- English

- عربي

Markets Kick Off the Week: S&P 500 Eyes 5900, USD Mixed, Gold Awaits Breakout

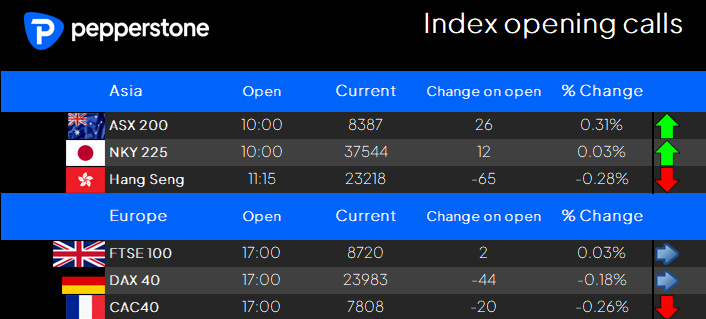

S&P500 and NAS100 futures have reopened largely unchanged (at 8am AEST) and with true participation set to build into EU and US trade we look to see how the big hitters come back and deal with a market that recently found good buying support at the 200-day MA and now trade above Friday’s high. After a precarious/bearish technical setup was building, with signs that volatility hedges were seeing increased demand, an element of the recently initiated bearish positioning would have been wrongfooted by this move higher and therefore may either be forced to cover or to martingale the position and add shorts into strength.

Of course, that action depends on the type of strategy and objective the trader adopts, as adding to losing positions comes with significant risk and is not an approach I would personally take on. If this market tells you anything is that we must be nimble and it rarely pays to question the holistic set of views, opinions and beliefs of the collective that are aggregated into the price.

The bull/bear case for US equity

If SPX500 futures can build through 5900 – and that may require US 10yr Treasury yields to gravitate lower towards 4.40% - then the prospect of a re-test of 5993/6000 (the 20 May high) will be there, and there are a number of reasonable kickers ahead with US durable goods, consumer confidence and a $69b 2-year Treasury auction in the mix – plus, we should see increased prepositioning ahead of Nvidia’s earnings (Wednesday after-market), with the options market implying a -/+6.8% move in Nvidia's share price on the day of reporting.

S&P500 longs know their risk, with the 100- & 200-day MA (5789 & 5804 respectively) recently offering a solid platform for US equity upside to build – subsequently, should US equity futures reverse course and result in a solid daily close below these long-term averages, and it wouldn’t surprise to see longs admitting the position isn’t working and cutting. These fast money players may indeed look to add on a break of 5900 for a move into 6000 – this idea resonates with me, and as is the way in all parts of our lives, doing more of what’s working typically leads to good outcomes.

Those in short US equity risk exposures would naturally see the opposite to play out and hope that the collective wisdom in the market sees the world through a more pessimistic lens and that US cash Treasury yields (reopen at 10am AEST) resume their selloff – driven by poor demand in the US 2YR treasury auction, and higher term premium, taking the 10yr back to 4.60%. Again, expect shorts to start dialling back the closer we get to 6000 while adding to bearish exposures on a convincing break below the 200-day MA.

Do all roads lead to a weaker USD?

The USD gets the attention of clients - where outside of gold, which is almost always our most actively traded market – we see the highest open interest in client positioning in EURUSD, GBPUSD, AUDUSD and NZDUSD. The aggregation of all flows sees clients modestly long of USDs, and while this skew goes against the growing chorus of calls from FX and macro strategists that the USD is set for a structural bear market - the position from clients is more to play a near-term counter-rally, but one where the net position could likely switch dynamically.

Certainly, we eye the dally set-ups in the USD pairs, with AUDUSD getting strong attention, with the daily chart portraying the spot rate ominously poised to break out topside of the 0.6500 to 0.6350 consolidation range it has held since mid-April. NZDUSD also eyes a similar holding pattern, with the top end of the range at 0.6000, with traders skewed to fade the move into the upper range – a breakout, ahead of tomorrow's RBNZ meeting could be telling. EURUSD rallied into 1.1419 post Trump’s push back to the 50% tariff start date but kicked back to 1.1370 as European trade rolled on, where the pair then held a tight range with US players away.

In a way, all roads have led to a weaker USD. Higher perceived US deficits have raised concerns about increased future Treasury issuance, pushing up term premium and seeing people migrate away from the USD. Concerns of weaker US growth in 2H25 see's USD sellers. Tariff risk resurfaces, USD trades lower and when the tariff risk and the implementation date is subsequently pushed back, again we see the USD lower.

Gold has tracked EURUSD for much of the session, and will be eyeing moves in USTs through trade, with flows in China into Shanghai gold futures and gold ETFs also a factor that could filter through to the CME gold futures and spot gold. One to watch, with spot gold needing a break of $3365 (last week's high) to set off a resumption of the short-term trend from the 15 May lows.

Good luck to all.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.