- English

- عربي

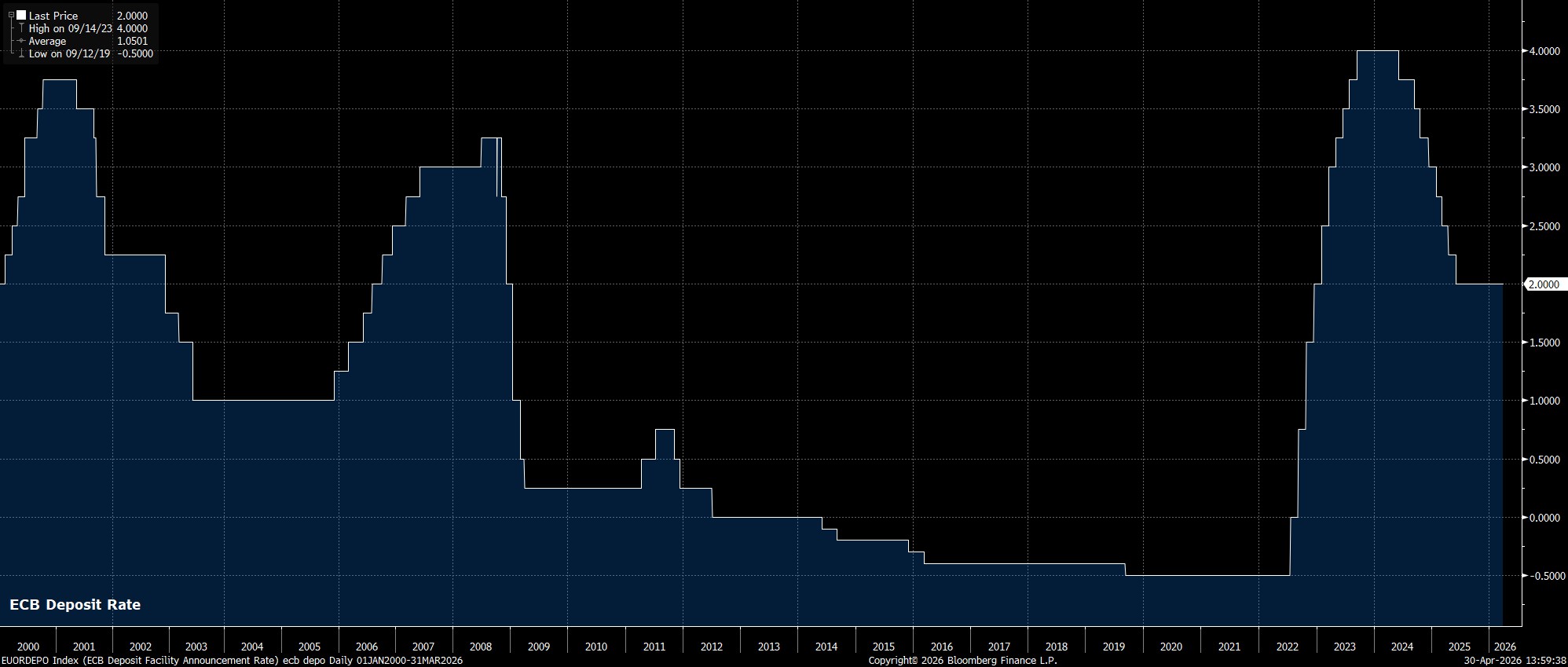

Rates Unchanged

In line with consensus expectations, and money market pricing, the ECB’s Governing Council made no policy changes at the April confab.

Consequently, the deposit rate was maintained at 2.00%, where it has stood since the easing cycle came to an end last summer.

Statement Little Changed

Along with that policy decision, the ECB’s updated policy statement once again reflected the uncertain economic outlook, while also flagging that upside inflation, and downside growth, risks have intensified since the March meeting.

Still, policymakers did once more maintain very familiar policy guidance, reiterating that a ‘data-dependent’ and ‘meeting-by-meeting’ approach will continue to be adopted moving forward, and that no ‘pre-commitment’ is being made to a particular rate path.

Lagarde’s Press Conference

Turning to the post-meeting press conference, President Lagarde noted that the economic outlook remains ‘highly uncertain’ as a result of conflict in the Middle East, which continues to ‘weigh’ on overall economic activity. Furthermore, Lagarde noted that long-term inflation expectations remain anchored around the inflation target, even if inflation is likely to be ‘well above 2%’ in the near-term.

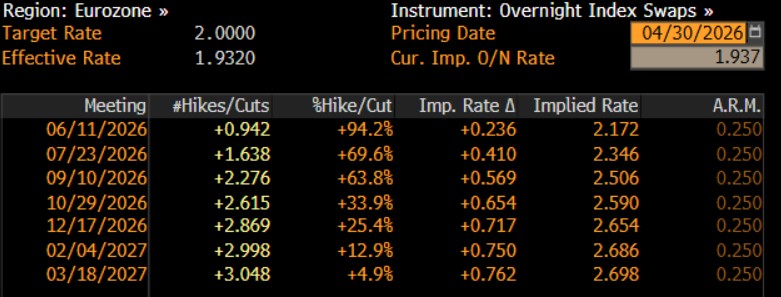

Lagarde also noted that the ECB is ‘certainly moving away’ from its baseline forecast and that, while today’s decision was unanimous, the possibility of a hike was discussed among Governing Council members. Added to which, Lagarde pointed to the June meeting as being a pivotal ‘decision time’ for the ECB, not only considering the updated round of forecasts that will be available at that time, but also the data that will be received in the intervening period.

Conclusion

By and large, the April confab saw the ECB reiterate the ‘wait and see’ approach that they continue to take, amid the highly fluid economic outlook. Although a further rise in near-term inflation is likely, as a result of the further rise in energy prices, the potential for second-round effects remains limited, owing to the weak domestic economic backdrop.

That said, policymakers do appear to be inching closer towards delivering policy tightening, even if such tightening is ultimately likely to prove to be a grave policy error. Depending on how the geopolitical backdrop evolves over the following six weeks, the door to a June hike now seems to be open.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.