CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.2% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

- English

- Italiano

- Español

- Français

This complemented the moves on Friday from BoC and PBoC and we should see actions from the BoJ and Bank of Korea shortly – if we don’t act they’re missing a trick. It then didn’t take long before the Fed hit us with a kitchen sink approach, which has come at a time when we’re hearing news that several US states are looking to limit access to public forums, like bars, restaurants and cafes.

RBA QE is a thing

It wasn’t until the Aussie lunch that we saw headlines that the RBA is to roll out its own government bond purchase program. We’ll hear more on Thursday and this may include a token rate cut to 0.25% - but the devil will be in the detail, and we’ll want to know the duration of the bonds being bought (likely 3-5 year maturities), the amount (probably around $60b pa) and anticipated duration. It should come with rock-solid forward guidance. Cash is king and there’s going to be plenty of it around, hence it's not hard to see why the Aussie 3-year Treasury yield has fallen hard, and why we are seeing even better sellers of AUD. AUDNZD to parity?

No real awe from the Fed’s shock

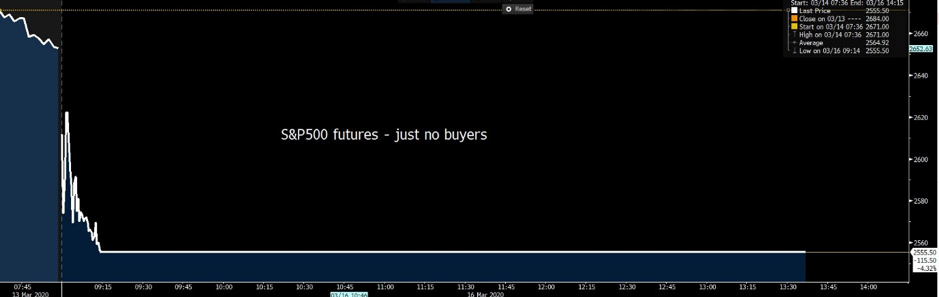

The news from the Fed was certainly punchy, but the logic on the timing was sound and shouldn’t really shock. We needed to see action now, not at a scheduled event later this week - get ahead of curve, as three days in this market is like a month in times gone by. What we have seen can be considered ‘shock and awe’, but the reaction in S&P 500 futures has been less than positive and we see yet another limit down session and there have been no buyers all day. It makes us think the US cash session will be another shocker. In Asia, the Nikkei 225 is slightly higher, while the ASX200 is getting another working over despite the Aussie regulator (ASIC) issuing directions to limit the number of trades high volume participants put through the market.

Moves, or lack of move, in S&P 500 futures today

I guess it partly answers the question whether Friday’s rally was part of a bottoming process or a bear market rally and a part unwind given the extreme pessimism. I favour the latter now. I think the other consideration is flow and the process of liquidation. Today feels like a new wave of liquidations and forced selling and it’s only when this dissipates and positioning has become unwound sufficiently will we see the market try and make a base.

But, it's clear that 9% rallies are far more thematic of bear markets and what we really want to see is massive range contraction, implied vols falling hard and price action to start showing signs of accumulation.

The market's poor reaction to such aggressive stimulus reeks of a market genuinely concerned about the implications for the healthcare system, not just in the US, but globally. And they are genuinely concerned about the sustainability for SMEs (Small and Medium- Enterprises), as there is already an impact being felt here.

Credit to the parts of the market that need it

The Fed, to their credit, have gone to town with great encouragement for banks and depository institutions to use the ‘discount window’, which they made more compelling by cutting the Primary Credit rate by 150bp vs 100bp for the fed funds target range. The Fed has also also cut the Reserve Ratio Requirement (RRR) for these financial institutions and again the hope in both cases here is these institutions are attracted to cheap capital to lend support to the areas of the economy that will need it the most.

The Fed cutting the fed funds target range to 0.25% was fully priced - but we have seen USD swap lines being enhanced with other key central banks. This is important as we have seen the USD on a tear last week, with the demand for USDs ramping up. FX traders have been watching FX basis swaps, and USDJPY and EURUSD, in particular, as they had moved aggressively lower showing a sizeable demand for USDs.

Pink - USDJPY FX basis, yellow - EURUSD basis

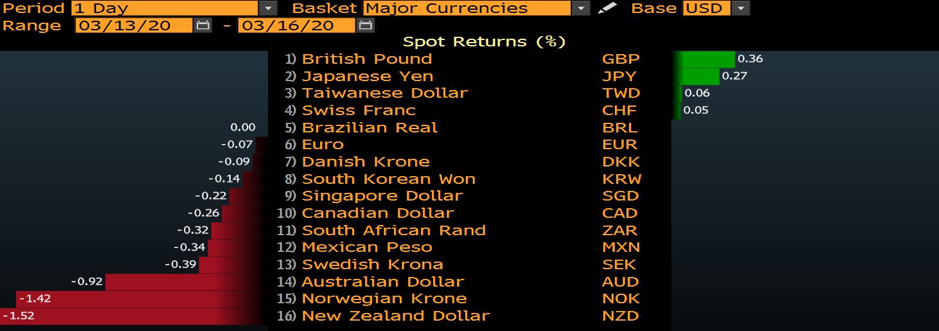

For foreign entities holding USD assets, this would have acted as a quasi-rate hike and no central bank wants to see their currency appreciating in a race to the bottom. It feels like a currency war is underway anyhow and today that winner in the RBNZ and RBA. It feels like EM will lose this one.

FX moves on the day

We are also watching the FRA-OIS spread (for those who aren’t familiar, here is some good info as this has blown up of late, showing greater stress in the interbank market and the Fed needs to offer some policy, such as Term Auction and Commercial Paper Facility.

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.