- English

- عربي

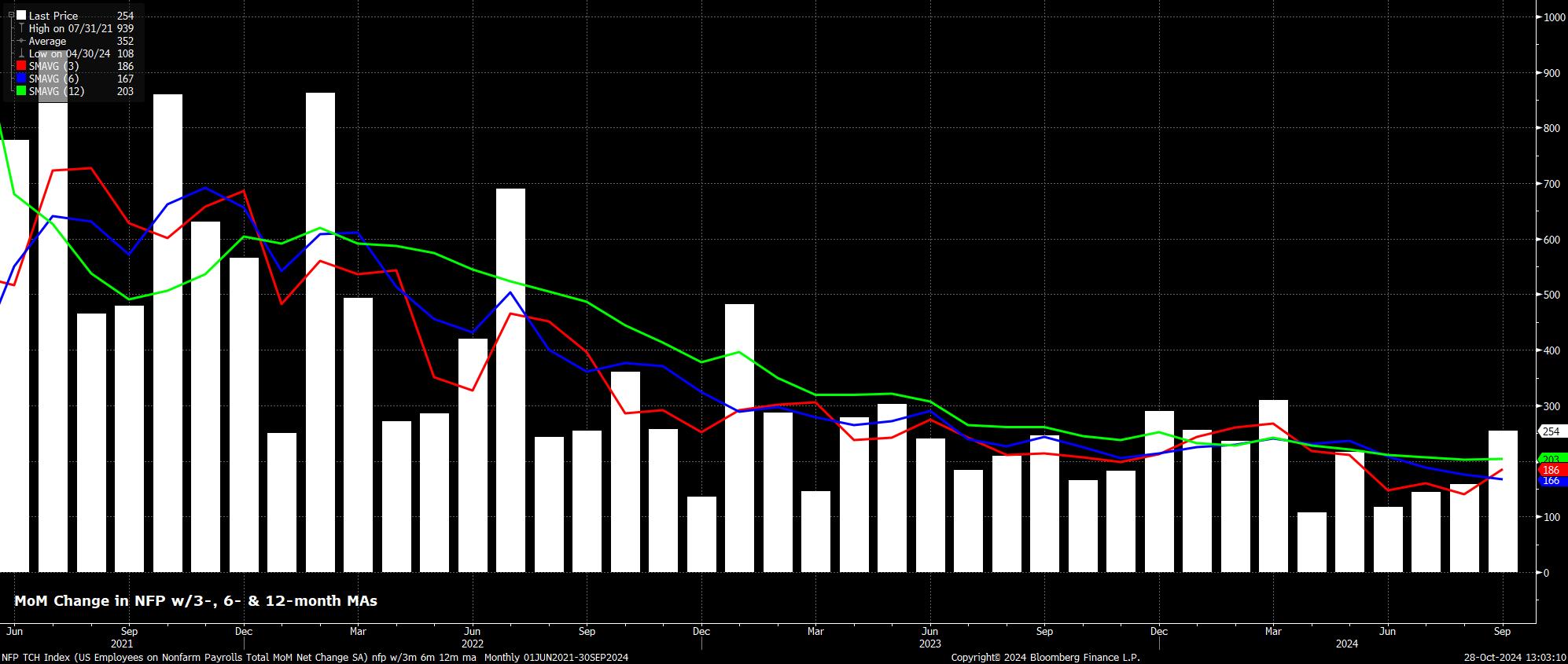

Headline nonfarm payrolls are set to have risen by +110k in October, a considerable slowdown from the +254k pace seen in September, while also being substantially below the breakeven pace of payrolls growth – around +225k – required for employment growth to keep up with the increasing size of the labour force. As always, the range of estimates for the payrolls print is incredibly wide, from -10k to +165k. A negative print, which would be incredibly surprising, would be the first MoM decline in employment since 2020, were it to occur.

As noted, there are numerous downside risks to headline employment growth in the October labour market report.

‘Mother Nature’ presents the first, with Hurricanes Helene and Milton both likely to depress employment, particularly in southern parts of the United States. While Helene arrived in late-September, the significant impact it had in North Carolina likely means that many were likely still off payrolls by the time that the survey week came around. Hurricane Milton, meanwhile, made landfall in Florida during the survey week, likely depressing employment in the state, with jobless claims having risen by a third from the YTD average during the week in question.

Secondly, there is the impact of ongoing strikes. While there are several to consider, those ongoing at Boeing are by far the most significant, with estimates pointing to over 30,000 Boeing workers taking industrial action. While the specific impact of this action on payrolls growth will hinge on how Boeing is handling salary payments, there is nevertheless likely to be a detrimental impact from this, and from the knock-on impact of the strikes on other companies in the Boeing supply chain.

Combined, these two factors could act as a drag of between 80-100k on headline nonfarm payrolls growth, with Fed Governor Waller having flagged the latter figure as his ballpark estimate earlier in the month. This means that, mentally, the FOMC are likely to add around 100k on top of whatever the NFP print is, before deciding its policy implications.

In terms of leading indicators for the jobs report, risks also tilt to the downside. Due to the timing of the report, the ISM PMI surveys are not due until after the employment report is released. Furthermore, as always, the ADP employment print should be ignored, while the NFIB hiring intentions metric – which has been an accurate gauge of employment growth this cycle – points to an NFP print of close to +270k, which seems far-fetched, at best.

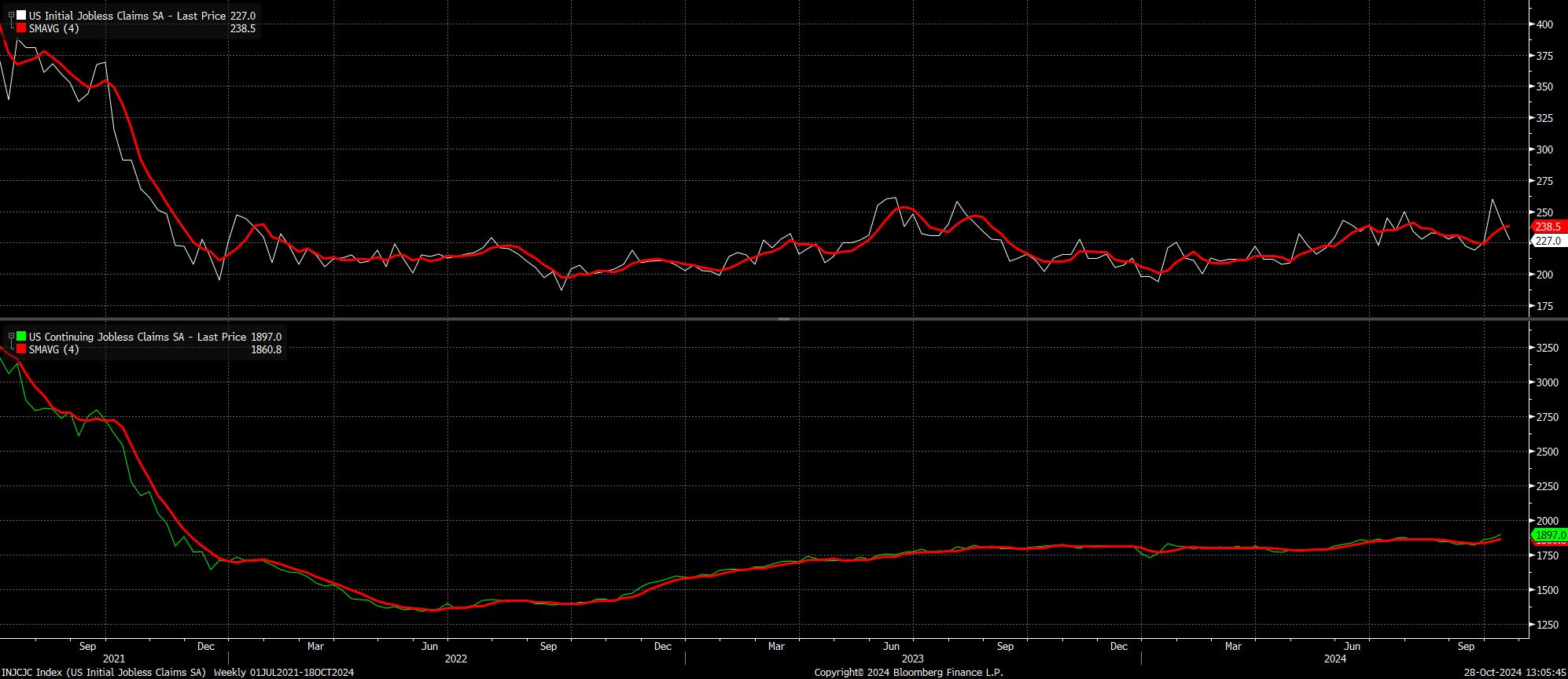

Jobless claims, though, could be of some use. Initial claims rose by 20k between the two survey weeks, while continuing claims rose by a more sizeable 70k over the same period, again suggesting a significant degree of downside risk to the headline payrolls print.

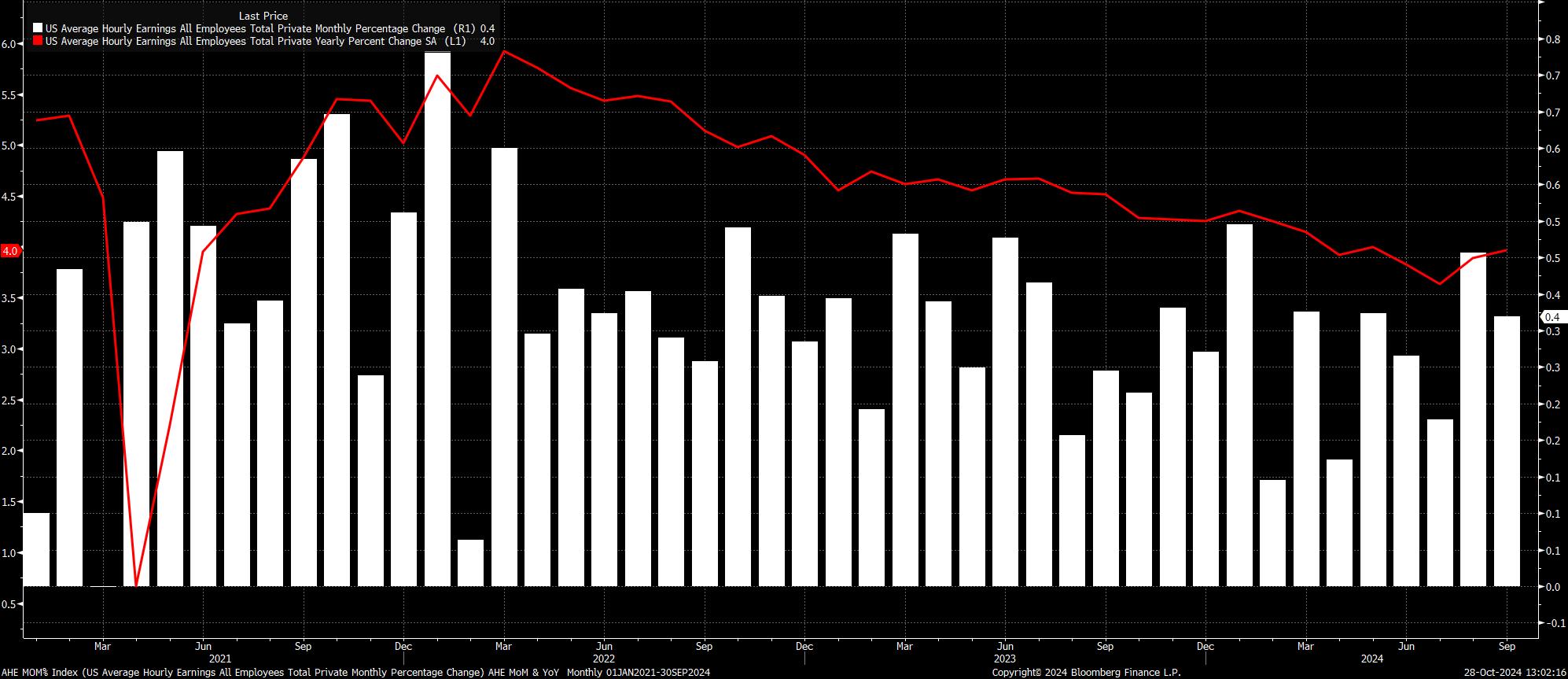

Meanwhile, average hourly earnings are set to have risen by 0.3% MoM in October, a tick slower than the 0.4% pace seen in September. There is, however, the risk of a faster-than-expected pace of earnings growth, particularly if hurricane-related layoffs have disproportionately impacted lower-paid workers in southern states. On an annual basis, though, earnings growth is set to hold steady at 4.0% YoY.

In any case, it seems unlikely that the earnings figures will materially alter the policy outlook, with FOMC members having already obtained sufficient confidence in inflation returning towards the 2% target over the medium-term, and with incoming data continuing to point to a relatively rapid pace of disinflation.

Turning to the household survey, measures of labour market slack are likely to remain largely unchanged in October.

Unemployment, consequently, is seen unchanged at 4.1%, though there is some risk of a small tick higher to 4.2%, depending on the impact of the aforementioned downside risks. Participation, meanwhile, is expected to have continued to hold remarkably steady, just shy of cycle highs, at 62.7%. The adverse weather, however, could well detrimentally impact response rates to the household survey, increasing volatility associated with the data.

For financial markets, the October jobs report comes in the middle of a risk event bonanza, which includes earnings from 5 of the ‘magnificent seven’ stocks; the UK Budget; a BoJ policy decision; the presidential election; and, decisions from the FOMC and BoE. This plethora of event risk is likely to limit conviction behind market moves for the time being, particularly with the jobs report coming just two trading days before the election.

Nevertheless, in keeping with recent reactions to US economic data, the jobs report seems likely to be another case of ‘good news is good news’, and vice versa, for risk sentiment, as participants focus on the macroeconomic picture that the figures paint, as opposed to any potential dovish policy implications of the report.

In terms of those policy implications, they are likely to prove relatively limited. Given the incredibly skewed nature of the figures, it seems unlikely that those on the FOMC will read too much into the data, and draw any significant conclusions from the report. Recall, policymakers tend to focus on trends in the data, and not a single data point; those trends, even after the October jobs report, are likely to point to a continued normalisation in labour market conditions, as opposed to any significant or sudden weakness.

Consequently, my base case remains that the bar for another 50bp Fed cut is a relatively high one, and that the FOMC will instead proceed with 25bp reductions at every meeting from here, until next summer, when rates are likely to reach a neutral level around 3%.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.