- English

- عربي

Markets Are Looking At The Wrong Second-Round Effects Of The Energy Shock

Summary

- On Hold For Now: Seven G10 central banks meet this week, with all besides the RBA set to stand pat, adopting a 'wait and see' approach

- Energy Shock: That said, the ongoing energy price shock amid conflict in the Middle East will exert upwards pressure on headline inflation metrics in the months ahead

- Second-Round Effects: Still, with labour markets relatively slack, and growth already anaemic, the potential for second-round effects seems limited, meaning central banks should 'look through' any near-term inflation increase, and that markets have likely repriced too far in a hawkish direction

A jam-packed week of central bank decisions awaits, with seven policy announcements across G10 alone, giving policymakers their first official chance to opine on the economic impact of ongoing conflict in the Middle East, and market participants an opportunity to gauge policymakers’ reaction functions.

Energy Shock In Focus

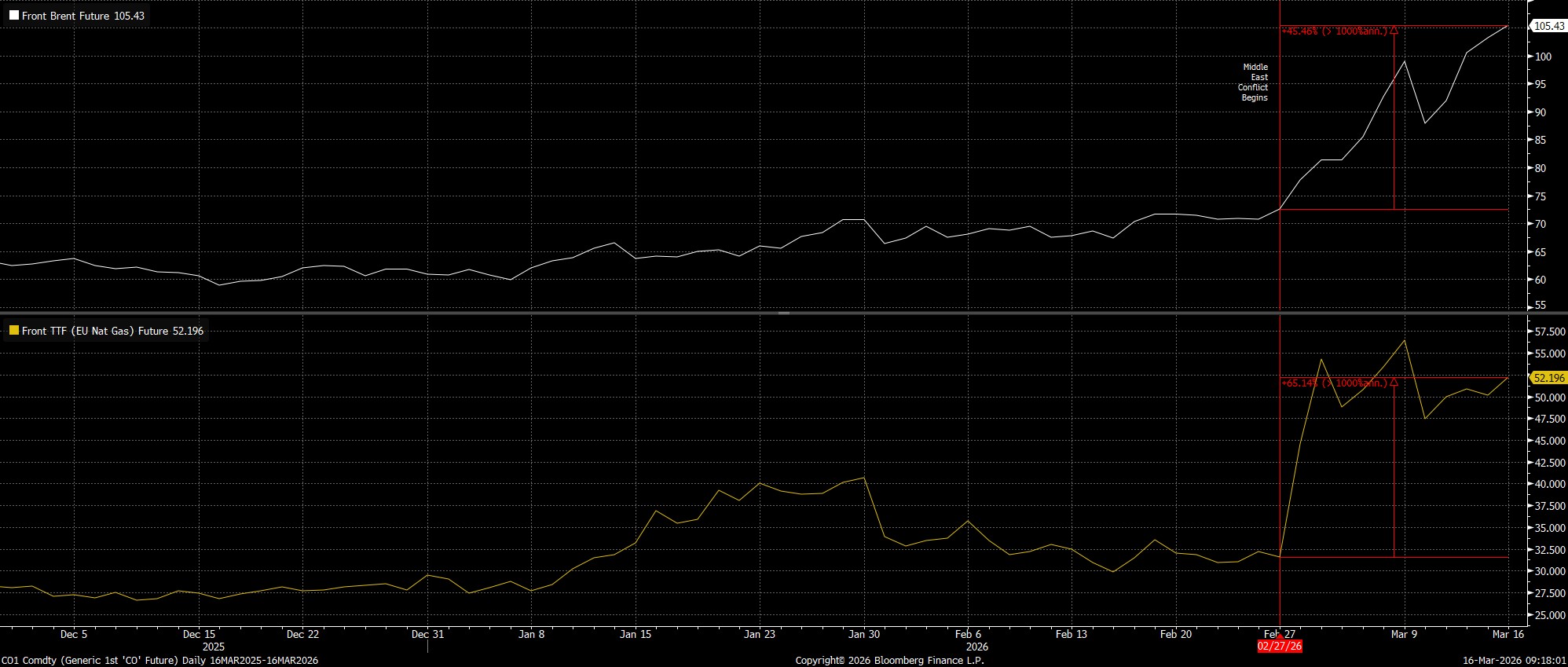

Clearly, the chief concern of both cohorts is the ongoing energy price shock. Prices of key commodities, namely crude oil and natural gas, have surged since conflict broke out, and the Strait of Hormuz became essentially impassable. Importantly, it is not only prompt prices, or front futures, that have vaulted higher, but commodity prices across the curve, implying an expectations that it will take some considerable time for the impact of present transit issues to fully fade.

Markets, hence, have reached for a relatively simple equation. Higher energy prices will lead to higher headline inflation, which in turn will lead to tighter policy stances from central banks across the globe. That theory, though, massively over-simplifies the dynamic that is actually playing out.

That said, it makes some degree of sense that market participants have lurched to that conclusion. Given that both the magnitude, and duration, of the energy price shock, and its subsequent impact on inflation metrics is at this point unknown, as well as with the distribution of potential outcomes from the ongoing conflict so wide, participants are having great difficulty in pricing a concrete outlook, either for monetary policy, or for the global economy at large.

Second-Round Effects Hold The Key

Here, it is important to remember what central banks are actually targeting. While specific mandates vary from authority to authority, generally speaking central banks are seeking ‘price stability, typically defined as inflation around the 2% mark, as judged over the medium-term. This final part is key, given that monetary policy famously works with ‘long and variable lags’, somewhere in the region of 18 to 24 months.

What one must consider, then, is not how high energy prices may push headline inflation metrics, but whether there is a risk of those price pressures becoming embedded, and thus inflation remaining persistently above target.

Here, we must turn to the concept of ‘second-round effects’, whereby an initial price shock – of the ilk that we currently see from the energy complex – becomes a more persistent one as a result of other catalysts.

The most obvious of these catalysts is a ‘wage-price spiral’, where higher prices lead employers to seek higher wages in order to compensate for an increased cost of living, which is hence passed on by companies in the form of higher prices, leading to a rather vicious cycle.

Though this did play a role in 2022/23, in the aftermath of the energy price shock at the beginning of the Russia-Ukraine war, infamously leading BoE Governor Bailey to urge workers not to ask for pay rises, it seems unlikely that such a factor is in play now. Across DM, labour markets continue to exhibit a significant degree of slack, limiting the bargaining power that workers have to request the pay increases that could lead to a rerun of such a scenario.

The second such catalyst stems from inflation expectations. Policymakers typically seek to ensure that inflation expectations remain ‘well-anchored’ at levels close to their inflation target, in order to ensure that decision-making from economic actors – be that price setting by a business, purchases by consumers, or wage bargaining by employees – is conducted in a manner consistent with the inflation target.

At this stage, across DM, expectations are broadly at target-consistent levels, once more reducing the risk of price pressures becoming embedded within the economy.

Markets Are Ignoring Growth Risks

With that in mind, and providing that the commodity price shock does prove relatively short-lived, as seems plausible, the base case logically becomes that higher energy prices will lead to a temporary ‘hump’ in inflation, as opposed to being the beginning of another sustained lurch higher.

While the obvious parallel that participants seem to have drawn is with that of 2022, the global economy now is in a very different place to where it was four years ago – broadly speaking, economic momentum is relatively weak; labour markets are relatively slack, with earnings pressures having moderated significantly; and, perhaps most importantly, monetary policy is already restrictive across much of DM, and not uber-loose as it was when the world was emerging from the pandemic. Consumer balance sheets are also in a considerably poorer place now, than then, with savings balances having been drawn down considerably.

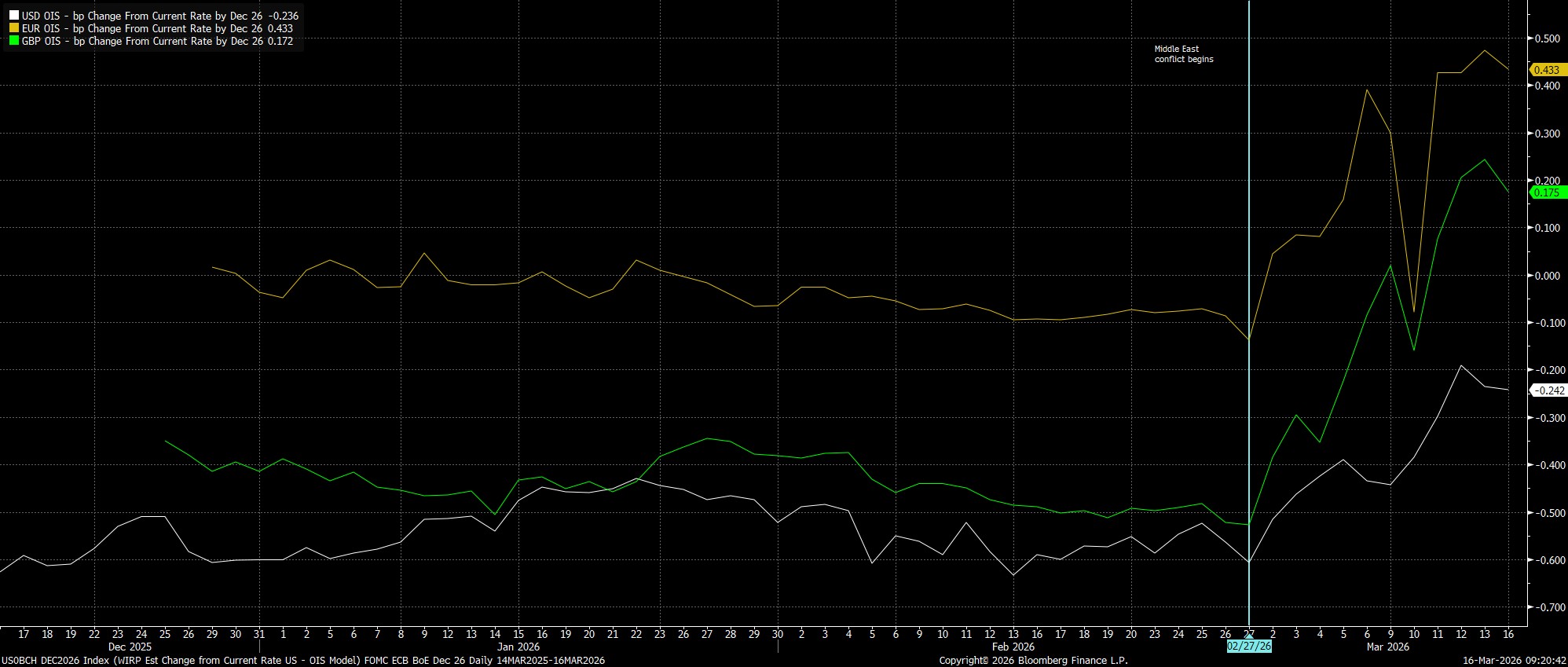

Viewed through this lens, current central bank pricing seems wide of the mark. Swaps currently discount less than 25bp of easing from the Fed by year-end, while STIR pricing on this side of the pond is even more extreme, with SONIA pricing 20bp of BoE tightening by December, and the EUR swaps curve almost fully discounting two 25bp ECB hikes by the end of 2025, with the first seen in July.

Markets, here, seem to have misread the situation. Short of the second-round effects of higher energy prices being a sustained inflationary shock, it seems considerably more likely that the consequence of the energy shock will be a substantial hit to demand, with such a hit becoming more considerable, the longer the energy shock wears on. Put very simply, the more that a consumer or business is spending on energy, the less they are able to spend elsewhere, be that on discretionary purchases, or capital expenditure/investment.

Tightening into such an environment, then, would represent a grave policy mistake, that G10 central banks would be wise not to commit. While the hawks have been very vocal thus far, and data is likely to support their argument in the short-term at least, policymakers and market participants alike would be wise to ‘zoom out’, and not lose sight of the bigger picture. ‘Team Transitory’ seems to have the upper hand, and fading of the recent hawkish repricing in STIRs seems ripe to be faded.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.