- English

- عربي

In fact, we saw one of the most impressive turnarounds for years, with big tech finding form and shorts capitulating (the Goldman Sachs high short interest basket closed +7.4% w/w), and the S&P500 and NAS100 ultimately had the best weekly performance since November 2023.

S&P500 futures weekly chart and % change

US cyclical equity may have underperformed the more defensive sectors, but it didn’t hold the respective indices back and after five straight days of upside momentum in US large-cap indices, the bull’s now eye key resistance levels, with some solid wood to chop to get to the all-time highs. If the buyers see the right outcome from the key event risk due this week, the upside levels to watch remain 20,025 in NAS100 futures, and 5669 in S&P500 futures – if the bulls can push through these levels, then the chase higher could be on.

Levels to define equity risk

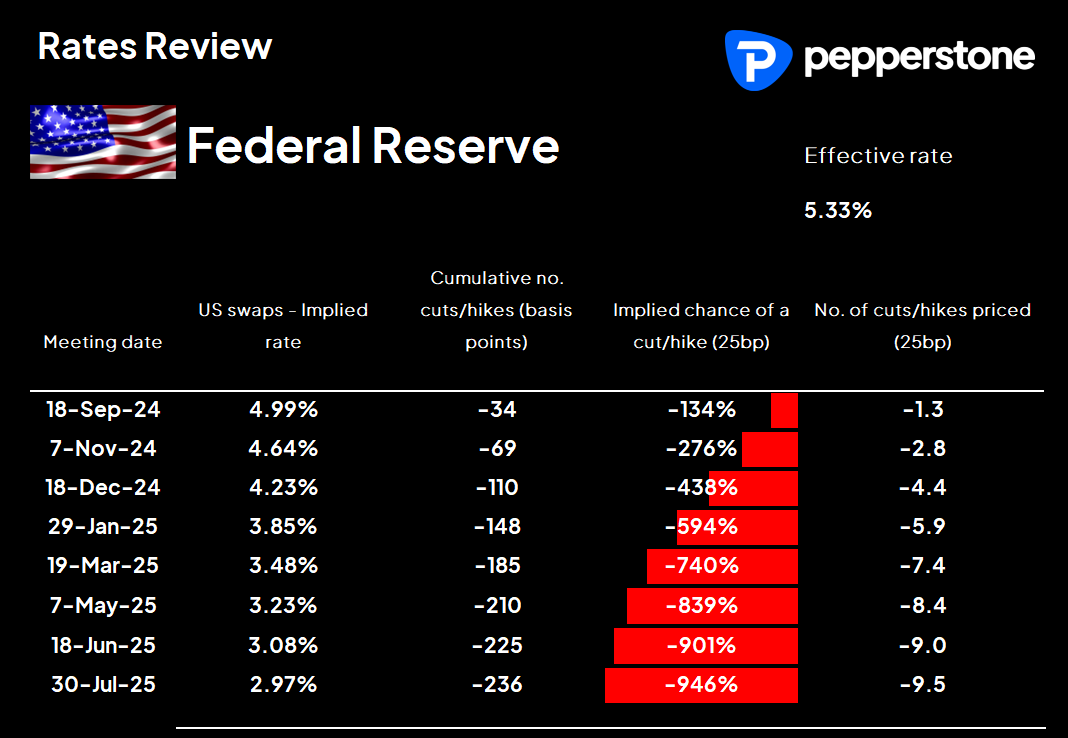

Should we see better selling flows, I see risk in S&P500 futures defined below the 100-day MA (5433) and then below 5394, where a breakdown would suggest short positions, on the higher timeframes, getting increased traction. US Small caps (the Russell 2k cash) lagged for most of the week, but caught a solid bid on Friday, closing +2.5%, and we’ll see if the momentum can build as we roll towards US retail sales and the all-important FOMC meeting. In the US Treasury market, the US 2yr fell 6bp on the week to 3.58%, with US swaps closing out the week implying 34bp of cuts for this week's FOMC meeting, and 110bp of implied cuts by December.

USD upside constrained by the falls in US Treasury yields The further reduction in US yields has held the pressure on the USD, notably vs the MXN, CLP, JPY, and AUD. USDJPY has been the cleanest expression of the fall in US bonds, with the pair closing at the weakest levels since July 2023, and while speculators are short and riding this lower, this trend is clearly one to align with. The big downside level to have on the radar is ¥140.25 (the 28 Dec low), where we saw USDJPY stop 3 -pips off this level on Friday, with buyers supporting – as we head into the week a daily close through ¥140.25 would likely open further downside.

EURUSD tested 1.1100 on Friday, but the sellers drove spot lower to close at 1.1075 –Subsequently, a break of Friday’s low of 1.1070 could result in a further move to 1.1040, as we look towards the key US data that could further influence, and to a lesser extent the army of ECB speakers due this week – a risk to be aware of, even if the ECB’s potentially truly dovish shift comes in October or November. EURJPY shorts seem a cleaner expression for those wanting to sell EURs, and with some hawkish risk due from the Norges Bank meeting (Thursday), EURNOK shorts also look interesting from a tactical perspective.

Can XAUUSD join gold futures above $2600?

The breakout in spot Gold (XAUUSD) has been well traded by clients, with $2600 now not far off. Gold futures in fact breached $2600 on Friday without too much resistance, although the accumulation did drop off markedly on the break, so conviction from the buyers did fall as we broke the big figure. On the week we saw a sizeable $654m of inflows into the GLD ETF and $282m into the GDX ETF (Gold miners ETF), which was the highest level of inflows into the GDX since November 2023 - so ETF buying was a bullish factor that needs to be accounted for. Adding to that flow, is talk that money managers have been better buyers of gold as a portfolio hedge, and they, in turn, have been the beneficiaries of what is a momentum trade, with gold futures driven higher by systematic momentum and trend buyers.

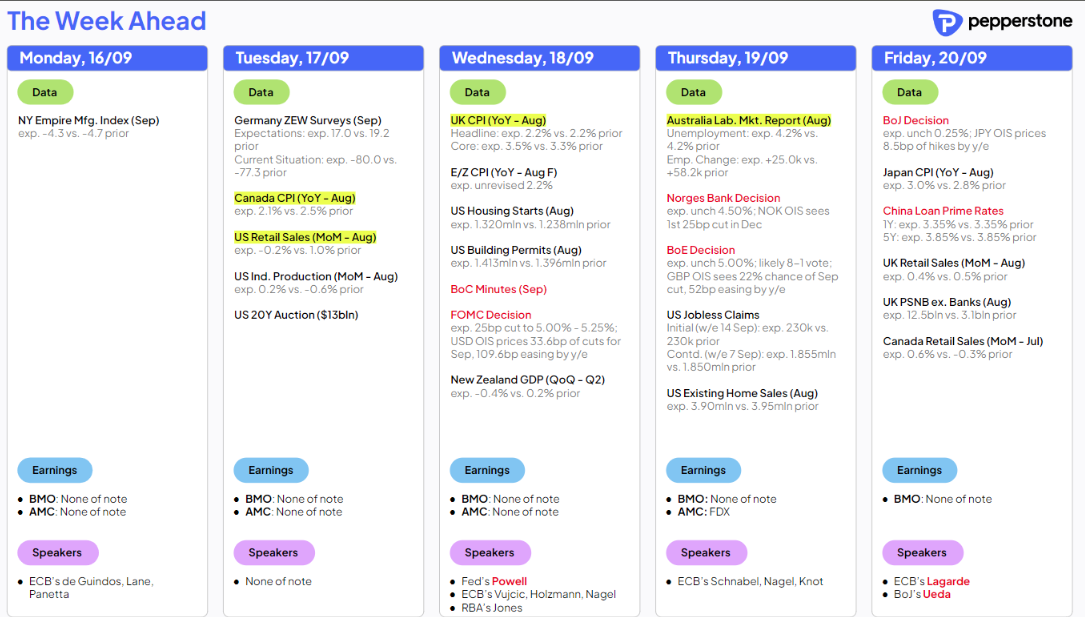

The key event risks to navigate this week:

US retail sales (Wed 13:30 UK / 22:30 AEST) – Could weak retail numbers affect the Fed’s thinking? It seems unlikely, and as such the volatility from this otherwise important data point may result in limited volatility. However, it could still validate those running short USD positions into the FOMC meeting.

The September FOMC meeting (Wednesday 7 pm UK / Thursday 4 am AEST) – After such lengthy and intense speculation the rubber finally meets the road, and the Fed will set the market straight on their collective thinking. There are just too many variables to make a clear-cut playbook over this event risk, and it is not as easy as thinking that the USD rallies/risk falls if we get ‘just’ get a 25bp cut – or conversely that the USD sells off/risk rallies if we get a 50bp cut. We need to also consider the Fed’s new economic projections and the new set of ‘dots'. The tone of Chair Powell’s press conference (30 minutes after the statement drops) will also be a huge factor, and whether there is the appetite for a series of big cuts if the labour market further deteriorates.

My own tactical bias for the Fed meeting is to stay out but to leave limits to sell USDJPY at higher levels on the day – this would allow for an initial spike higher if the Fed cut by 25bp, but then align if Powell does validate pricing for a 50bp cut in the November meeting. Given how much focus there is on the meeting cross-asset price action may get a little wild, so do manage risk accordingly.

UK CPI (Wed 7 am UK / 16:00 AEST) – UK swaps price a 25bp cut this week from the BoE at 22%, so with a high barrier for a cut, the CPI numbers may only result in small changes in swaps pricing and by extension the GBP. To get the GBP really moving, naturally, the outcome of CPI would need to be a significant deviation from the consensus.

BoE meeting (Thursday 12:00 UK / 21:00 AEST) – The strong belief is that the BoE maintains the bank rate unchanged at 5%. The split in the voting may result in a small move in the GBP, and whether it’s a 6:3 split or a more definitive 8:1 split, would send a signal of the urgency to ease again. Overall, I would have limited concerns about holding GBP exposures over the meeting, although there is a strong view the BoE ease by 25bp in November and December and the commentary may need to signal that pricing marries to their thinking.

BoJ Meeting (Friday – Asia afternoon) – Despite the rally in the JPY, the BoJ meeting will likely be a non-event for markets. Governor Ueda’s press conference later in the session will be more closely followed for signs the review process the BoJ has undergone since the July hike is progressing and for any clues of an appetite to hike again this year. Prior to the BoJ policy statement, we see Japan’s national CPI print (09:30 AEST), and again while unlikely to cause any major volatility in the JPY it could impact the pricing for a hike in December.

China data and policy rates – We watch to see if there is a negative reaction to the weaker-than-expected China data dump (released on Saturday) in the AUD on the FX open, as we will in copper and iron ore futures, and in the China equity indices. The trend in the CN50 index is firmly lower and unless we hear something new and substantial on a fiscal level – or that state-owned banks are asked to step in and support the equity market - then rallies will be sold and the trend is lower for a reason. We also see the PBoC making a call this week on the Medium-Lending Facility and the 1 & 5-year Prime rate, although given how cheap it already is to access credit or to refinance, I’m not sure reducing the cost of capital is the answer the market is looking for. With Chinese households and businesses increasingly looking to reduce debt, there just isn’t the appetite to invest and spend, and that needs to change.

Also on the docket, and data that could move specific markets – Aussie jobs (Thursday 11:30 AEST), Norges bank meeting (Thursday 18:00 AEST – on hold), SARB meeting (Thursday – 25bp cut expected) and Canada CPI (Wed 22:30 AEST).

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.