- English

- عربي

Summary

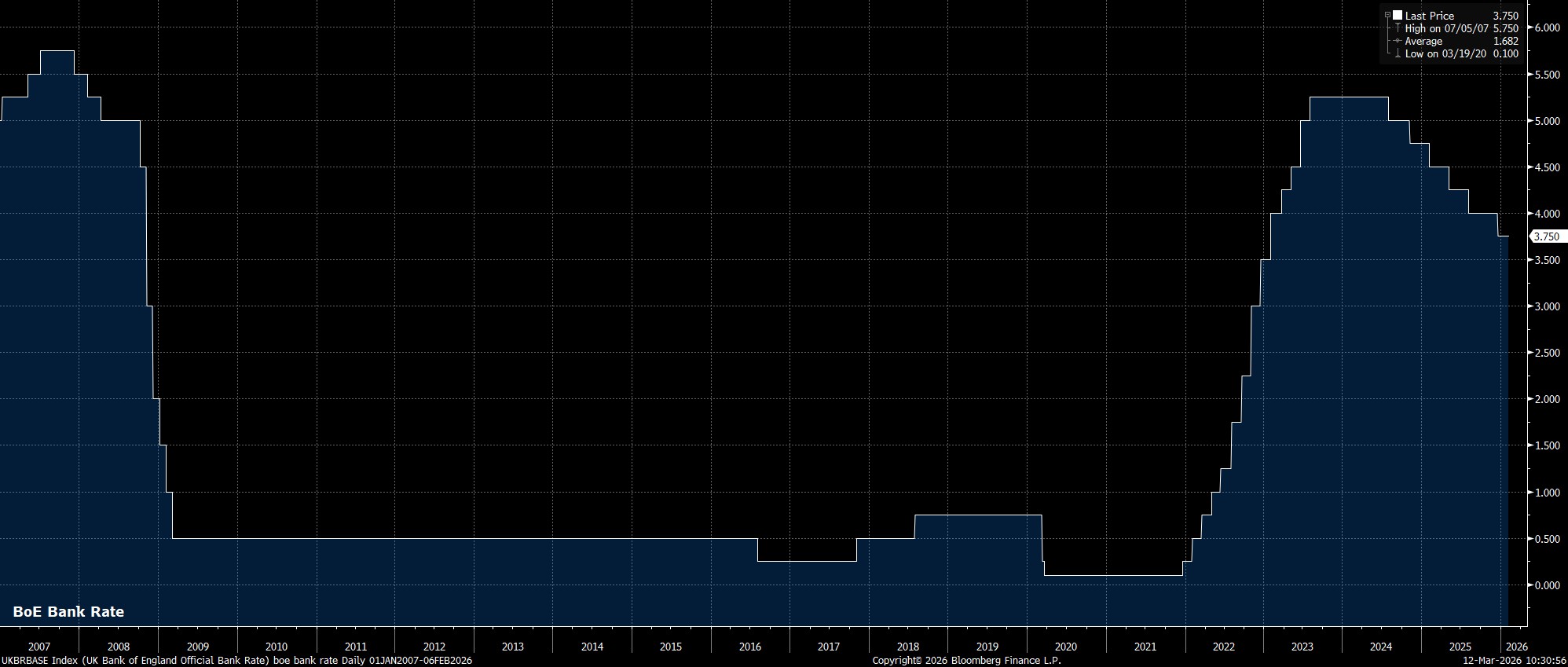

- Standing Pat: Bank Rate is set to remain at 3.75%, with the MPC adopting a 'wait and see' approach amid geopolitical turmoil

- Inflation Risks: Upside inflation risks have emerged as a result of the recent commodity price surge, though the MPC should 'look-through' this temporary inflation boost over the medium-term

- Cuts Delayed: As a result, and with the potential for second-round effects limited, further Bank Rate cuts are likely still on the cards as the year progresses

Bank Rate Unchanged

As noted, the MPC are likely to stand pat at the March confab, maintaining Bank Rate at 3.75%, having last delivered a 25bp cut at the December 2025 meeting.

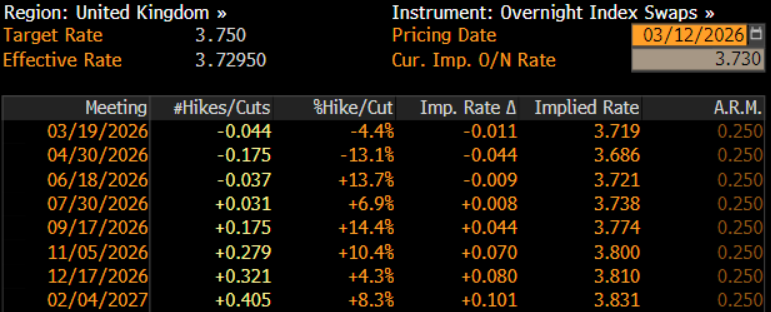

Money markets, per the GBP OIS curve, price next-to-no chance of any action this time around, having undergone a dramatic hawkish repricing since the breakout of conflict in the Middle East. Having discounted as much as 52bp of easing this year as of late-February, the curve now discounts around 10bp of tightening by December, reflecting the recent surge seen in crude, natural gas, and other energy prices.

Vote Split In Focus

The MPC have not voted unanimously for a Bank Rate decision since September 2021, with a unanimous vote again unlikely this time around.

At the February meeting, Governor Bailey was again the swing vote, in a 5-4 decision to stand pat. This time out, it seems highly unlikely that any of those five hawks (Bailey, Greene, Lombardelli, Mann and Pill) will change their mind, not least considering the intensification of upside inflation risks since the last MPC discussion around six weeks ago. Given those upside inflation risks, it seems plausible that one or two of the MPC’s doves may also vote to stand pat, with Deputy Governors Breeden and Ramsden the most likely candidates to prefer a ‘wait and see’ approach at this time. Hence, a 7-2 or 6-3 vote seems the most likely outcome.

Policy Guidance Likely Tweaked

Meanwhile, the accompanying policy statement is likely to be tweaked to reflect how significantly the macroeconomic outlook has changed since the February meeting, owing to the upside inflation risks posed, in the short-term, by higher energy prices.

The MPC are likely to acknowledge how the outlook has grown considerably more uncertain since the prior meeting, though are unlikely to come to any firm conclusions as to the precise impact that ongoing geopolitical events may have on the UK economy, instead waiting until the April Monetary Policy Report, when the full impact of recent developments will be modelled.

That said, the statement is likely to reiterate the idea of data-dependency, noting once more that the ‘extent and timing of further easing in monetary policy will depend on the evolution of the outlook for inflation’. It is reasonable to expect, though, that the Bank’s explicit guidance around further Bank Rate cuts being ‘likely’ will be removed, as such a dovish remark seems somewhat misplaced in the present environment.

Geopolitics Has Upended The Outlook

At the February confab, the accompanying Monetary Policy report provided some much-needed good news on the inflation front, with the forecasts pencilling in not only a return to the 2% target this spring, but also headline CPI remaining at that level through the remainder of the forecast horizon.

However, the entire outlook has since been upended by developments in the Middle East, with the effective impassability of the Strait of Hormuz causing significant disruptions to global commodity flows, subsequently causing prices to spike, with Brent crude having recently cleared the $100bbl mark. Crucially, the implications of this energy price shock on the wider economy depend almost entirely on the duration of the conflict, with there being little-to-no clarity on that front right now.

That said, while the MPC will hope to have greater clarity on this front by the time of the April forecast round, at face value one can reasonably assume that higher energy prices will result in a substantial lift to headline inflation metrics, though there may be some degree of cushioning provided by the Ofgem energy price cap, depending on when the present situation resolves. It can also be reasonably assumed that higher headline inflation will act as a drag on demand more broadly, posing headwinds to growth, which was already anaemic at best.

That said, the potential for ‘second-round’ inflationary effects seems limited, given there being both a significant degree of labour market slack still present within the economy, and with consumer balance sheets not in the rudest of health. This, in turn, should allow policymakers to ‘look-through’ any temporary CPI boost stemming from higher energy prices, with underlying pressures set to remain relatively muted.

Conclusion

Consequently, it is likely to prove a case of Bank Rate cuts being ‘delayed’ for the time being, as opposed to cuts being ‘cancelled’ entirely.

Bank Rate remains in restrictive territory, with neutral likely sitting around the 3% mark, meaning that it is very difficult to imagine a world in which the Bank deliver the rate hikes that markets have started to price, not least considering that some degree of normalisation in commodity flows is likely by the time of the April meeting, meaning that one would expect the peak in headline CPI in that forecast round to be lower than where knee-jerk expectations probably put it right now (approx. 3% in H2 26).

Hence, for the time being, the cut that had been expected in March is likely to be punted to April, with the MPC likely to then deliver further easing through the remainder of the year, likely at MPR meetings, lowering Bank Rate to a neutral level by year-end. This is simply an elongation of the path previously expected, with the pace and extent of easing likely to be little changed, providing that second-round inflationary effects prove limited. Clearly, though, conviction around this path is considerably lower than it ordinarily would be, given the fluid and ever-changing global backdrop.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.