- English

- عربي

Crude Oil Volatility Highest Since 2022 as Middle East Tensions Drive Oil Market Uncertainty

Key Takeaways

• Energy markets remain the central driver of cross-asset volatility as traders focus on developments in the Middle East.

• Brent crude has surged toward $86 and is on track for its strongest weekly gain since 2022.

• One-month Brent implied volatility has jumped to 67%, the highest since the Russia-Ukraine conflict.

• The oil futures curve is showing extreme backwardation, signaling significant near-term supply concerns.

• Analysts estimate Brent could reach $120 if supply through the Strait of Hormuz is disrupted for several weeks.

• Conversely, signs of de-escalation could push prices back toward a longer-term equilibrium near $60.

Energy Markets at the Center of Global Market Attention

The eyes of many in financial markets remain firmly fixed on developments in the Middle East. Even traders not directly involved in energy markets are closely watching crude oil because of its influence across asset classes.

Brent crude, WTI crude, Nat Gas and Gasoline are now shaping broader market sentiment. Hedging flows, speculative activity, and changing liquidity conditions are contributing to exaggerated price swings and increasingly fast-moving markets.

At the core of this environment is the challenge of pricing risk and certainty. With geopolitical developments evolving rapidly and most market participants lacking deep expertise in geopolitical strategy, conviction around where prices should trade is currently very low.

Pricing the Risk of Oil Supply Disruptions

Strategists are attempting to estimate a theoretical fair value for Brent crude based on two key factors.

The first is the scale of potential output disruptions. The second is the duration that energy infrastructure and production facilities may remain offline.

These variables have enormous implications for supply expectations. As a result, the distribution of potential outcomes for crude prices has become extremely wide, naturally leading to higher volatility across the market.

Brent Crude Price Action and Levels to Monitor

Brent crude recently traded above $86 before sellers pushed the price back below $84. However, buying activity returned during the Asian session, with prices again pushing toward the $85 level.

Meanwhile, spot WTI crude continues to encounter strong selling pressure around the $80 mark. That level increasingly looks like a key technical threshold where a daily close above it could open the door to further upside.

The rally in oil prices has been substantial. Crude is currently on track for its strongest weekly gain since 2022.

Gasoline has also showing significant momentum. While our cash gasoline market is down around 1.5% today as sellers step in, gasoline has rallied for ten consecutive sessions and remains more than 50% higher year to date.

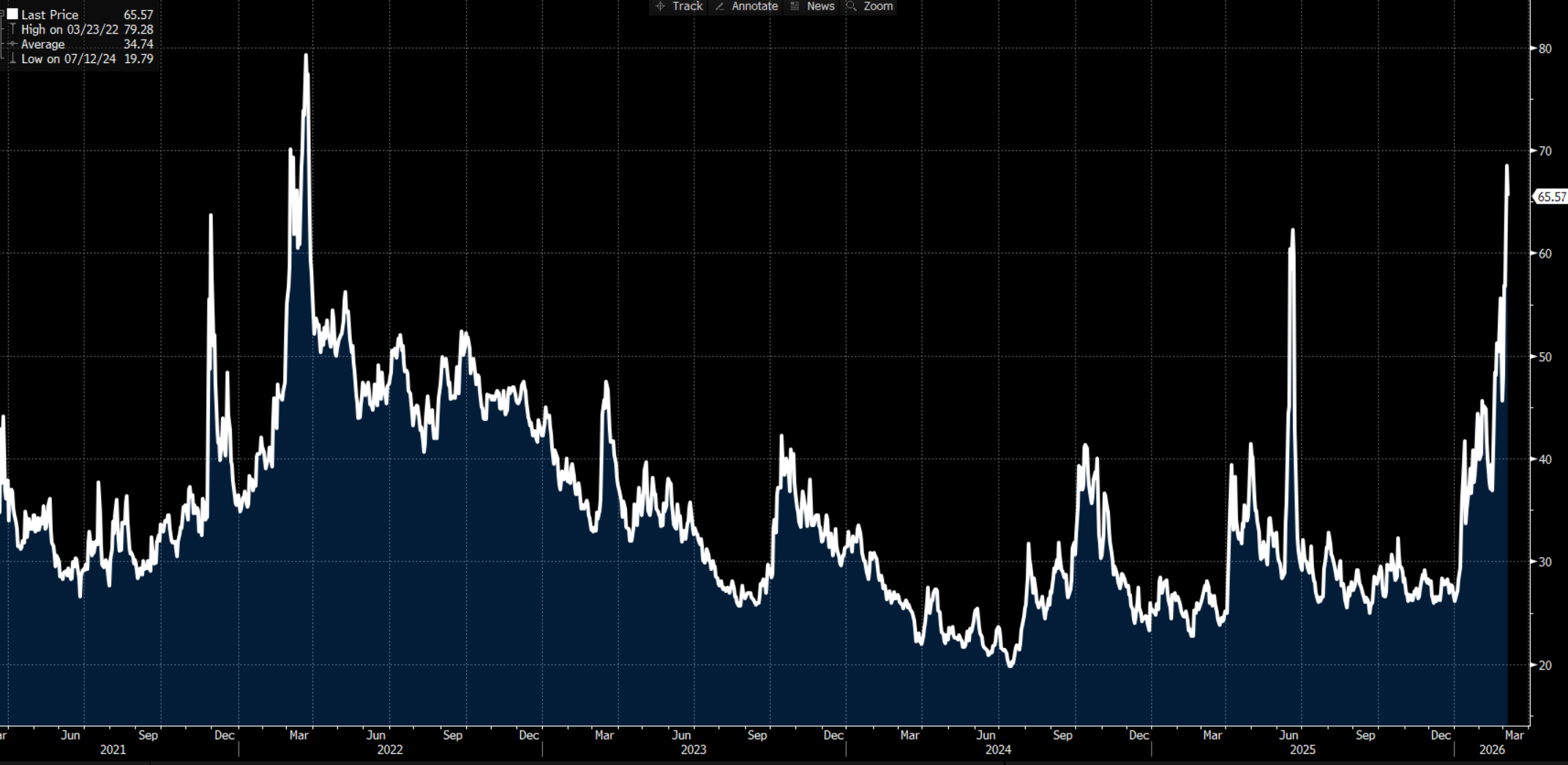

Oil Market Volatility Surges to Post-2022 Highs

A deeper look at market structure highlights the extent of the current volatility.

Brent crude one-month at-the-money implied (options) volatility has surged to 67%. That is the highest level since the Russia-Ukraine conflict in 2022 and double the 12-monh average.

Such elevated volatility raises the possibility that futures exchanges may consider increasing margin requirements to manage risk.

The crude futures curve is also signaling tight supply conditions. Brent crude is trading in steep backwardation, with the front-month contract commanding a premium of about $10.76 relative to the six-month contract.

Further along the curve, the spread between the front-month and twelve-month contracts has widened to $14. These are again the largest levels of backwardation seen since 2022, highlighting expectations of near-term supply shortages.

Strait of Hormuz Disruption Raises Supply Concerns

Supply disruptions are already beginning to emerge.

Six major oil infrastructure sites and refineries in the region have been impacted, reducing output capacity. At the same time, disruption through the Strait of Hormuz remains a major concern for traders.

Confidence in the ability of U.S. security measures to ensure smooth passage through the Strait appears to be declining.

There is storage capacity and tanker availability that can temporarily house oil that cannot be shipped through the Strait of Hormuz. However, this buffer is limited. Estimates suggest production could continue for roughly 25 days before storage constraints force additional facilities to reduce output.

Analysts Model Brent Crude Scenarios From $60 to $120

Market analysts are now modeling a wide range of possible price outcomes.

If disruption in the Strait of Hormuz persists for five weeks or longer and removes roughly four million barrels per day from global supply, analysts estimate that Brent crude could reach a theoretical fair value near $120.

However, the downside scenario must also be considered. Any credible signs of de-escalation could quickly shift market expectations and see Brent crude move back toward a longer-term equilibrium closer to $60. For now, market pricing suggests traders see the risk of ongoing disruptions as more likely, with any meaningful circuit breaker still some distance away.

Crude Oil Options Market Shows Heavy Hedging Activity

The options market further highlights the current risk dynamics. Deep out-of-the-money (5-Delta) one-month Brent call options are trading with an implied volatility premium of 37 volatility points premium to puts. While still below the extremes seen in 2022, this signals strong demand for upside protection.

If traders heard signs of de-escalation, and felt the geopolitical tensions were to ease, traders would unwind these hedges and aggressively sell volatility. That process could push both implied volatility and the underlying crude futures price sharply lower.

Weekend Risk: Potential Gap Moves in Oil Prices

Another important factor heading into the weekend is positioning risk. With volatility at elevated levels, traders face the possibility of a significant gap move in either direction when markets reopen on Monday. As a result, some participants may look to trim excessive exposures ahead of the weekend close and reassess once markets reopen.

Given the extreme levels of implied volatility and the potential for sudden geopolitical headlines, this remains a key risk for traders to manage.

For now, all eyes remain on the weekend news flow and any developments that could determine the next major move in global energy markets.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.