- English

- عربي

Equities Price An End To Middle East Conflict, But Sector Dispersion Persists

Stocks Think It’s All Over

Recent equity price action suggests that many market participants are becoming less focused on the day-to-day geopolitical news flow, with a prevailing view emerging that light is emerging at the end of the tunnel, and that a durable end to hostilities is now seen as a foregone conclusion

Certainly, recent market moves suggest such a view is increasingly widely-held, with the S&P having now erased all of the losses seen since kinetic action started at the end of February, and turned positive YTD once more.

This viewpoint stems from a number of factors – talks between the US and Iran continue in an attempt to reach a peace deal; President Trump’s Hormuz blockade appears to be working as part of an ‘escalate to de-escalate’ negotiating gambit’; and, neither side appears to seek major re-escalation in terms of kinetic action, with the fortnight-long ceasefire continuing to hold.

For stocks, which are inherently forward looking, all this is enough ‘light at the end of the tunnel’ to allow markets to somewhat shrug off day-to-day headlines regarding the ongoing conflict, and instead focus on the broader direction of travel. While the journey to get there is indeed likely to be a bumpy one, the most important point for participants will be ensuring that we remain on that journey. So long as we do, equity dips are likely to prove shallow, and likely to be used as buying opportunities as well.

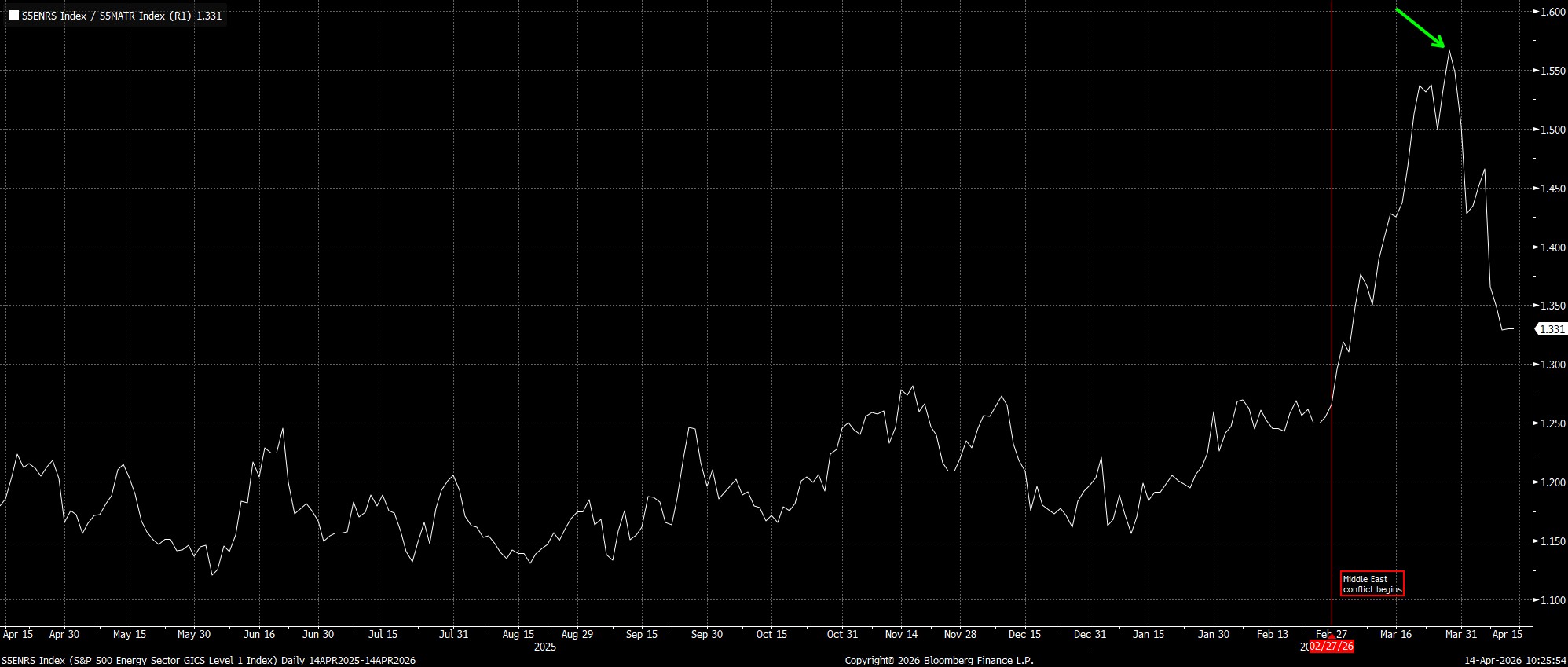

While it was only on Monday that the S&P erased its conflict-linked decline, one could argue that the equity market actually began to move past a point of ‘peak fear’ at the tail end of last month. Comparing the performance of the sector most likely to benefit from higher commodity prices caused by the conflict, Energy, with that of the sector most likely to be harmed by it, Materials, signals a dramatic reversal in sentiment since President Trump’s ‘Truth’ post noting ‘great progress’ having been made in talks with the Iranians, which in turn represented the first sliver of de-escalatory news that had been received since the war commenced.

Not All Sectors Are Equal

Digging a little further into things, at a sectoral level, one can see that the recent rebound in the S&P hasn’t treated all stocks equally. In fact, only five of the eleven GICS sectors (Consumer Discretionary, Energy, Financials, Information Technology & Communication Services) trade above their pre-conflict closing level.

In many regards, there is little reason for the other sectors to be lagging so significantly. While Industrials and Materials will indeed have to grapple with higher input costs in the coming quarters, as a result of higher energy prices, though these pressures should prove manageable, particularly in the event that Hormuz flows normalise in relatively good order, as markets now appear to be discounting.

Meanwhile the relative outperformance of the Consumer Discretionary sector suggests little by way of market concern in terms of consumer spending moving forward, with the rebound in equities at large supporting this theory too, as the ‘wealth effect’ should continue to prop up the upper part of the ‘K-shaped economy’, while tax refunds from the OBBBA largely compensate for any increase in consumer energy costs.

This, in turn, gives one little reason to expect that higher energy prices would prove the trigger for a broader, and more prolonged, economic slump, at the present juncture, which further suggests that there should be no structural reason to expect those underperforming sectors to lag behind the pack for too much longer.

Conclusion

Perhaps, it will require the agreement of a definitive and durable deal to end the conflict before participants are fully able to buy into that theme, though the closer we get to such an agreement, the more participants are likely to increasingly buy into a broader risk rally.

Underpinning this thesis is the continued idea that participants are actively seeking not to get ‘caught short’, with a sustained bearish view something that remains difficult to position for, considering the elevated probability that, as we’ve seen so many times of late, the entire macro outlook can be rapidly turned in a more positive direction, simply on the back of a ‘Truth Social’ post, which subsequently sparks a face-ripping rally few want to be on the wrong side of.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.