CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.2% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

- English

- Italiano

- Español

- Français

A Busy Week Ahead For UK Traders

As noted, the UK economy is in a relatively delicate spot; despite having avoided sliding into a technical recession in the fourth quarter, all is far from rosy. The latest PMI figures pointed to a continued economic contraction as the year got underway, with all three gauges (manufacturing, services, and composite) having now been beneath the key 50.0 mark between expansion and contraction since last September.

Couple this with deteriorating consumer and business confidence, in addition to other leading indicators heading in a similar direction, it’s perhaps remarkable that cable has managed to hold its ground above the 1.20 handle.

_2023-02-09_16-09-10.jpg)

Having said that, from a technical standpoint cable is in an interesting spot, being sandwiched between the 50-dma to the upside, and the 200-dma to the downside. Implied vols price a range of +/- 161 pips (with a 68% degree of confidence) over the next week, hence these two levels are the first that should be on traders’ radars.

Macro Rundown

So, what could inject a bit of life into the quid, and see us take on the aforementioned levels?

It is a little tough to pinpoint which of the three releases – employment (Tues), inflation (Weds), and retail sales (Fri) – is likely to have the most significant impact on UK assets, given how the MPC appear split not only on the policy outlook, but also on whether upside inflation risks, or downside risks to the growth outlook, should take precedence when making policy decisions.

Consequently, it seems logical to take the data in turn, beginning with the December jobs figures. Headline unemployment should stay at 3.7%, though it is earnings where attention is likely to fall, given the implications of wage growth on the inflation outlook. Earnings growth should cool to an annual pace of around 6.2%, however this is before a range of public sector industrial disputes have been settled, which could see wage growth reaccelerate over the short-term.

Moving on, Wednesday’s inflation print is set to show price pressures continuing to abate, while again pointing to a widening divergence between headline and core CPI measures. CPI should rise by 10.2% YoY, still over 5x the BoE’s target, but a 0.3pp decline on the prior month, as well as marking a second straight month of easing inflation. Core inflation, however, which strips out the impact of volatile food and energy prices, is likely to accelerate once more, to 6.4% YoY, evidencing the difficult predicament that the Bank currently find themselves in.

Rounding off the week, Friday’s retail sales report will prove a key bellwether of consumer health, and is likely to attract extra attention after a dismal festive trading period. Sales are likely to stagnate on a MoM basis, as the cost of living crisis continues to bite. The report will also likely again show how inflation is biting in the ‘real world’, with the value of sales set to rise significantly, even if volume does not; evidencing how, compared to a year prior, it costs more, to procure less.

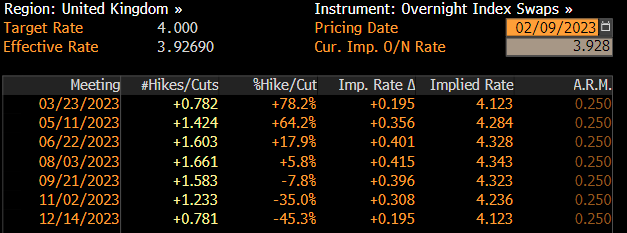

Policy Pricing

The market impact of this data deluge will, almost entirely, depend on how it is perceived to impact the BoE outlook. Money markets presently assign a roughly 75% likelihood to the BoE raising rates by a further 25bps next month, while also assigning a two-thirds chance to a further such hike at the following MPC meeting in May.

In light of recent comments from BoE policymakers, which have by and large taken on a dovish bent, including one MPC member – Tenreyro – even touting the possibility of voting for rate cuts, this pricing seems punchy to say the least. Softer than expected figures, as survey data presently points to, would help to support this view, likely leading to downside in GBP pairs.

Trading the GBP

Said downside is likely to be particularly noticeable against those G10s where central banks remain far from concluding their respective tightening cycles – especially the EUR and the AUD.

EUR/GBP has backed off a little of late, with a foray above the 0.89 handle fizzling out rather rapidly, though the fundamental backdrop – a significant data, and policy, divergence in the EUR’s favour – continues to support a bullish view. A break beneath the pink ascending trend-line would make one want to reconsider, however.

_E_2023-02-09_16-11-13.jpg)

UK Equities Outlook

A softer pound, however, is likely to be good news for the FTSE 100, which trades at all-time highs once more. This is due to the well-known inverse correlation between the two assets, which stems from the majority of the benchmark index’s firms generating the bulk of their revenues from overseas.

_ftse_2023-02-09_16-16-39.jpg)

This latter point is another reason why the index is likely to be able to shrug off any domestic data weakness, given that there is little reliance on UK consumers or businesses for revenue generation. A test, and probably break, above 8000 looks likely in the short-term, especially with the broad rotation towards value names, and out of US indices, set to continue.

Related articles

.jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.