- English

- Italiano

- Español

- Français

- English

- Italiano

- Español

- Français

.jpg?height=93&quality=100)

Thursday’s ECB meeting should be a relatively calm affair with an autopilot approach the most likely outcome. So where do things stand at present? At the last meeting the ECB communicated an APP purchase schedule of €40bln in April, €30bln in May and €20bln in June. Q3 was signalled as a potential expiry date for the programme (albeit data dependent). The sequencing path expected by most in the market is a termination of APP in July followed by a 25bps rate hike in September.

The risks going into this meeting are tilted to the hawkish side in the event the ECB decide to pull the trigger earlier and wrap up APP at the end of Q2 in June, and pulling forward the rate hike to July (the market prices this with a 62% chance). I think if this was to happen it’s more likely to occur at the June meeting when new economic forecasts will be available. There’s not enough data to evaluate the impact of the war on the eurozone economy yet and the war itself is still very uncertain. Lastly, the uncertainty around the French Elections should see the ECB utilising this meeting as a placeholder before June. However, that being said the minutes were pretty hawkish with some GC members wanting APP terminated in the summer and believing forward guidance conditions for lifting rates had been met or were close to being met. They were also fairly upbeat on the eurozone’s economic outlook despite very obvious headwinds. This was also pre euro area inflation reaching its highest level since the inception of the euro. At the same time, wage growth, a key data point for the ECB has not increased to levels (3%) which they believe would violate their inflation target.

The press conference will be interesting to see if Lagarde makes any comms errors while trying to convey flexibility and data-dependency. Markets are currently pricing in around 70bps by December 2022 and 35bps by September as can be seen in the table below (check the implied rate change column).

(Source: Bloomberg - eurozone OIS pricing)

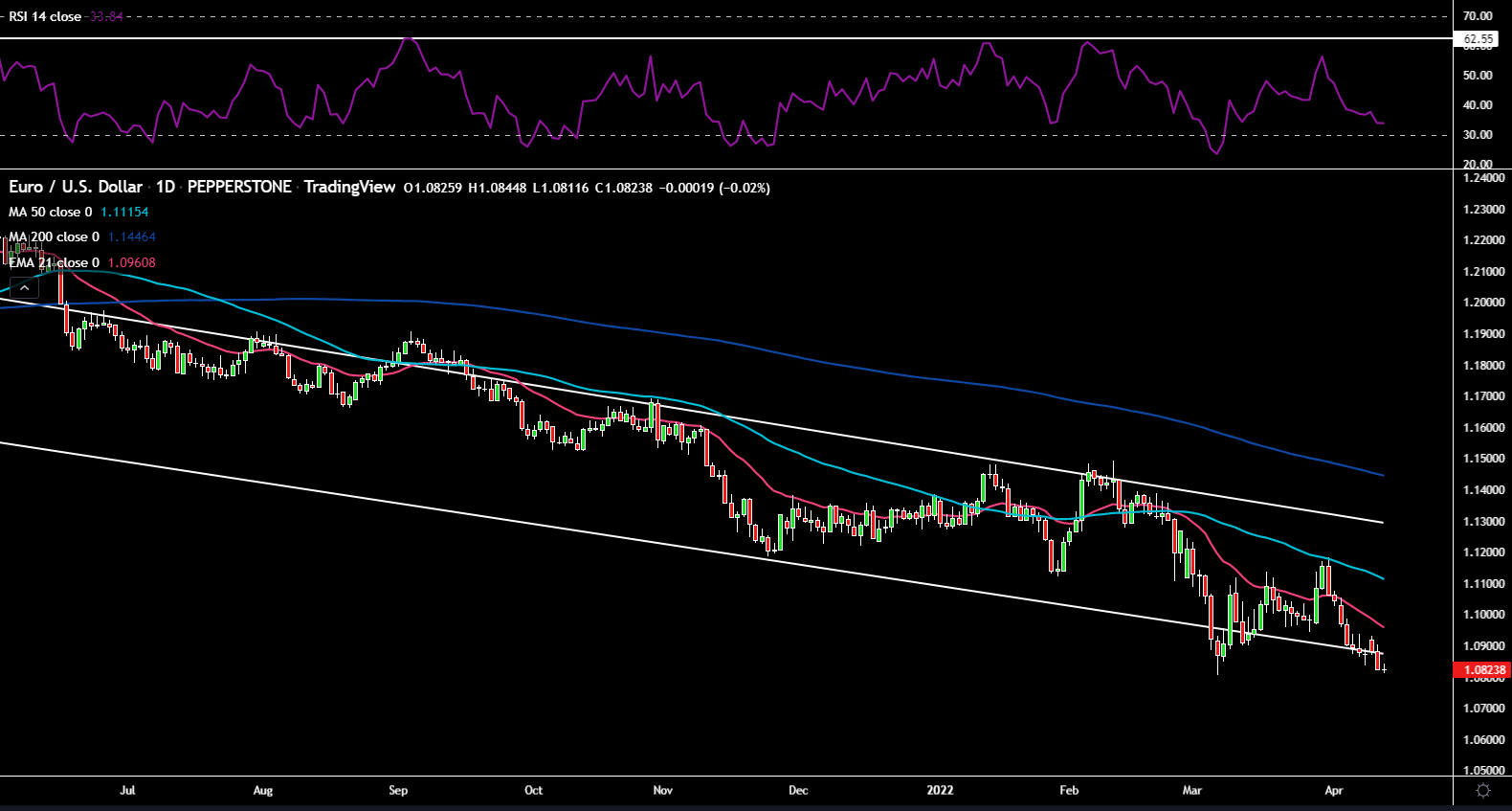

EURUSD:

EURUSD remains around 28 pips from its March low of 1.08. The negative divergence on the RSI is a positive for the bulls who may be expecting a reversal. Could we also be seeing a double bottom forming? A breach below 1.08 would open up 1.075 support. 1.09 on the upside is the level to watch for resistance.

EURGBP:

EURGBP is also close to a key support level around 0.83 and if broken could see price travel towards the former low of 0.82 with 0.825 on the way. The RSI is also showing negative divergence which could see selling pressure run out of steam. On the upside, 0.835 and 0.837 (50-day SMA) would provide some headwinds to further gains potentially.

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.