- English

- عربي

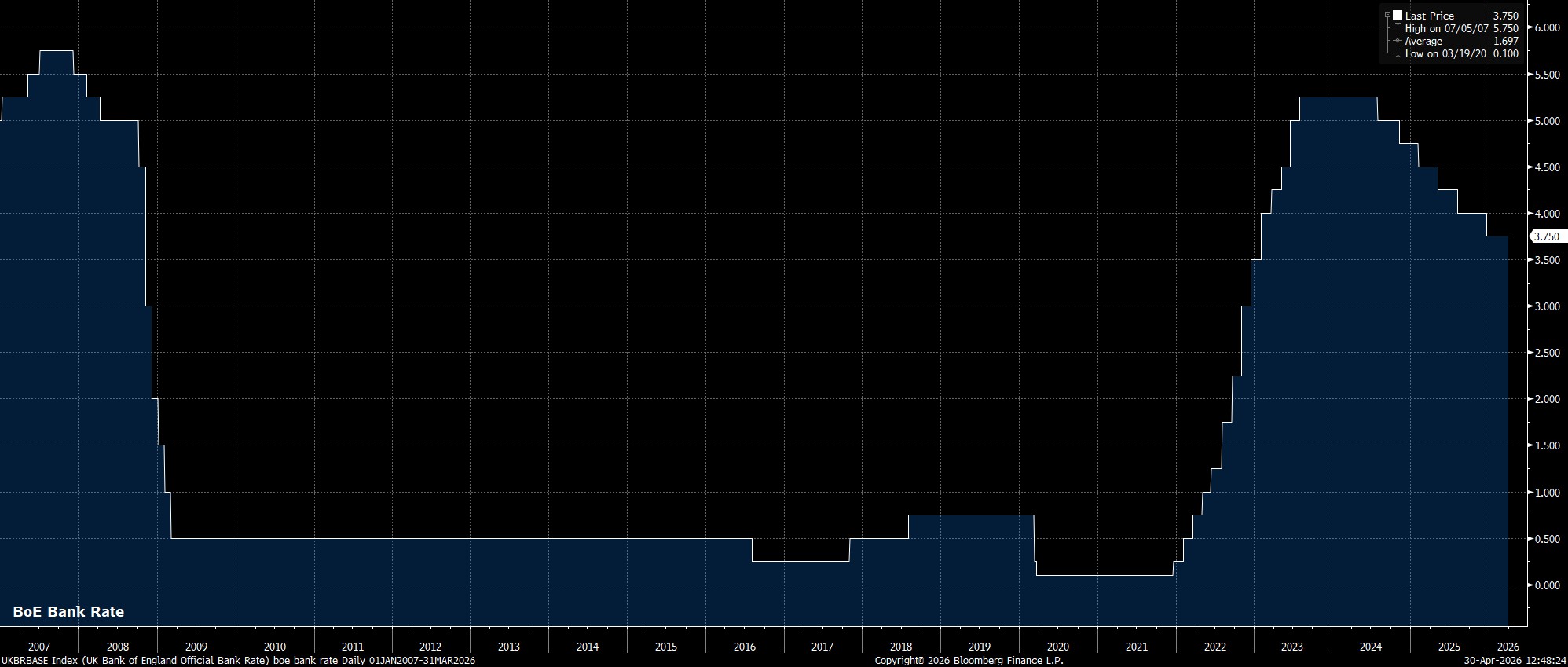

Policy On Hold

As expected, the Bank of England’s Monetary Policy Committee held all policy settings steady at the conclusion of the April confab, maintaining Bank Rate at 3.75%, a level at which it has stood since last December.

The decision to stand pat, for the third meeting running, reflects the ‘wait and see’ approach that the MPC are continuing to adopt, in light of a highly uncertain, and ever-changing, economic outlook, amid conflict in the Middle East, and continued upward pressure on energy benchmarks.

Committee Divisions Return

The decision to stand pat, though, did not come via a unanimous decision, with Chief Economist Pill dissenting in favour of a 25bp hike, noting the risk of second-round effects being ‘skewed to the upside’, and noting how a ‘prompt’ Bank Rate hike, even a ‘modest’ one, could mitigate upside inflation risks.

Regardless, all 8 of the other MPC members were in favour of standing pat for now, with the Governor flagging that leaving Bank Rate unchanged is a ‘reasonable place’ to be for the time being.

Statement Little Changed

Accompanying the decision to stand pat, was the updated policy statement. Here, the MPC made little by way of significant changes compared to last time out, noting once more the potential for second-round inflationary effects to emerge, while repeating a readiness to ‘ct as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term’.

Scenarios Give Little Clarity

Meanwhile, the April meeting also saw the publication of the quarterly Monetary Policy Report. However, in contrast to the usual forecasts, the Bank instead chose to publish a range of scenarios outlining how the outlook may evolve, depending on the degree to which energy prices rise, how long they remain elevated, and the magnitude of second-round effects that may be seen.

However, in attempting to ‘cover all bases’, policymakers have actually provided nothing by way of signal. Take inflation, for instance, which may peak anywhere between 3.6% and 6.2% depending on which scenario one chooses to place more weight on. Similar applies to the unemployment, and growth, paths, which carry such wide uncertainty bands as to not really be worth the paper that they’re written on.

All this, to me, speaks to how uncertain the outlook is at present, more than the Bank attempting to signal any sort of policy reaction. In fact, the Governor himself put the Bank’s reaction function rather well in the minutes, which I shall repeat here – “If the shock appears to be short-lived or the economy weaker, policy should place relatively more weight on avoiding unnecessary contraction in activity. If second-round effects are likely to be greater, policy should focus on returning inflation back to target more quickly.”

Post-Meeting Press Conference

Speaking of Governor Bailey, at the post-meeting press conference, while outlining the various scenarios and policy rules, the Governor noted that under either Scenario ‘A’ or Scenario ‘B’, the necessary interest rate response is achieved simply by not delivering the cuts that were expected in February, not by delivering further policy tightening.

Besides that, the presser offered relatively little by way of fresh information, with the Governor leaning strongly on the various scenarios outlined in the MPR, and seeking not to provide any concrete guidance whatsoever, or box the Bank in to a particular policy path. Frankly, who can blame Bailey for this, given how volatile the situation remains.

Conclusion

Zooming out, this is a Bank of England that, for the time being, are continuing to take a ‘wait and see’ approach, so far as both the economic and monetary policy outlooks are concerned, reflecting the highly uncertain and fluid geopolitical backdrop.

Clearly, focus remains not solely on spot inflation, but on the degree to which second-round effects may emerge, and the risk posed by those effects leading to price pressures becoming embedded within the economy. It is unlikely that the Bank will have adequate data on this risk for a prolonged period of time.

Consequently, although in my view the potential for second-round effects is limited, given that a significant degree of labour market slack remains, and that corporates continue to possess little by way of pricing power, this ‘wait and see’ stance seems set to be maintained for some time to come.

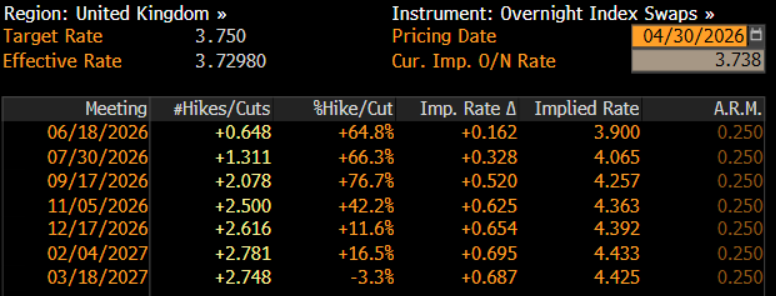

With that in mind, the path to a Bank Rate cut at some stage this year now appears very narrow indeed. The base case, as such, is that the MPC instead stand pat for the remainder of 2026, though further hawkish dissents do seem likely, particularly in the event of a more sustained energy price shock. That said, while the bar to a rate hike is clearly now lower than it was a month ago, there does not yet appear to be a majority of policymakers who are ready to consider policy tightening as appropriate.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.