- English

- Italiano

- Español

- Français

- English

- Italiano

- Español

- Français

Analysis

We see preliminary PMIs in the US, UK, and EU, with the UK and Aus reporting employment data. The US CPI print gets close attention and after Friday’s NFP report this could have big implications on the pricing of a March cut from the Fed - at this point, I am inclined to fade current rate cut expectations, as it still feels like June is a more likely starting point for policy easing. However, a below consensus CPI print would clearly strengthen the case for sooner easing.

US treasuries will again be influential in driving the USD and gold, and while the FOMC meeting and US CPI print will be a clear risk, so could the US Treasury Departments scheduled $37b 10yr (12 Dec 05:00 AEDT) & $21b 30yr bond auctions. I am leaning long of USDs this week but would get greater confidence on a break of 104.31 in the DXY, and a further push towards 7.2400 in USDCNH. USDCHF looks to eye a move into 0.8900.

I am still biased long of US equity indices, with the NAS100 getting good attention as it looks to break the consolidation highs. EU equity is where the momentum traders have focused attention, with the GER40 having closed higher in 8 of the past 10 sessions and sitting at new highs. We see good participation in the rally, with 93% of stocks above the 50-day MA, 72% above their 200-day MA, and 50% at 4-week highs. Perhaps too hot to initiate longs, pullbacks are likely buying opportunities in a bullish trend.

Gold has modest downside risk and I look for 1980/70 to come into play, while SpotCrude upside has been confined by the 5-day EMA, so break here and we should see a quick move to $73.06.

Good luck to all.

The marquee event risks for the week ahead:

UK employment and wages report (12 Dec 18:00 AEDT) – UK wages are expected to increase 7.6% 3m/yoy, a slowdown from the 7.9% yoy pace seen in September. Even though wages are falling, the absolute level of wages still supports the case for the BoE to ease the bank rate in 2H24.

Australia employment report (14 Dec 11:30 AEDT) – the median estimate from economists is for 11k jobs created in November, and the U/E rate to tick up to 3.8%. On the week, I would look to fade rallies in AUDUSD into 0.6670. EURAUD shorts look compelling, although AUD longs would be keen to see a better tape in the CN50.

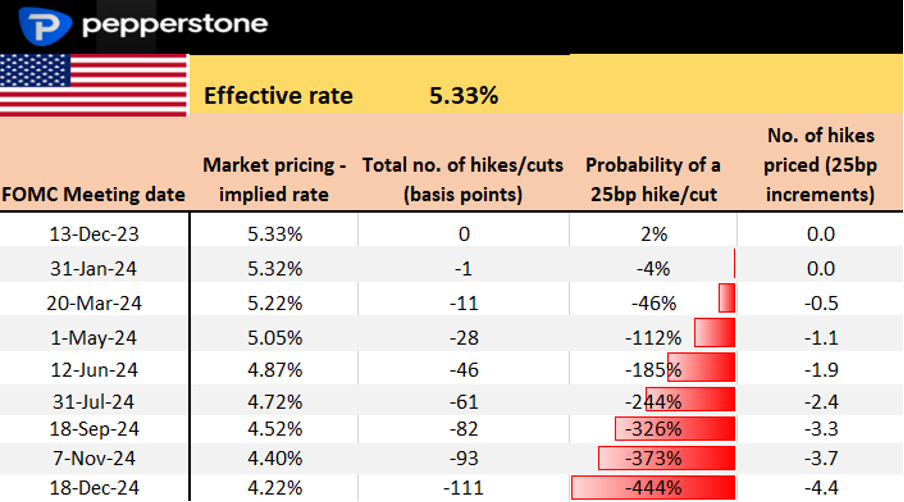

US CPI (13 Dec 00:30 AEDT) – the marquee event risk of the week - the market looks for headline CPI to come in at 0.0% mom / 3.1% yoy, and core CPI at 0.3% mom / 4% yoy. Post US nonfarm payrolls, the market has reduced some of the lofty easing expectations for 2024, with US swaps now pricing 111bp of cuts by Dec 2024. With the market broadly short of USDs, the pain trade is a hotter CPI print, where core CPI comes in above 0.35% mom, resulting in the odds of a March rate cut being pared right back. Risk bulls and USD shorts will want to see a core CPI print below 0.25%, which keeps a cut in March firmly on the table.

Brazil central bank meeting (14 Dec 08:30 AEDT) – The BCB is expected to cut the Selic rate by 50bp to 11.75%. The broad view is the BCB will now cut at every meeting until the policy rate is closer to 10%.

Swiss National Bank meeting (14 Dec 19:30 AEDT) – CHF swaps price a 20% chance of a 25bp cut at this meeting and 67bp by Dec 2024 (or just under three 25bp cuts). Biased towards USDCHF upside this week, with conviction increasing through 0.8828.

Norges Bank meeting (14 Dec 20:00 AEDT) – we see NOK swaps price a 28% chance of a 25bp hike at this meeting, which seems underpriced. A 25bp hike wouldn’t surprise at all, an outcome that could promote a solid rally in the NOK.

BoE meeting (14 Dec 23:00 AEDT) – In theory, this meeting should be a low-volatility affair - There is no chance of changing policy at this meeting, and the BoE should vote 7-2 in favour of no change. With 3 cuts priced by late 2024, there are modest upside risks for the GBP at this meeting.

FOMC meeting (14 Dec 06:00 AEDT) – The Fed will provide new economic projections here, although we shouldn’t see any big changes in their inflation, growth, or unemployment estimates. The focus will be on their projections for the fed funds rate (or the ‘dots’ plot) in 2024. On balance, we should see the median projection for the fed funds rate in 2024 being taken from 5.1% to 4.875%, implying a base case of two 25bp cut next year, although there are risks of a deeper change to 4.6%. With US swaps pricing the fed funds rate at 4.21% by Dec 2024, if the 2024 ‘dot’ is set at 4.875% it could result in USD short covering. The tone of the statement and Powell's presser could also promote USD volatility, where Jay Powell should make it clear they’re not currently talking about easing. Modest hawkish risks in this meeting.

China monthly growth data (15 Dec 13:00 AEDT) – the market will see data on industrial production, fixed asset investment and retail sales. The consensus is for a strong lift in activity, notably in the November retail sales report which is eyed at 12.5% (from 7.6%). China’s equity market continues to attract sellers, and we see no let-up in the bearish trend. We therefore watch to see if the data can stabilize the tape and attract better buyers.

US retail sales (15 Dec 00:30 AEDT) – the market looks for a decline of 0.1% mom, with the control group element rising 0.2%. The outcome could influence Q4 GDP nowcast models, which currently suggest the US is growing at 1.25%.

Banxico meeting (Mexico) (15 Dec 06:00 AEDT) – there is no chance of a cut at this meeting, but the MXN will be sensitive to guidance on the future path of easing. March seems a likely starting point for Banxico to start its cutting cycle. MXNJPY has seen increased interest and should be on the radar given the BoJ meeting next week.

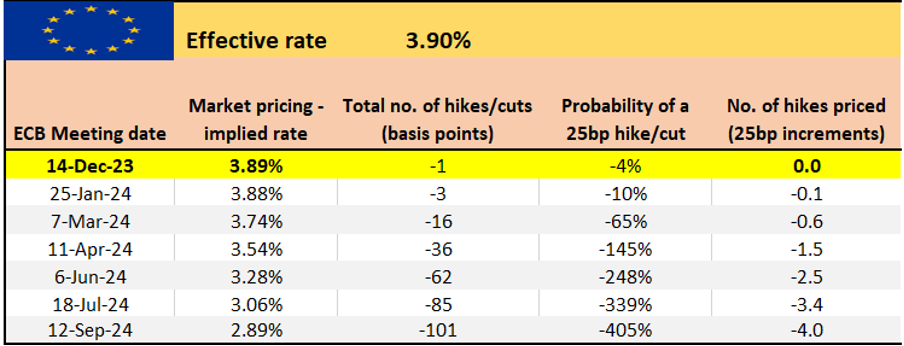

ECB meeting (15 Dec 00:15 AEDT) – the market will see new economic projections from the ECB, with their core CPI estimates expected to drop a touch to 2.8% in 2024, and 2024 GDP at 0.8% (from 1%). Post ECB executive board member Isabel Schnabel’s comments last week on inflation, the door is wide open for a rate cut in April - so EUR traders will be looking at signs around a readiness to cut. We should hear more on the future of PEPP reinvestments and the acceleration of reducing the ECB’s balance sheet.

EU HCOB manufacturing and services PMI (15 Dec 20:00 AEDT) - the consensus is we see the EU manufacturing index coming in at 44.5 (from 44.2), and services at 49 (48.7). Further poor numbers are expected, but recent trends show EU economic data – while weak - has been largely coming in better-than-feared.

UK S&P global manufacturing and services PMI (15 Dec 20:30 AEDT) – the consensus is we see the UK manufacturing index come in at 47.5 (from 47.2), and services at 51.0 (50.9). The market should be more sensitive to the service print, so a read above 52.0 should promote a GBP rally. A read below 50.0 should see GBP under pressure.

US S&P global manufacturing and services PMI (16 Dec 01:45 AEDT) - the consensus is we see the manufacturing index come in at 49.3 (from 49.4), and services at 50.7 (50.8).

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.