- English

- Italiano

- Español

- Français

- English

- Italiano

- Español

- Français

Has The Hawkish Repricing Run Its Course?

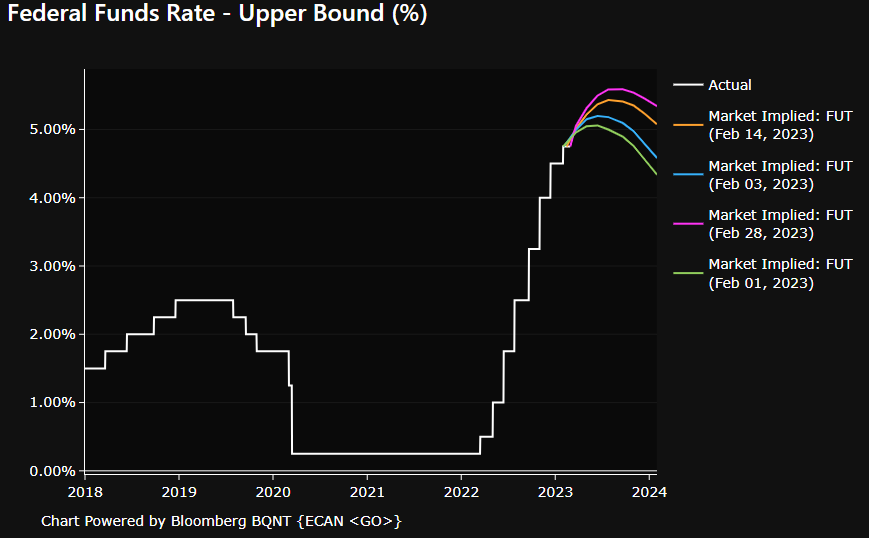

These concepts can, perhaps, seem a little abstract, so it’s best we start with a graphical representation, showing how market rate expectations have shifted so drastically over just four weeks – from pricing a Fed terminal rate around 5% after the last FOMC meeting, to now pricing a terminal rate above 5.5% after a slew of hotter than expected figures; including, the blowout January jobs report, higher than expected CPI and PPI prints, as well as the worrying reacceleration in PCE inflation seen last week.

This is all well and good, but the important question for market participants now is whether this repricing will continue, or whether it is now over. To answer this, we must consider the balance of probabilities – both in terms of where data may print, and what the Fed are likely to do next.

Guidance from the FOMC has been clear for some time, since the tail end of 2022, that rates will go higher than markets expect, and stay there for longer than markets expect. Focus now is on how high rates go, and the duration we stay at the terminal level, rather than the pace at which we go to get there, as was the case last year. Taking this into account, and bearing in mind the downshift to 25bps seen at the February meeting, it seems a long shot that the FOMC would step back up to a 50bps move this month, even if some of the Committee’s hawks are touting such a U-turn whenever they’re near a microphone.

In fact, the market curve seems well-priced at the current juncture, with hikes in the second half of the year a long shot given how, by then, inflation is likely to have continued its bumpy downtrend, and how growth will likely have slowed fairly significantly.

Taking this into account, and considering how high the bar is for the hawkish rates repricing to continue, a prolonged move back above 4% in the 10-year yield – a huge psychological level – seems unlikely.

When we apply this to the G10 FX market, the logical conclusion is that further significant gains for the USD may be hard to come by from here on in, with the hawkish Fed narrative having rather run out of steam. The risk/reward doesn’t appear to favour further USD longs at the current time.

That said, expecting an imminent dollar demise also doesn’t seem especially rational, particularly with consensus increasingly forming around a ‘soft landing’ outcome, and with US data proving resilient for now. Instead, after such a rapid move in February, the greenback could be in for a period of consolidation – a range between 103-106 in the DXY seems a reasonable expectation for now.

_P_2023-03-01_09-15-59.jpg)

Looking across the G10 board, most pairs are sitting at huge technical levels, from which we could quite easily see a modest reversal.

USD/JPY is one that should definitely be put on the radar, with the recent rally having failed to break above the 136 handle – not only a psychological level, but also a confluence of the 100- and 200-day moving averages, with the 38.2% retracement of last year’s decline thrown in the mix for good measure. Leaning short against this level seems reasonable, especially with the dovish Ueda narrative now seemingly discounted by the JPY.

_2023-03-01_09-08-06.jpg)

Cable is also interesting, with the much-talked-about double-top at 1.2445 having failed to play out as expected, with the quid valiantly holding its own, with the bulls thus far able to hold price above the all-important 200-day moving average.

It is still somewhat tough to be bullish GBP, especially when the BoE remain likely to conclude the tightening cycle in March, despite markets pricing hikes through to August. However, a move above the 50-day moving average at 1.2145, which has capped the pair for a number of weeks now, would decisively flip control in favour of the bulls.

_2023-03-01_09-08-01.jpg)

Outside of the FX arena, a peak in yields, the dollar, and the hawkish repricing trade should prove good news for gold.

The yellow metal’s recent declines have stalled out just above $1,800/oz, with the bulls now attempting to take control of matters. A closing break of prior support at $1,850/oz would provide further impetus for the move, with a reasonable short-term target being a return to the 50-day moving average, at $1,866/oz.

_D_2023-03-01_09-07-37.jpg)

Related articles

.jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.