- English

- Italiano

- Español

- Français

- English

- Italiano

- Español

- Français

Analysis

Time:

- FOMC rates decision and quarterly economic projections (SEP) – 4am AEST / 19:00 BST

- Fed Chair Jay Powell’s press conference 04:30 AEST / 19:30 BST

Despite 13 central banks meeting this week and most expected to hike rates aggressively, it’s the FOMC meeting that is the marquee event of the week. With so many variables that could move markets, we look at the core factors that traders should be aware of when assessing risk around the FOMC meeting.

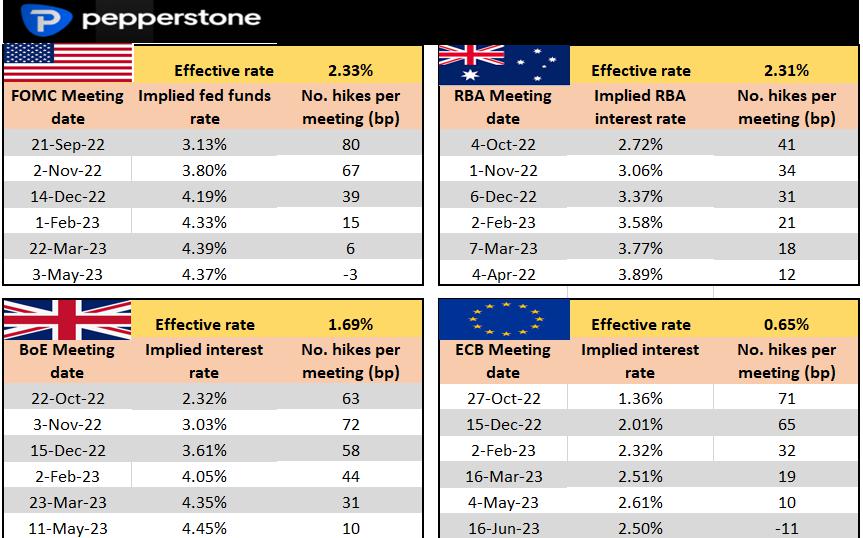

Rates Review – we display the implied rate hike priced by the market for the upcoming central bank meeting, and the step up (in basis points) to the following meeting(s).

- A 75bp hike incoming - Arguably the debate everyone wants answering straight away; will the Federal Reserve hike the fed funds rate by 50bp, 75bp or 100bp – the consensus view (from economists) is they hike by 75bp, with the market pricing in 80bp – this equates to an 80% chance of 75bp and 20% of 100bp. Given the recent (Aug) US CPI print (core CPI at 6.3%), I think we can rule out a 50bp hike. 100bp’s would be a surprise and would make a defiant statement, but again this seems unlikely. So, 75bp is the play and given the elevated expectations in rates pricing, a 75bp hike in isolation offers modest downside risks in the USD.

- The ‘Dot plot’ projections – the Fed offer their individual forecasts for where they see the fed funds rate in the years ahead. The current median projection for 2022 and 2023 is 3.38% and 3.8% respectively – One suspects these will lift to 3.9% (2022) and 4.1% (2023), just under current market pricing.

- With US financial conditions the tightest since April 2020, 30yr mortgage rates at 6.33% and the Fed’s Quantitative Tightening (QT) program about to beef up to $95b a month, Fed chair Jay Powell will be grilled (in his press conference) on how long policy is expected to be restrictive and the signals they are watching to slow the pace of policy tightening.

- Reading the statement, how concerned will the Fed be given likely persistently high core and ‘sticky’ inflation – notably, around core goods, shelter, and rental inflation?

- Turning to Jay Powell’s press conference - Will Powell show reduced confidence that the Fed can bring down inflation and still engineer a ‘soft landing’ in the economy?

- Forecasts on inflation (in the Statement of Economic Projections/SEP) – it wouldn’t shock at all to see its core PCE inflation forecasts lift for 2022 from 4.3% to 4.5%, but will there be any change to the call of 2.7% for 2023?

- Forecasts on GDP (in the Statement of Economic Projections) – in June the Fed forecasted GDP at 1.7% for both 2022 and 2023 – we should see the 2022 GDP forecast cut in half, but will we see forecasts of 1.7% GDP for 2023 revised lower?

- Forecasts on Unemployment - Again, looking at the economic projections, with the Fed expected to forecast a slightly higher unemployment rate for 2022 and 2023. The current forecast is 3.7% (2022) and 3.9% (2023) respectively.

Balance of risk – With the market pricing a 20% chance of 100bp hike and the ‘dots’ likely to modestly undershoot market pricing, it feels there could be a downside bias in the USD into and around the meeting. Any selling in the USD will provide relief to equities, but I suspect this offers levels for the shorts to re-enter. The market will watch the ‘terminal’ rate in fed funds pricing (currently 4.4%) and risky assets should be sensitive to moves in this pricing. US 2yr Treasuries will be closely watched and a move in the yield above 3.9% would be positive for the USD. Conversely, any move below 3.80% would weigh on the USD and boost risky assets.

Positioning – CFTC data shows traders clearly long of USDs, and broad positioning is the most stretched since July 2020. Clients are sensing a turn and are largely positioned short USD, notably vs the GBP and JPY. We see traders net short NAS100 and positioned for a near-term bounce in gold.

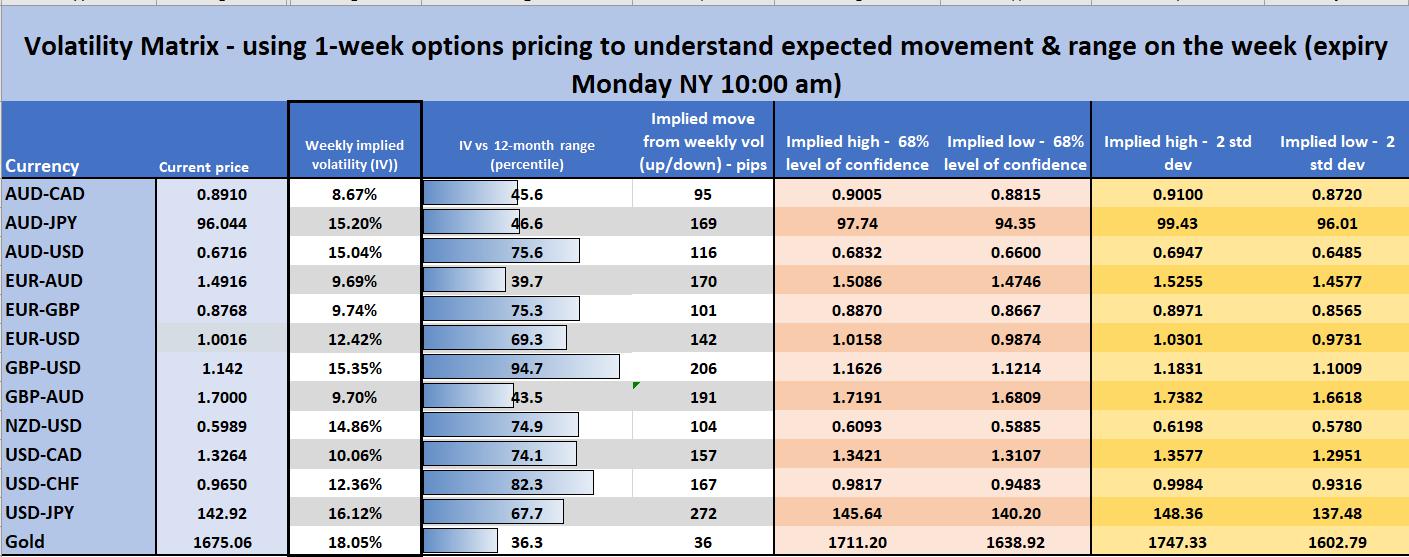

Volatility – Unsurprisingly 1-week FX volatility has risen, notably GBPUSD which is close to the 100th percentile of the 12-month range. We can see the expected move (up or down) over the week and the implied range (with a 68% level of confidence). The market is expecting greater movement, so consider this in position sizing.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.