CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.2% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

- English

- Italiano

- Español

- Français

The Daily Fix – A good old-fashioned risk-off day in markets

- A poor ISM manufacturing report triggers broad de-risking

- Cyclical plays shunned - Growth fears resonate through broad markets

- US swaps price a 25% chance of a 50bp cut in September

- Rotation into ultra-defensive equity plays

- CHF and JPY find the love in FX markets

- All eyes on US nonfarm payrolls

Those involved in the US session have had to navigate a real old-fashioned anti-cyclical risk aversion day, and it has got a little moody out there in the markets.

One could argue that the Federal Reserve planted a seed yesterday, by moving its focus so much more to the labour market, which screams out - and has all but confirmed - that their models see the US economy in the late stages of the business cycle. As such, market players, and algo’s are positioned far more sensitively to the marquee growth economic data points and labour market readings and will react more intently to the macro over earnings.

The signal to derisk was opened with the weekly jobless claims coming in at a higher-than-expected 249k, although the punchy cross-asset moves really came alive once the US ISM manufacturing report came in 30 minutes after US equity trade was underway. The numbers were grim, with the headline index in at 46.8 vs 48.8, and well into contractionary territory, with the employment sub-component at a lowly 43.4 and new orders falling to 47.3. It's not great reading, especially with prices paid increasing from the prior month.

From here, we saw a move that would last right through the session and that sets Asia up on a dark and sinister footing.

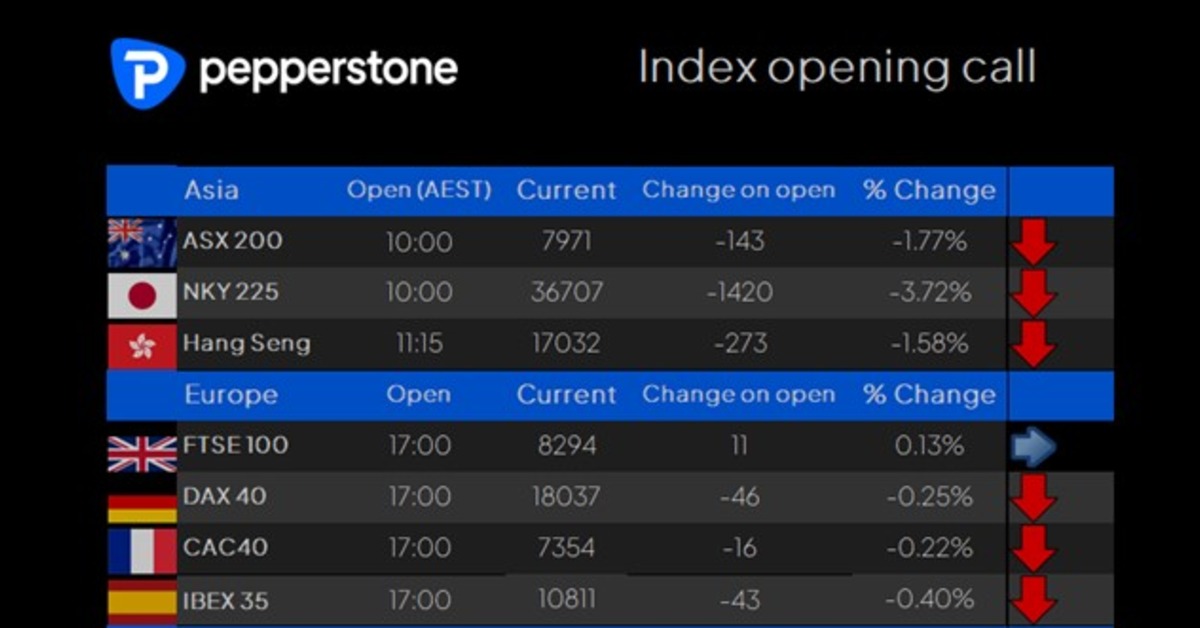

Pepperstone’s index opening calls:

US 2yr Treasury yields fell from 4.28% to 4.13%, and settled at 4.14% -11bp on the day, with eyes now on the YTD yield low of 4.11%. US Swaps now price 31bp of cuts for the September FOMC meeting, essentially a 25% chance of a 50bp cut at this meeting, and we see over 3 25bp cuts priced by December. With 9 25bp cuts priced into swaps over the coming 2 years - this pricing suggests ‘the market’ is moving away from a ‘soft-landing’ scenario to one where the Fed will need to take the fed funds rate below a neutral setting and to stimulate. Perhaps even an element of front-loading upcoming rate cuts, which is a far more worrying sign.

S&P500 sector moves

Any goodwill towards US tech in the prior session has been unwound, with cyclical names taken down hard, although it wasn’t a blanket liquidation, and we have seen rotation into the ultra-safe haven equity sectors – utilities, staples and healthcare, and the plays with low volatility in their cash flow generation. Nvidia, once again, trading like a penny stock with shares closing -at 6.7% and names like QCOM -at 9.4% and AMD -at 8.3% respectively with earnings very much trumping my macro considerations.

We can see high yield corporate credit spread widening out, with the HYG ETF -0.7% and looking dangerously like it wants to break the recent consolidation lows of $78 – put this on the radar, because while corporate credit is still at multi-year tights, if we do see a deterioration in the credit markets then equity will not be happy.

Smalls caps have been taken to the woodshed, with the Russell 2k -3%, and the close in the large-cap indices was hardly much better, with the NAS100 -2.4%.

Volatility has been a major factor, and while we’ve seen the S&P500 trade a massive 155-point high-low range on the session, we’re seeing the VIX index into 18.5%, with traders holding a strong preference for put options over calls. Flow once again exacerbating moves at a both a single stock and index level, with systematic momentum funds selling S&P500 and NAS100 futures as the respective indices traded through their rules-based trigger levels, with volatility dynamic funds heading out of equity and into cash as the higher volatility dictates that they do.

For those positioned for a late-stage rally on the hope that Amazon, Intel, and/or Apple could lift the mood, well, it’s been disappointing as Intel has been smashed 20%, Amazon is 4.8% lower, while Apple is up only smalls in the afterhours session.

Copper is always a go-to market for traders to express a view on economics, and we see an ugly tape here (-2.7%), with selling also seen in Dalian iron ore futures.

In FX markets, we’ve seen some good activity in the GBP, notably post the BoE cutting rates by 25bp, although the fact we see spot at 1.2740 is now more a reflection of USD demand as a haven. The fact the CHF and JPY have found good buyers also speaks to haven demand, with the high yield/high beta Latam currencies finding good selling activity – MXNJPY is in freefall, and rallies will likely be short-lived, as carry trades continue to be taken out to the woodshed.

Clearly, all the focus now falls on US nonfarm payrolls in the session ahead and Asia-based equity traders will be highly cognizant that they will have to hold positions through the US session with the threat of gapping risk on the Monday open.

With the market firmly moving to a mantra that bad news is bad news for risky assets and sentiment, where swaps are pricing an element of more emergency cuts, poor US job numbers will not be digested well at all. While the unemployment rate is calculated from the far more volatile Household survey (as opposed to the Establishment survey), should we see the U/E rate at or above 4.2% and it could get dark in the markets, especially if weather events seen when the survey was conducted result in payrolls coming in below 160k.

Of course, we could see far better jobs numbers, and that may send some relief through markets, but given the market is so focused on whether growth is indeed slowing at a faster pace, there are now some bringing up the notion of a central bank policy mistake, I would therefore argue the broad suite of market players will be far more sensitive to a downside miss to jobs and a higher U/E rate, than a beat.

Good luck to all,

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.