- English

- Italiano

- Español

- Français

- English

- Italiano

- Español

- Français

Analysis

The debate reinforced by a strong trimmed mean inflation print of 2.1% YoY. In fact, at 0.8% QoQ, this was one of the biggest increases in price pressures in some 8 years and was the first time since 2015 we’ve hit the RBA’s 2-3% target range.

What’s got the markets so interested is the sheer degree of hikes that are priced in the Aussie interest rate markets – they’re flashing game on. The market is effectively feeling we get three rate hikes between now and end-2022, which seems incredibly rich when the RBA will still be undertaking QE at least until February. They’ve also made it known that wages are the cornerstone of sustainably higher inflation and despite a slight tick higher in Q2 wage data (to 1.7%), the RBA really need this above 3% to feel inflation warrants a higher cash rate.

The Q3 wage print is on 17 November and that could be well worth putting on the radar.

We also have increased macro-prudential measures which can be used to cool the demand for credit in the property space, and that could quickly impact sentiment. We should also consider that the RBA is still conducting $4b in asset purchases a month, as well as yield curve control (YCC) and attempting to pin the April 2024 Aussie bond around 10bp.

It’s hard to see the RBA gov Lowe pivoting the bank's guidance towards market pricing with these levers still to pull.

That said, the markets don’t live in the present. They make a set of assumptions and live firmly in the future and adjust as new intel presents itself. The belief expressed in current pricing is that the RBA is going to see inflation that becomes more problematic with wages at the heart of that view. We can look at Aussie 30-day cash rate futures, or swaps pricing, which both tell us over three rate hikes are priced by end-22. Further out and we see Aussie rates really exploding higher, with over six hikes now priced by end-2023.

Aussie 3yr bond yield

(Source: Tradingview - Past performance is not indicative of future performance)

For many, the best place to view this is in the Aussie 3-year bond yield (AU03Y in Tradingview). This essentially captures rates pricing out to three years out and has a strong relationship with rates markets. As we see this has also moved higher with genuine force.

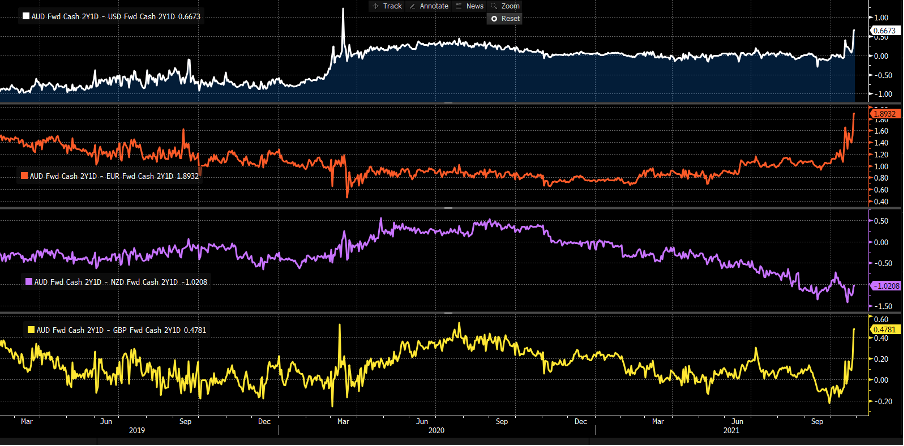

Aussie vs USD, EUR, NZD and GBP rate differentials

(Source: Bloomberg - Past performance is not indicative of future performance)

What’s also important is that the pace of hikes in Aussie rates has been far more aggressive than pricing in the likes of the USD, EUR, and GBP. So rate expectations have been ratcheting up in Australia on a relative basis. This has been supporting the AUD, but some are now questioning whether it’s really advantageous to buy the AUD into what is predominantly a supply shock – granted, demand should ramp up as the economy fully comes out of lockdown and savings rates are drawn down – but how would such a leveraged economy manage a series of hikes?

Even the threat of hikes psychologically has a big impact on the appetite to make big-ticket purchases.

However, near-term, when the Aussie 3-10-year yield curve is flattening, industrial commodities are starting to roll over and the RBA still has a number of levers to pull, one has to question if the market is getting just a little too excited about the prospect of hikes.

Will we really see the extent of tightening that’s priced? And will the RBA really pivot towards market pricing this side of February? I suspect not, and therefore this dynamic may limit the upside in the AUD.

As a trader, having an open mind is crucial especially when it comes to economics and the impact on rates and the AUD. However, one thing seems clear, AUD volatility is likely going to rise and the battle between the vision the market holds around the start date and the extent of rate hikes relative to central bank guidance will be one that we debate for some time.

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.