- English

- Italiano

- Español

- Français

- English

- Italiano

- Español

- Français

Wall St Struggles Not Yet Mirrored Elsewhere

Looking through a technical lens, it’s interesting to note that the S&P 500 now trades below all three of the 50-, 100-, and 200-day moving averages for the first time since early-January. Clearly, momentum has flipped in favour of the bears, with the gains seen since the turn of the year having almost entirely fizzled out, meaning said move must go down as another bear market rally.

A move below these key levels, as well as the failure of the index to break above 4,200 earlier in the month, paints a dismal picture in the near-term, with a return to the 3,800 region – which marked the lows last December – back on the cards. The descending wedge that is now in place (in green on the above chart) is something that the bears should pay close attention to.

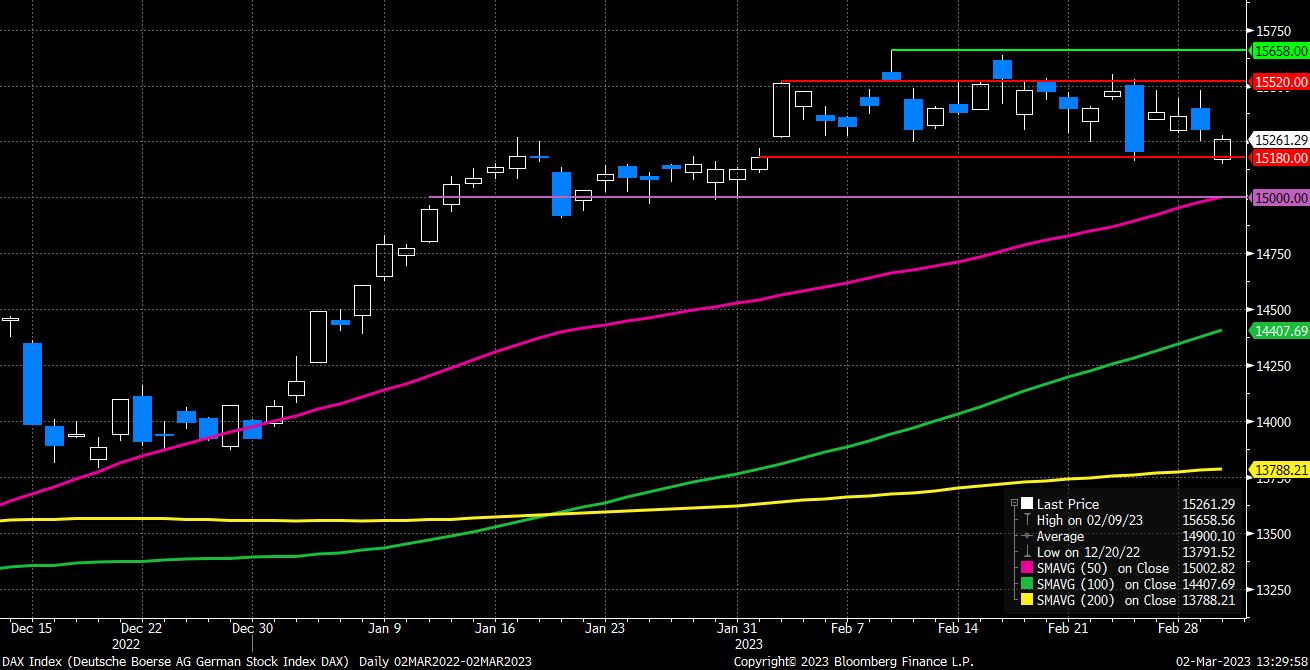

For European stocks, however, the story might not be so grim. The DAX, for instance, despite the sharp losses seen on the other side of the Atlantic, remains within the tight range that has been in place since the start of last month.

The resilience of European equities has been remarkable, though can be relatively easily explained – investors have demonstrated a clear preference for value since the turn of the year, an area towards which Europe is heavily weighted, in addition to the improvement in sentiment towards China, which is a key driver of both the German index, and the German economy.

Bulls will look for price to remain above the 50-day moving average, and the key 15,000 psychological level, above which the index will remain a buy on dips. That said, we would need a close above 15,520 – the top of the recent range – to strengthen the bulls grip on proceedings.

Other European indices are also beginning to look more constructive. Despite having somewhat pared recent gains of late, and backing back under the 8,000 mark, London’s FTSE 100 has managed to hold above the May 2018 highs at 7,885, and above resistance-turned-support at 7,860. So long as price remains above this latter level, it seems logical to retain a bullish bias.

A similar theme is in evidence in Asia. The Hang Seng enjoyed a blockbuster session to kick-off March, vaulting over 4% higher in a single day, allowing the index to break to the upside of the descending channel which has been in place since mid-January, having bounced nicely off the 200-day moving average. Plenty of ticks in the box for the bulls here.

Said bulls likely now have the 50-day moving average, and the 21,000 figure, on their radars.

_Dai_2023-03-02_13-29-34.jpg)

Related articles

.jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.