- English

- Italiano

- Español

- Français

- English

- Italiano

- Español

- Français

Analysis

A traders’ week ahead playbook – trading opportunities in an evolving world

The world’s market participants continue to debate whether long-end bonds are a good buy as we roll into 2023, given the consensus view of a recession in Europe, the UK, and the US – while China should see a tough 1H23 but a more prosperous 2H23. We debate whether the USD has indeed peaked and whether the seasonal rally in risky assets into the end of the year is on the money this time around. Some macro thematic views to consider but many still feel early to put on in any great size.

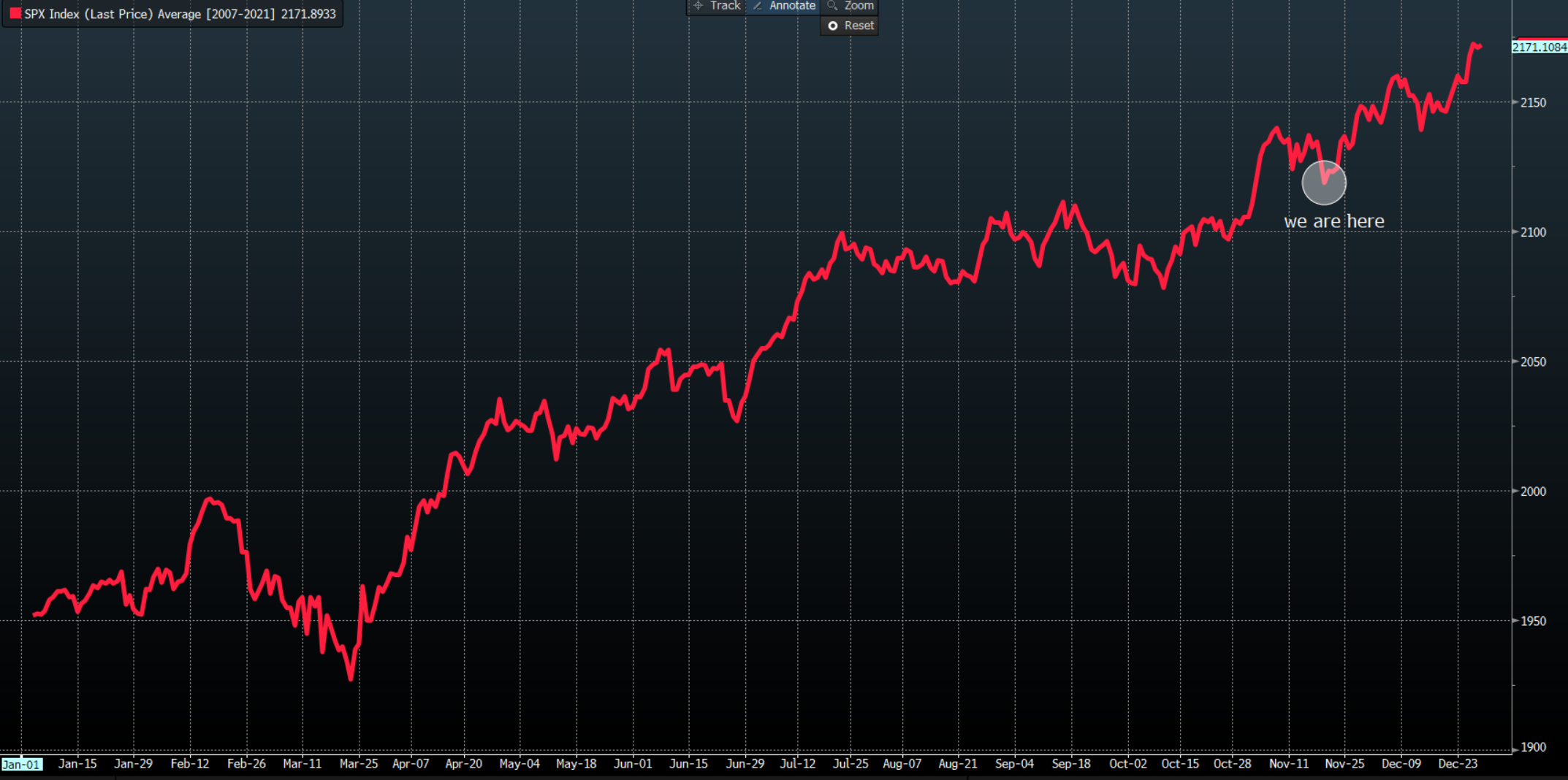

Looking at the data flow for this week it doesn’t feel like any of those debates/views will be accelerated – one aspect which may have kept a lid on any buying of risk last week was Friday’s options expiry, with over $2t of index options notional expiring – having passed, in theory, it means the S&P500 is free to move around more readily. An equity melt-up into year-end is still possible, where a downside break of the 100-day MA at 3917 may alter that view. The 200-day MA on the top side (4068) posed as resistance on 21 April and 16 Aug and may do this time should it be tested – or the bulls may take this one to the bank, we shall see.

S&P500 seasonals – blending the past 15 years performance into one chart to see where we typically get the seasonal strength/weakness

The USD remains central to markets, but with the fed funds terminal rate back above 5% (thanks largely to James Bullard) and US 5YR real rates back to 1.69%, the USD looks supported – clients see this and are holding a net long exposure here.

On a central bank theme, one of the most interesting dynamics last week was Japan’s October inflation rate pushed to 3.7%, equalling the highest level since 2014 and not far off levels last seen in the 1990’s - welcome to the inflation club Japan! Tokyo CPI comes out Friday and that data is for November and therefore it’s more recent - an upside surprise (consensus is 3.6% from 3.5%) could get people looking at future BoJ policy in earnest – With BoJ chief Kuroda leaving the bank next year, we question policy without the keynote dove at the helm.

Trade on the radar - What else do I like as I scan the charts:

Equity indices

GER40 – Along with the CAC40, the GER40 is the strongest of the indices on my watchlist and even when you price in alternative currencies we get the market breaking higher.

HK50 – Like many markets we see consolidation – happy to buy a breakout through 18,500, for 20,000

FX

EURNZD – sitting on the range lows at 1.6770, but we also see potential divergence with the 9-day RSI. The setup looks weak and if this kicks lower then I’ll join, but the divergence may come into play.

USDCAD – One of the stronger looking USD pairs right now – a solid bid coming in at the July highs, and we’re seeing a short-term MA crossover with bullish ROC

NZDCAD – a combo of the prior two set-ups, so this always a consideration for position sizing but we see a close above the 200-day MA and while overbought and testing the June and August highs, this is trending beautifully – I could see the attraction for many wanting to fade into these levels, but the bulls have dominated so far.

EURUSD – ran into a wall of supply into the 200-day MA and 161% fibo extension – the daily suggests this chops around for the time being – so take this into the 30-minute and look at intraday mean reversion moves.

Commodities

SpotCrude - price closed below the 18 Oct swing low, which is also the double top neckline - with a negative 3-day ROC, the target on the downside is $72.

XPDUSD – palladium lost 5.4% last week and is undoing much of the recent rally from 1800. Risks look to the downside.

Cattle – for the breakout traders cattle look strong and is in beast mood – one to hold and wait for bearish 3 and 8-day EMA crossover.

Stocks

I like shorts in COIN and TSLA, with longs in IBM, Merck, and Arthur J. Gallagher.

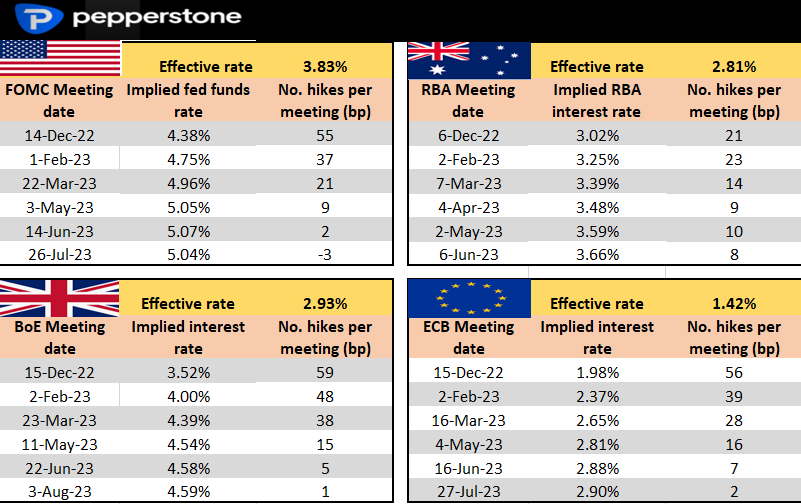

Rates Review – we look at the market pricing and what’s priced for the upcoming central bank meeting and the subsequent step up to the following meetings.

It’s a quiet week ahead by way of known event risks, with many traders taking leave over the Thanksgiving celebrations (Thursday) – on the docket we see the FOMC minutes, RBA gov Lowe speaks (Tuesday 18:00 AEDT), some spluttering of colour from Fed and ECB speakers, an RBNZ meeting (they should hike by 50bp), as well as central bank meeting in Sweden and South Africa. Tokyo inflation (Friday 10:30 AEDT) will be interesting for the reasons expressed above. To many, it has been an underwhelming build up, but we have a football World Cup ahead of us and a chance to revisit the notion that once again “It’s Coming Home”.

With a quiet week in mind, it also offers a chance to look at the big catalysts left on the calendar that could drive into year-end. I’ve looked solely at the marquee event risks, that matter above all else – these dates need to go in the diary. Arguably all roads lead to a 24-hour window in mid-December, where the ECB, BoE and Fed meet and are expected to hike by 50bp a piece – their guidance and economic projections could set the tone into New Year and into 2023.

30 Nov – EU CPI inflation – this print could decide if we see a 50bp or 75bp hike in the December ECB meeting. The current headline CPI estimate sits at 10.7%, so one questions if we see the estimate move north of 11%.

3 Dec – US non-farm payrolls – we know US payrolls always pose a risk for traders – the Fed want to see a cooling of the labour market, but while we did see a lift in the last unemployment rate report at the last report, the US labour market is still in good health. A US payrolls print below 150k could be taken well by markets, but it’s the unemployment rate (which is taken off the Household Survey) that really drives, so a rise from 3.7% could see risky markets (like equity) rally.

6 Dec – RBA meeting – we should get another 25bp hike, but will we get clearer signs of one more hike in this cycle and then an extended pause? Recall, the RBA doesn’t meet in January, so they’ll refrain from being too explicit and committal here and retain a degree of flexibility.

12 Dec – UK CPI inflation – with UK headline inflation at 11.1%, another rise in price pressures could put the BoE in a real pickle – ever-rising inflation and deteriorating growth are not a great mix for UK assets.

14 Dec – US Nov CPI inflation – after last month’s downside surprise (core CPI came in at 6.3%), sending equity sharply higher and slamming the USD, this CPI print could be huge for markets – one could argue it’s the key data point for the rest of 2022 – should we get another downside surprise and risky asset rally hard into year-end.

15 Dec (06:00 AEDT) – FOMC meeting and Chair Powell presser– the outcome of the Nov US CPI print could influence what we hear from the Fed, but moderation in the pace of hikes to 50bp hike seems very likely – given James Bullard’s comments last week for a terminal rate between 5-7%, we continue to view 5% as the minimum level the Fed is targeting for the fed funds rate, but they’d ideally like to get to a point where the fed funds rate is higher than the inflation rate – so this could be a pivotal meeting, especially given we get new economic and fed funds projections at this meeting and the Fed has made it clear they plan to send a message out, portraying that rates are going higher and will stay high. The market prices the fed funds rate to peak at 5.07% by June.

15 Dec (23:00 AEDT) – BoE meeting– a hard one for the BoE and a clear balancing act – the BoE were dovish at the last meeting, but with very high inflation, and with UK households very sensitive to rate hikes and amid a bleak economic outlook, the BoE are between a rock and a hard place. We should get a 50bp hike here though.

16 Dec (00:15 AEDT) – ECB meeting– the market prices 59bp of hikes here, but while we watch for the ECB to get the deposit rate to neutral there is a focus on how the ECB start to unwind its many asset purchase programs.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.