- English

- عربي

Stock Markets – FOMO and TINA…

Nearly everyone on Wall Street, and Main Street too has underestimated the strength of this year’s stock markets. Investors have been spooked by a myriad of headwinds and yet, the markets continue to set new records, including fresh highs on Friday in the wake of the announcement of an interim trade deal between Beijing and Washington.

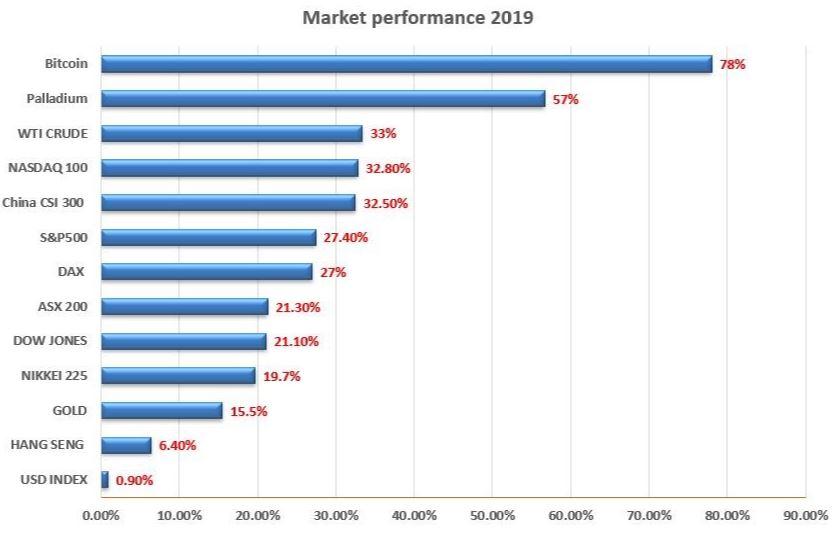

Equity indices are up year-to-date by more than 20% across most countries (with the noticeable exception of the UK) and the Stoxx Europe 600 has clocked the best year since 2009.

Of course, we had a broadly similar equity rally two years ago but that was fuelled by the then synchronised pick-up in global GDP – a classic risk-on story if you like. This time around, bonds and fixed income have also delivered solid returns with high single digit returns for euro area sovereign and high-yield debt among others.

So, this year’s story is all about the monetary policy (QE) driven rally, particularly fuelled by the Fed following last year’s Q4 sell-off. Indeed, one of the most striking aspects about 2019 is that it marks the fastest pace of central bank easing since the GFC. This has cushioned the blow of contracting global manufacturing, shaky business confidence and falling capital investment.

How much longer can central banks extend the business cycle and so confirm these stock market valuations? A de-escalation in US-China trade tensions and Brexit last week will help going forward but tariffs are still in place, uncertainty around US election cycle looms large while service sectors are worryingly fragile. Add to that a slowing Chinese economy and global disinflationary pressures and headwinds are still ever present.

The most recent policy meetings of both the Fed and ECB were encouraging for those looking to see the central bank safety net extended. Balance sheet expansion will be maintained which means with bond yields entrenched, the low yield environment will persist and favour stocks, plus strategies involving selling market volatility.

One other area which continues to support equity markets are stock buybacks. When companies buy their own stock, they reduce the number of shares on the market, inflating earnings per share metrics, which typically fuels the stock price. This year remains on track to be one of the most active on record, after companies spent a record $800bn buying back shares last year. The market has certainly got used to companies repurchasing their own shares and providing support to the market.

Stock markets are meant to have a record of pricing in today what will happen in the economy in the near future. Cautiousness remains a theme for next year especially as the S&P500 is on track to show a third consecutive quarter for negative year-over-year growth. But FOMO has been in full effect for some time now with historically low rates and persistent stock buybacks likely to keep stocks elevated. Perhaps we should use ‘TINA’ instead – There Is NO Alternative?

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.