal stimulus, likely to be rolled out over the coming two to three months, will add some 2 percentage points to US growth over the next two years.

I wrote in December that capital will flow to where the growth is and while we are seeing some worrying trends in the US, we also know the vaccine is being rolled out, fiscal stimulus will be aggressive in supporting economics and the Fed is still incredibly accommodative. This could make the US attractive relative to other major economies as an investment destination and promote USD short covering. Conversely, if the Biden administration looks at measures post-inauguration (20 January) to forge a far more stringent stance to control the virus then this could cause a risk-off theme through markets – again promoting higher real yields and a wave of USD short covering.

However, its moves in US real Treasury yields that interests most here. We saw on Friday a mere 6bp rise in real US yields (or TIPS) and the USD rallied 0.3% and gold had its biggest fall since 9 November with silver losing 6.3% and copper falling 0.6%. Is this a sign of things to come? I suspect it is and equities, while incredibly strong and resilient, may also see higher volatility.

Like many, I remain a USD bear as part of a longer-term macro thesis and believe in reflation for 2021. However, in the near-term I am watching for a reversal in real yields, and the positive effect that will have on the USD and any repositioning it could have huge implications for gold, copper and the reflation trade that is now so consensus

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.