Macro Trader: Swaps = Dots

It must be said that the hawkish repricing which markets have undergone has not been a straightforward journey. Nevertheless, the labour market remaining incredibly tight, including the blowout +353k jobs which were added in January, in addition to the bumpier than expected disinflation path, to which recent hotter-than-expected CPI and PPI data have nodded, have combined to see market participants ‘wake up and smell the coffee’ that the easing cycle will neither be coming as soon, or turn out to be as aggressive, as had previously been expected.

Unsurprisingly, the hawkish repricing has not been spurred by some sort of collective epiphany among investors that we should suddenly be taking the FOMC’s word on the policy outlook as gospel. If anything, the January FOMC meeting has arguably been the only real ‘dovish’ event of the year, with the Committee having dropped their explicit tightening at that meeting, despite flagging the need for more ‘confidence’ of inflation returning to the 2% target before firing the starting gun on the easing cycle.

This seems more a case of data forcing the market to view the economy, and by extension the likely rate path, through a different lens – i.e., one that points to much more resilience, and somewhat stickier prices (especially in services) than previously expected – rather than the FOMC explicitly steering the market’s opinion.

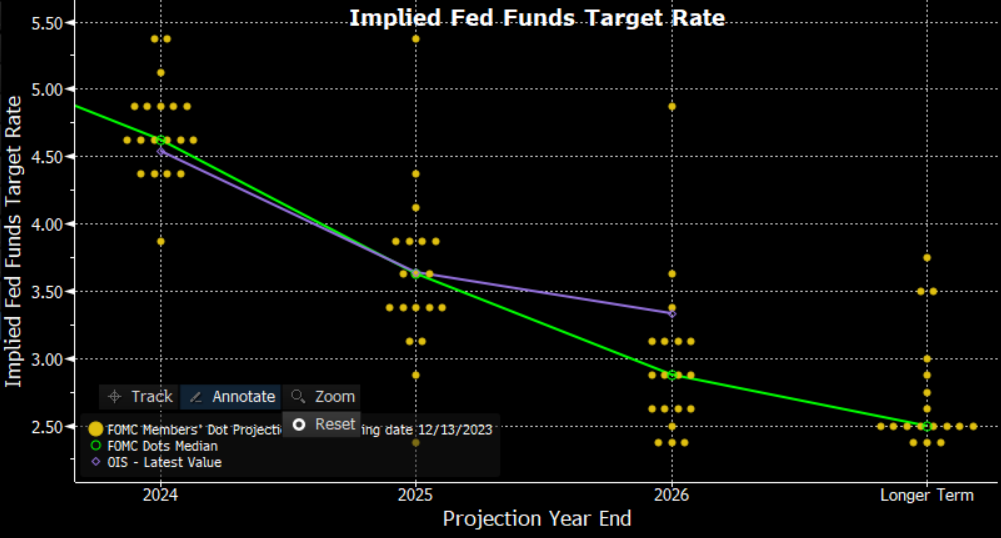

However we got here, the most important thing is that the curve, and the dot plot, are now bang in line with each other. Now we’re here, where do we go next?

Though you should never answer a question with another question, I am going to do so. What market participants should really be asking here is whether Mr Market is now prepared to go further, and price a more hawkish outlook than policymakers have outlined? And, what catalysts would be required for it to do so?

Naturally, one’s mind turns to both inflation, and the labour market, to answer those queries. Handily, we have our latest read on the Fed’s preferred inflation gauge – the core PCE deflator – later this week, with risks to the 2.8% YoY and 0.4% MoM consensus estimates likely tilted to the upside after the aforementioned hot CPI and PPI prints earlier in the month. It is important to note, though, that the calculations for each index, and the basket weights for items included in each, do have some significant variations, particularly when it comes to rent inflation.

In any case, we would likely need to see a significantly hotter-than-expected PCE print to substantially move the needle in a more hawkish direction, particularly with an upside surprise likely already discounted, at least to some extent.

We turn, then, to the labour market, and the next jobs report on 8 March. While it is rather too early at this stage for forecasts for the print to have been modelled and published, it seems likely that payrolls growth will moderate from the >300k pace seen in each of the prior two months. Though, given recent form, one would be wise not to bet against the continuing strength of the US labour market. Once again, we would likely need a materially hotter-than-expected print, probably in line with the January report (+353k NFP with 3.7% or below unemployment and sizzling hot 0.6% MoM average hourly earnings growth) to spark a significant and sustained hawkish repricing.

Taking those two key event risks into account, and also considering that OIS pricing works as a probability distribution, hence some ‘insurance’ will likely remain priced in case of an aggressive easing cycle by virtue of a financial accident, or sharper than expected growth slowdown, it seems that the bar for a further hawkish repricing is a relatively high one.

Some, therefore, are likely to be starting to mull whether now may well be an appropriate time to fade some of the selling that has recently been seen in the fixed income complex, particularly at the front end of the Treasury curve, at least until the next FOMC (and dot plot) on 20th March. I put such a short time limit on that position as it would only take two FOMC members to upwardly revise their end-2024 rate expectation 25bp higher, for the median dot to make an equivalent move higher to 4.875% - putting us back, at least some of the way, to ‘square one’.

Of course, were such a rally – even if short-term – to occur in Treasuries, that begs the question of where the dollar, and risk more broadly, may head.

For the greenback, while one may logically expect lower front-end yields to see headwinds intensify, there are two easily-identifiable issues with this view.

The first is that, as I’ve discussed at some length recently, there is little else in the G10 FX universe that appears particularly attractive to be long of at this moment in time. The BoJ continue to disappoint those expecting a more rapid tightening cycle, the EUR is rather unattractive owing to continued anaemic economic growth, the AUD and the NZD look likely to continue facing headwinds due to the ailing Chinese economy, while the GBP remains at risk from the lagged effects of the BoE’s tightening campaign and subsequent wave of mortgage refinancing, even if recent PMI surveys have pointed to activity beginning to pick up.

Secondly, there is the question not of the short-term rate outlook, but of what happens in the easing cycle as a whole. Given the aforementioned sticky price pressures, particularly in the services space, there remains the residual risk that this will be a late-90s-esque ‘short and shallow’ cycle, rather than the prolonged loosening back towards neutral that markets currently price. This should help to underpin a certain level of demand for the greenback in the medium-term.

_2024-02-27_21-55-47.jpg)

As for equities, at the risk of sounding flippant, I would humbly suggest whether any of this actually matters.

I’m not sure that many would’ve believed me if, at the start of the year, I’d outlined a scenario where markets would price out over 80bp of Fed cuts, the 2-year yield would rise almost 50bp, and that – despite that – both the S&P 500 and Nasdaq 100 would rally to fresh record highs, and print such all-time highs on a near daily basis.

However, that is exactly what has happened, with equities having become detached from near-term rate expectations, instead focusing on something that I continue to harp on about. That being that central banks now have the flexibility, with inflation well on its way back to 2%, to deliver whatever form of easing cycle they deem necessary, at a pace of their liking, while also dispatching any necessary targeted liquidity injections to resolve issues that may occur in certain corners of the market.

It is this optionality, and the flexible Fed put that results from it, which means that the policy backdrop remains incredibly supportive, with said backdrop likely to make playing risk from the short side on anything other than the shortest of timeframes difficult for some time to come.

Related articles

Pepperstone不代表這裡提供的材料是準確、及時或完整的,因此不應依賴於此。這些資訊,無論來自第三方與否,不應被視為建議;或者買賣的提議;或者購買或出售任何證券、金融產品或工具的招攬;或參與任何特定的交易策略。它不考慮讀者的財務狀況或投資目標。我們建議閱讀此內容的讀者尋求自己的建議。未經Pepperstone的批准,不允許複製或重新分發此信息。