- English

- عربي

Summary

- Chief Concerns: Market participants are again fretting over tariff uncertainty, as AI capex concerns linger, and geopolitical uncertainty persists

- Other Worries: Other worries are present too, including the erosion of Fed policy independence, ongoing policy volatility in DC, and a continuation of the 'sell America' trade

- Fundamentals Still Strong: All that said, the fundamental backdrop remains a robust one, with earnings growth solid, economic growth robust, as well as with both monetary and fiscal tailwinds both still present

Bad news sells.

That’s nothing new. It has always been the case that an innate negativity bias within all of us triggers a greater emotional response to negative news, or stories about potential threats, than one experiences to positive headlines.

Even by those standards, though, there seems to be an awful lot of negative news around right now, on a whole host of different fronts. However, markets have always had an uncanny ability to climb that ‘wall of worry’, and that ability is highly unlikely to have gone away.

Let’s, then, have a look at the worries on participants’ minds right now, and see how they are likely to be navigated.

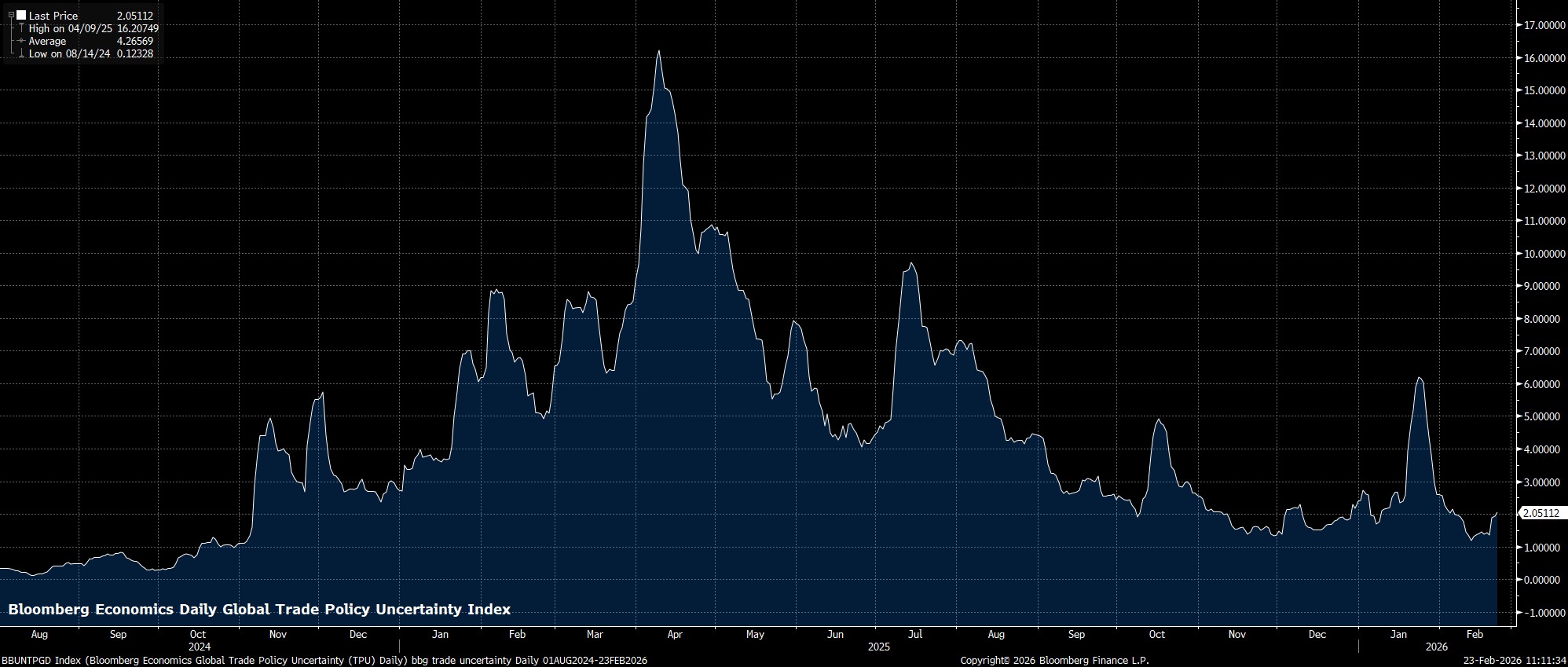

Trade

Trade-related uncertainty is back on the radar, after the Supreme Court struck down President Trump’s ability to impose tariffs under IEEPA in a long-awaited decision last Friday. However, this uncertainty really shouldn’t persist for long – the Admin’s initial backup plan, of imposing a 15% global tariff under Sec. 122, means that for the next 150 days at least there will be no, or very little, change to the overall average effective tariff rate.

In the meantime, investigations under Sec. 301 will take place, with those investigations in turn likely leading to a tariff structure very similar to that which existed before the SCOTUS ruling being recreated using different statutes of commerce law. Put simply, while the legal ‘means’ through which tariffs are implemented may change, the macroeconomic ‘ends’ will remain largely the same. Hence, the overall impact on growth, unemployment, inflation, or any other economic variable, as well as on the monetary and fiscal outlooks, should prove minimal at most.

The biggest risk, here, is actually not one emanating form Washington DC, but of some form of international retaliation – say, the EU reaching for the anti-coercion instrument. While doing so would be counter-intuitive, and is not my base case, some probability of at least punchier rhetoric from around the world should be considered.

AI

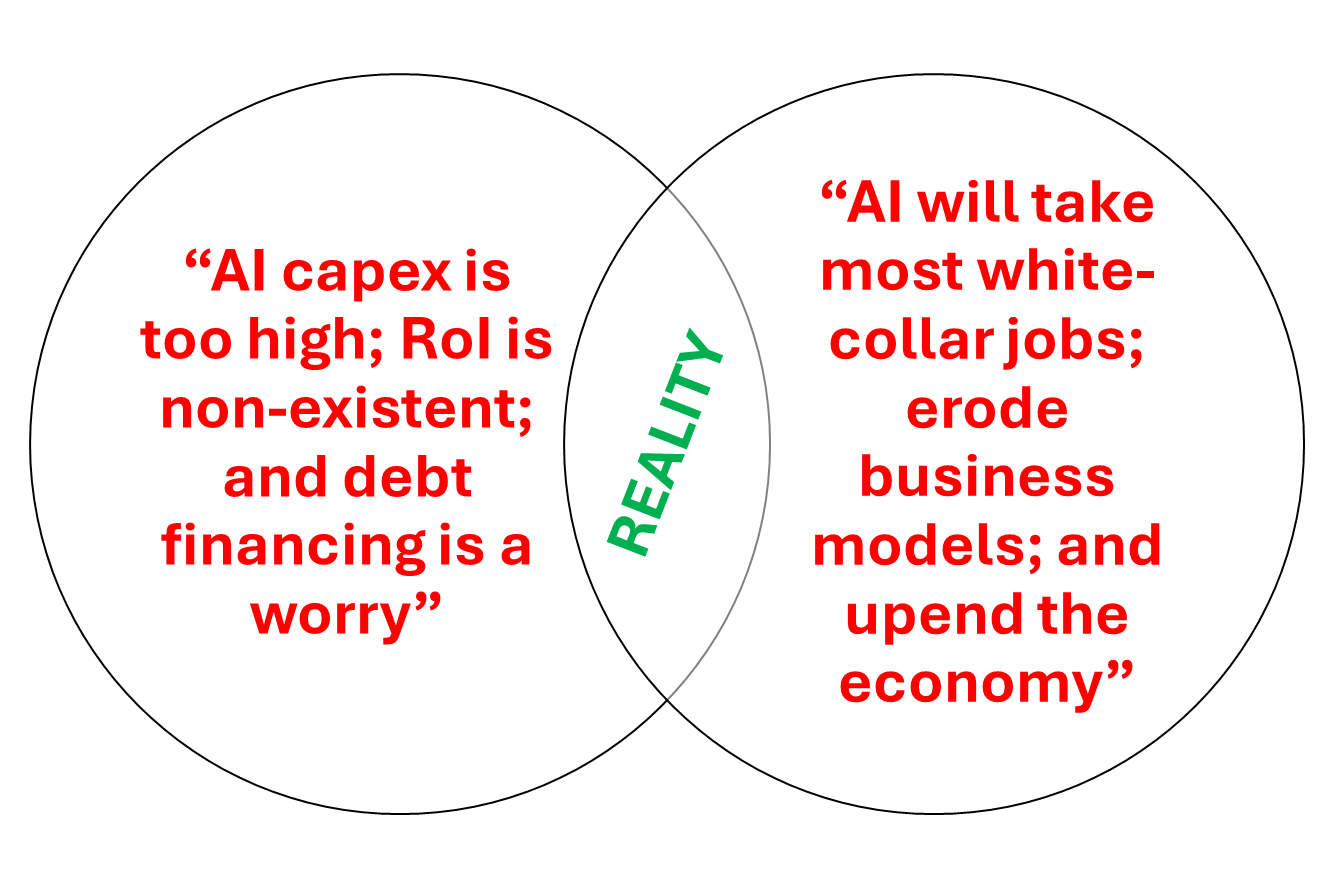

Participants at large continue to take an increasingly sceptical view of the AI theme; gone are the days of ‘all capex is good capex’, having been replaced with question marks over both how said spending is being financed, as well as the payback timescales. Simultaneously, concern is increasing as to whether progress in the AI space will lead to the death of many familiar business models, particularly in the realm of software.

At risk of stating the obvious, both of those cannot be true – AI spending failing to be monetised can’t be the biggest market risk, at the same time as AI advancements killing ‘white collar’ work is also the top concern. While markets oscillate, sometimes wildly, between those two ends of the spectrum, reality is probably somewhere in the middle.

Saying with certainty how a new technology like this evolves is a fool’s errand, akin to how folk once thought that things like the telephone and the internet would never catch on, especially when progress is being made as rapidly as it is at present. However, while some hyperscalers likely are spending at an unsustainable rate with high revenue concentrations and questionable payback times (e.g. ORCL), and while some sectors will likely see their competitive advantages eroded over time (e.g. those heavily reliant on patterns and repetitive tasks), markets will likely still present opportunity, not only in terms of those selling the ‘picks and shovels’ of the AI boom, but also those companies/sectors that are able to use new technologies in order to enhance their operation, and thus profitability.

Geopolitics

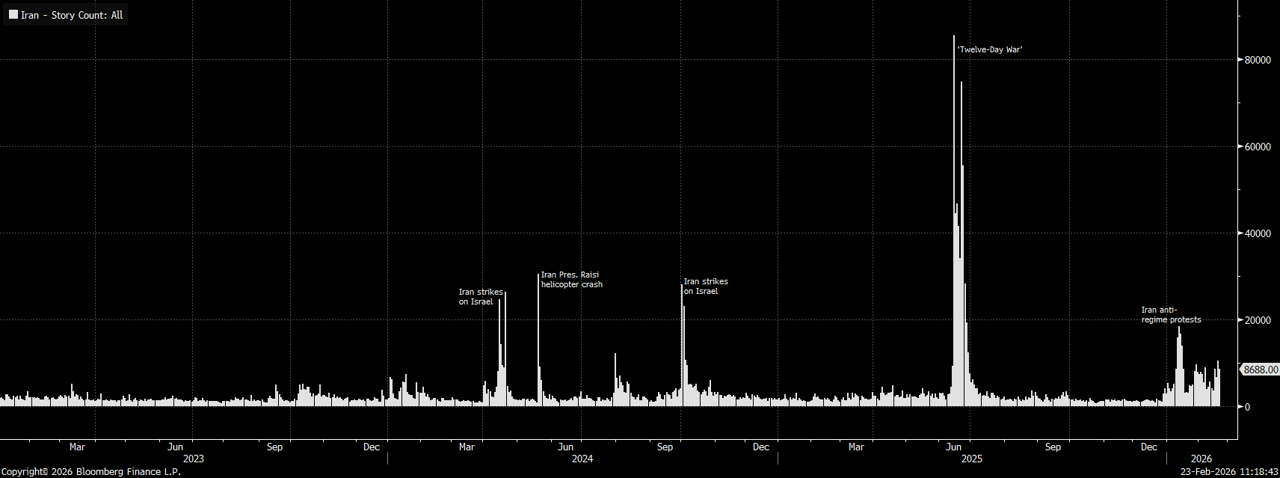

Geopolitical risk ebbs and flows over time, with markets typically being utterly terrible at accurately discounting it. Of course, tensions are presently heightened in the Middle East, as the US continue to amass military materiel in the region, potentially for use in a strike against Iran, as negotiations between the two parties continue.

While a strike of any nature, especially one that morphs into a more prolonged-conflict, poses some degree of risk to crude supply in particular, broader context is important here, especially with the global oil market still in an over-supplied state, meaning that any crude interruptions can probably be made up with supply from elsewhere relatively easily.

Furthermore, from an equity perspective, the ‘half-life’ of geopolitical headlines is typically relatively short-lived. If one examines the most significant Middle East geopolitical shocks in the last 30 years, while the initial move has been one of risk aversion, the S&P has typically recovered losses within a week or two, with such developments tending to prove more of a short-term headwind, as opposed to a catalyst for more longer-lasting declines. I see little reason to believe that this time would be different, not least considering the resilient nature of both economic and earnings growth, meaning that I continue to view dips as buying opportunities.

Other Worries

While the aforementioned three factors may be those that participants appear most pre-occupied with for the time being, there are others that bear consideration.

Inflation is one, with some still concerned that price pressures may prove persistent, even if the disinflationary process does appear relatively well-embedded across DM by this stage, particularly with further bouts of tariff-induced inflation stateside now a somewhat more distant prospect. Similarly, jitters over a potential disorderly sell-off in Treasuries haven’t gone away either, not only as the fiscal path remains unsustainable, but also as global confidence in USTs, and the USD, continues to wane. Still, my base case here is that the whole ‘sell America’ narrative is rather overdone and that, if international investors are to trim stateside exposures this will be done gradually, and not in some sort of ‘fire sale’.

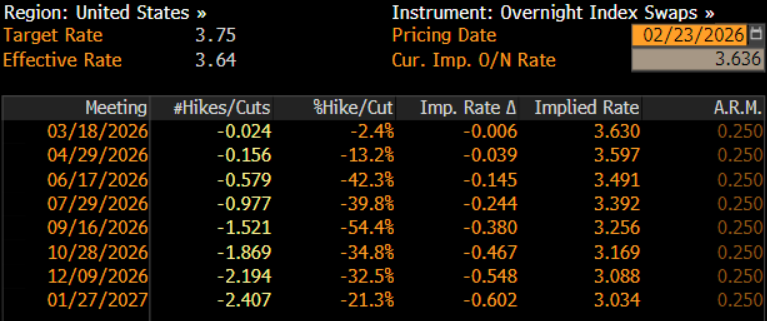

Besides that, while policy volatility is likely to remain elevated, especially in Washington DC, it cannot be said that uncertainty will do the same, especially given how well-known Trump’s ‘escalate to de-escalate’ strategy should now be. Simply, the noise is something that we’ll all have to learn to live with. Finally, concerns over incoming Fed Chair Warsh adopting a drastically more dovish approach are probably overdone, given that the Chair is simply ‘first among equals’, and that unless economic data supports whatever action Warsh may propose, a majority of FOMC members are unlikely to back it.

Climbing Higher

Taking all that into account, I’ll suggest doing what I’ve suggested so many times already this year – zoom out!

Yes, there are plenty of near-term concerns playing on participants’ minds. However, the fundamental backdrop for risk assets remains robust – we’ve just come through a fifth consecutive quarter of double-digit earnings growth on Wall St, while US economic output continues to grow at a healthy clip (if we ignore the record-long government shutdown having skewed Q4 GDP to the downside). Added to which, monetary tailwinds will continue as the year progresses with the lagged impact of last year’s 75bp of Fed cuts, coupled with RMPs expanding the balance sheet once more, and further cuts likely being delivered as the year progresses. On top of this, fiscal tailwinds are also on the horizon, as the impulse turns positive on the back of the ’One Big Beautiful Bill Act’ passed last year.

With all this in mind, I retain confidence that markets will be able to continue to climb this ‘wall of worry’. Though a continued sector rotation could cap index-level gains to a degree, the broader, medium-run ‘path of least resistance’ continues to lead to the upside.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.