- English

- عربي

.jpg?height=93&quality=100)

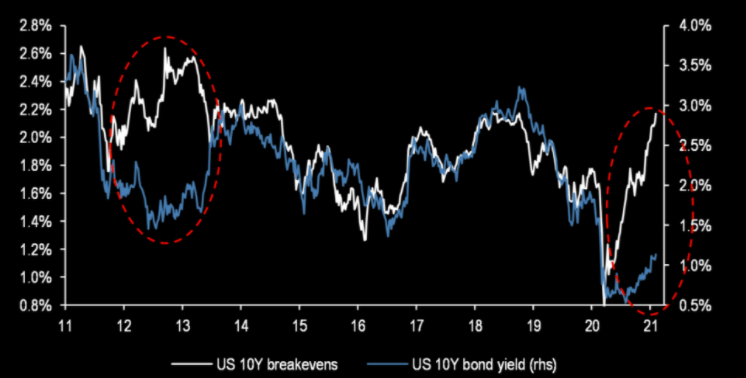

Maybe it was jubilant Tampa Bay traders celebrating their team’s win or more likely it was Janet Yellen’s push for rapid stimulus and how the US could see full employment by 2022 if the relief package delivers. The poor jobs numbers on Friday have clearly been brushed off as a speed bump rather than roadblock as traders begin to see some light at the end of the pandemic tunnel. The weak job numbers provide more support to the rapid rollout of a large fiscal stimulus package, which the street now sees being roughly $1.5 trillion (upgrade from $900bn previously). The blue sky scenario looks to be taking front and center of traders’ minds, however, there are two risks which could rock the boat. There was some concerning virus news over the weekend, regarding Astra Zeneca’s reduced efficacy against the South African variant in terms of mild/moderate illness. The jury is still out on more severe cases. These developments will need to be monitored closely. The other risk is a too rapid rise in yields, break-evens and yields usually track closely and a large divergence has opened up. Equity markets valuations are certainly not on the cheap side and if rates start to move higher aggressively then financial conditions will tighten and we could see a price correction.

Source: JP Morgan

FX:

DXY – The dollar is giving back some of its recent gains and has moved below the 91 level. For the bulls it’s important that price holds the small ascending channel line and pink 21-day EMA around 90.7. The US exceptionalism story is making a comeback as their vaccine rollout is accelerating rapidly, combined with a nice shot in the arm from fiscal stimulus. This translates to faster economic growth and therefore better prospects for the domestic equity market which will see more flows and the benefit the greenback. If inflation out on Wednesday beats expectations we could see yields move higher and the dollar catch a bid to continue its upward trend. The big dollar short versus the euro still makes no sense give the problems the continent is facing. We did see a slight unwinding of those shorts over the weekend, but it is still very sizeable.

EUR – Super “Mario” Draghi, the former top dog at the European Central Bank is on course to form a new Italian Government after he received the backing of the Five Star Movement and Matteo Salvini’s League. So it looks almost certain that he’ll become Prime Minister. Investors have responded well to this news as indicated by the BTP-Bund spread which continues to go lower and lower. On the technical front the EUR/USD has changed direction over the last two days and is now comfortably above the 1.20 level. However, there is some resistance which will have to be negotiated around where price is now – 1.205 and the pink 21-day EMA is above at 1.21. Net specs positioning is still very elevated and one only has to remember the unwinding back in Q2 2018 to see how a long euro position can lead to serious pain.

Source: Bloomberg

GBP – After last week’s BoE meeting where negative rates where swatted away and the bank could be described as fairly hawkish, Cable has been firmly bid and is pushing right up against the all important 1.371 -1.375 resistance zone. The last 3 days has seen some bullish price candles on the chart. Vaccine rollout targets look to be met with ease and against the euro cross GBP is still in the driving seat as the vaccine spread between the two widens. We have UK GDP data out at the end of the week which shouldn’t be a market moving event unless there is a big beat/miss.

.png)

Yen – The USD/JPY seems to be suffering from some high altitude sickness as the dark blue 200-day SMA creates some downward pressure. Also, the RSI has moved back below overbought territory. If US yields continue to move higher and the spread with Japanese bonds widens further then 106 starts to look likely on continued USD strength.

Commodities:

Oil – Oil has been on a rip of late as mobility starts to increase demand and the supply cuts from OPEC+ keep the demand supply picture well balanced. The futures curve has taken on the shape of backwardation (higher spot prices vs futures prices) and supports the bullish sentiment around the black liquid, driving it back to Feb 2020 levels. One can express a view via our share offering in Chevron and Exxon or through our direct oil instrument.

Gold – Gold has put in two massive bullish candles over the last two days in what can be seen as an inflation hedge/reflation trade. A slightly lower dollar and real yield will be helping the shiny yellow metal too. It’s at an important crossroad now, hovering just above the uptrend line from March. False break or rejection of trend break?

Equities:

All the cyclical sectors are having a great day, namely Materials, Energy and Banking. Both the Nasdaq and S&P are up, but it’s the Russell 2000 which is stealing the show on the back of the reflation rotation. Will we be saying S&P 4000 soon? There is still quite a bit of room left before RSI reaches overbought territory.

Cryptocurrency:

Bitcoin has made a fresh ATH as Tesla buys $1.5B in bitcoin and will start accepting Bitcoin as payments for cars. The digital currency is up almost 15% with the RSI just crossing the RSI overbought line. Will traders try to target $50k or will any upset on the risk front see an equally large sell-off. Ethereum is marching higher too eyeing the $2000 level as price goes almost vertical.

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.