CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72.2% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

- English

- Italiano

- Español

- Français

Week Ahead Playbook: Markets Play Defence Ahead Of Central Bank Bonanza

The Week That Was – Themes

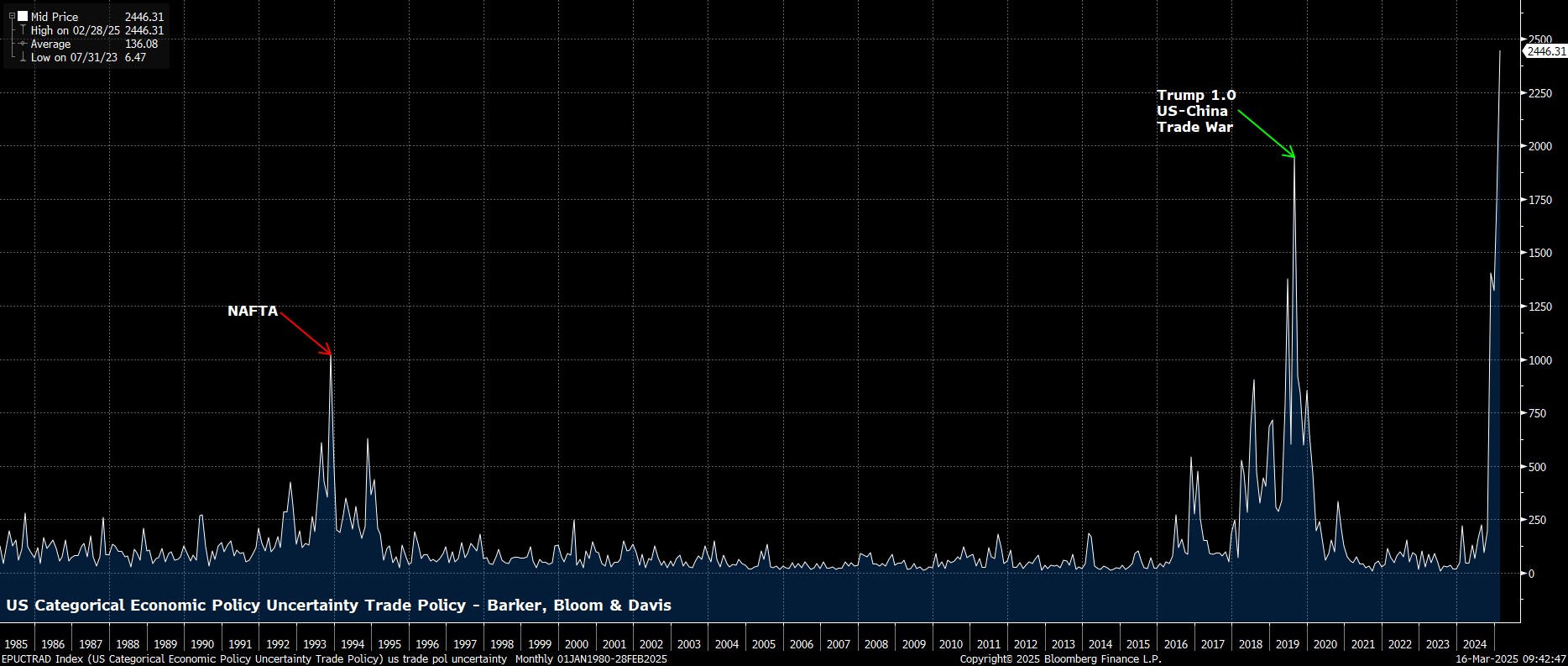

Last week proved, unsurprisingly, to be another where US trade policy dominated the narrative, and where participants were beholden to whatever President Trump decided to post on ‘Truth Social’ at a given time. Those hoping for trade uncertainty to begin to dissipate, however, proved to be sorely disappointed, with the volatile, incoherent, inconsistent, and frankly insane way in which tariffs are being thrown around continuing for yet another week.

Firstly, Trump’s ire was centred on Canada, again, with the Administration threatening to double steel and aluminium levies imposed on imports from its northern neighbour to 50%, before backing down on such a threat just eight hours later. By my maths, that made it six times in seven days that the US had changed its trade policies and tariffs towards Canada. Then, it was the EU’s turn, with Trump throwing a 200% (!!) tariff on imports of European alcohol, in response to an EU threat to charge a 50% tariff on imports of American whiskey.

How any consumer, or business, is meant to plan ahead in such an environment is beyond me, with this degree of policy uncertainty also making it impossible for market participants to accurately price risk, or discount the future policy path.

The detrimental impact on confidence was on full display in the latest UMich consumer sentiment survey, with the index tumbling to 57.9 per the preliminary March reading, the lowest level since November 2022. I would caution, though, that the data is considerably skewed from a political perspective – essentially, if you’re a Democrat (41.4 vs. 51.3 prior), you think this is the worst economy ever, and if you’re a Republican (83.9 vs. 86.7 prior) you think things are ticking along rater nicely. The key question remains when, or indeed if, this plunge in consumer sentiment translates into a subsequent drop in consumer spending, which does seem likely at this stage.

Anyway, the overall strategy from the Trump Administration seems to be one of ‘short-term pain, for long-term gain’. Commerce Secretary Lutnick implicitly confirmed this in one of many media appearances last week, noting that the current Admin “will own the economy” from the fourth quarter onwards. Be prepared for a bumpy ride, a sharp slowdown, and a lot of blaming the prior Biden Administration, until then. Whether the obsequious Lutnick is still in his job by Q4, though, is another matter entirely.

Still, while this might be a politically expedient strategy, and plans to re-allocate resources away from the public and towards the private sector will improve the economy in the longer-run, it is much easier to engineer a slowdown, than it is to recover from one, hence caution being required here.

That said, the Administration, and the FOMC, will have cheered some better than expected figures last week, with CPI having cooled more than expected last month. Headline prices rose 2.8% YoY, while core prices rose 3.1% YoY, the slowest pace since the beginning of 2021. These figures, though, shan’t materially move the needle in terms of the FOMC policy outlook, serving more to reinforce the idea of a bumpy disinflationary path back to the 2% target, particularly with upside inflation risk from those tariffs already imposed, and those coming on 2nd April, plentiful.

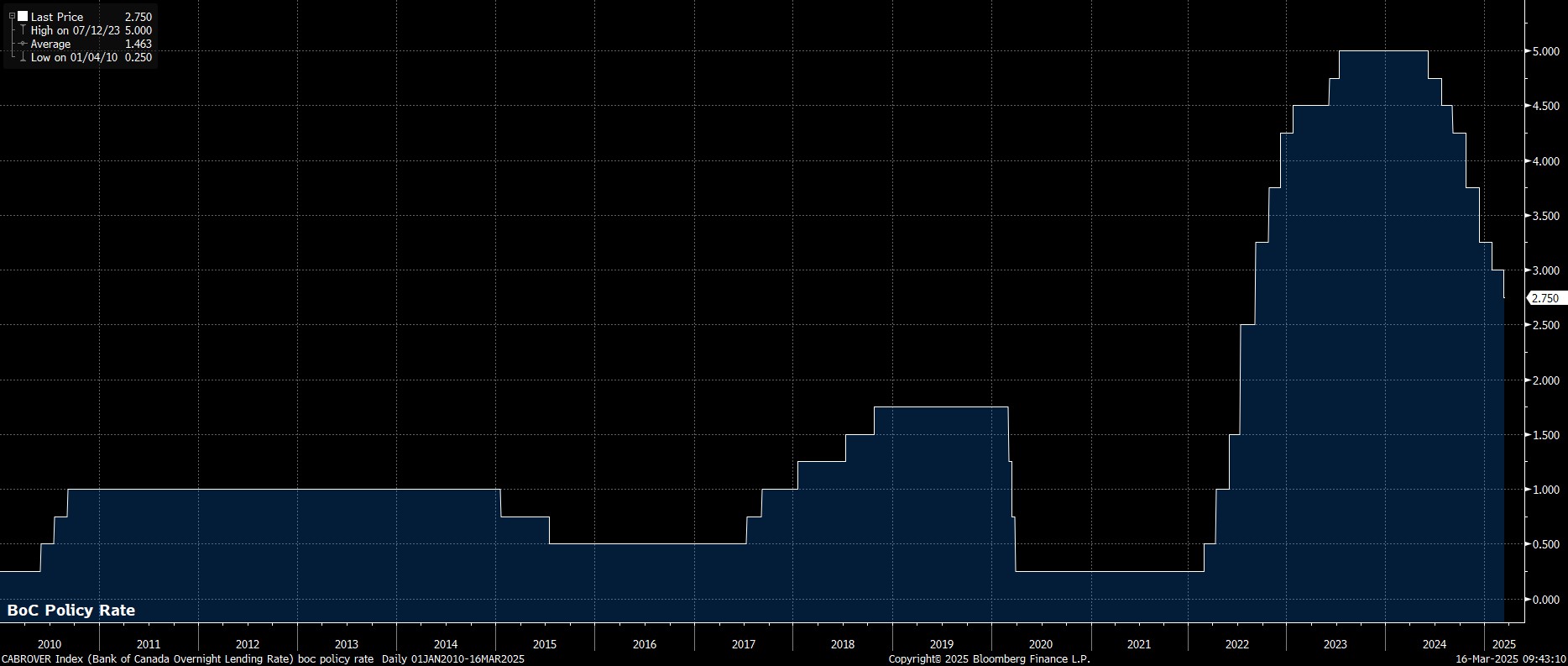

Away from the US, albeit still on the subject of tariffs, the Bank of Canada delivered a 25bp cut last week, lowering rates to 2.75%, bang in line with expectations.

The BoC find themselves in the rather unenviable position of being the ‘only game in town’ at the moment to insulate the Canadian economy from the effects of the ongoing tit-for-tat trade war, particularly amid ongoing political uncertainty. Though PM Carney has now taken office, elections will likely be held sooner rather than later, leaving further rate cuts on the table, as the ‘unreliable boyfriend’ seeks a democratic mandate to continue in post.

On this side of the pond, last week brought a useful, if pessimistic, reminder of the grim economic backdrop here in the UK, with the economy having unexpectedly contracted by 0.1% MoM as the new year got underway.

This contraction did come on the back of the solid 0.4% MoM growth seen in December, though provide further evidence of the anaemic pace of growth which continues to dog the UK economy, and the ‘stagflationary’ backdrop which continues to give the Chancellor a (self-imposed) headache ahead of the Spring Statement on 26th March. Speaking of Reeves, her trying to blame President Trump’s policies for this slowdown is frankly farcical. She would be well advised to have a look in the mirror – and at the brutal tax hikes delivered in last autumn’s Budget – as the catalyst for these grim figures. Reeves is another one who seems to be on borrowed time.

Meanwhile, in Europe, the German Green Party finally agreed to the planned 500bln EUR defence fund, after a bit of prevaricating at the start of the week. In true EU fashion, the three parties involved agreed a bit of a fudge, that will see some additional spending on climate infrastructure, and unlock the full debt brake reform package. Hence, it’s still safe for us to say that Europe is finally getting its fiscal act together, even if it was rather ironic to hear incoming Chancellor Merz touting the importance of “fiscal discipline” when he’s about to add 11% of German GDP to its debt pile!

The Week That Was – Markets

Amid all of the uncertainty mentioned earlier in this note, and the incoherent manner in which US trade policy continues to be made, it proved to be another grim week for risk assets. In short, return of capital is of far more importance than return on capital at this juncture.

Equities on Wall Street slumped once more, with the S&P 500 extending recent declines into a 4th straight week, and falling more than 10% from the record close set in mid-February, hence formally entering ‘correction’ territory. The index has also slipped below the 200-day moving average for the first time since November 2023, and we all know that nothing good ever happens below that fateful yellow line.

_Daily_2025-03-16_09-45-34.jpg)

I still find it tough to advocate for anything other than selling rallies at this moment in time, and remain bearish in the short-term. There is scant sign of the current degree of policy uncertainty lifting any time soon, while both economic and earnings growth expectations must now also re-rate sharply lower as a result of the policies being adopted by the Administration, and the chaotic way in which they are being delivered.

Despite that, as alluded to earlier, if (and it’s a big IF), the Admin are able to effectively re-allocate resources to the private sector, and trim public sector wastage, this should result in a more efficient, productive, and stronger US economy, which does help to reinforce the longer-run bull case for US equities. That’s all some way off, though, and with the idea of a ‘Trump Put’ for the stock market now stone dead, further short-term downside does look to be on the cards.

This has, obviously, sent participants searching for a safe haven, which continues to underpin demand across the Treasury curve, even if trade was choppy last week. Though benchmark 2-year yields did pop back above 4% on Friday, I still like the risk/reward of longs here, particularly as growth expectations roll over, and as the balance of risks increasingly tilts in a more dovish direction for Fed policy. 10s at 4.30% also seem like a solid buy.

It is in the precious metals space, though, that haven demand has really shone through, with gold glimmering once again, as the yellow metal rose north of $3,000/oz for the first time ever intraday on Friday. Though a move north of the big figure prompted a predictable round of profit taking, further upside does seem to be on the cards here, with haven demand unlikely to dissipate any time soon.

Zooming out, one thing to note with gold is how the traditional correlation with real yields has been broken for the last three years, since war in Ukraine broke out. This is not a coincidence, with the seizure of Russian FX reserves at the beginning of the conflict having prompted, or perhaps scared, other EM nations into diversifying their reserve holdings. This diversification, and hence inflows into bullion, seems unlikely to slow any time soon, underpinning the market, and leaving the path of least resistance leading to the upside.

_go_2025-03-16_09-45-54.jpg)

One asset that clearly isn’t a haven right now is the greenback. When participants are seeking to hedge against political uncertainty, and a potential US economic slowdown, the last thing that springs to mind is to buy the very asset that is most exposed to those very factors.

The dollar index, consequently, ended last week with back-to-back declines, and below the 104 figure once more – I still view any USD rallies as selling opportunities, and would be fading any USD upside across the G10 board. Last week saw the EUR run to fresh YTD highs at 1.0947, while cable also remained close to its own YTD best, north of 1.29. Breaks of 1.10, and 1.30, respectively seem like a question of ‘when’ rather than ‘if’, here, though I’d wager on upside beyond those levels being much more likely in the former case, given the grim economic backdrop here in the UK, which participants are trying their best to ignore, but will likely be unable to do so eventually.

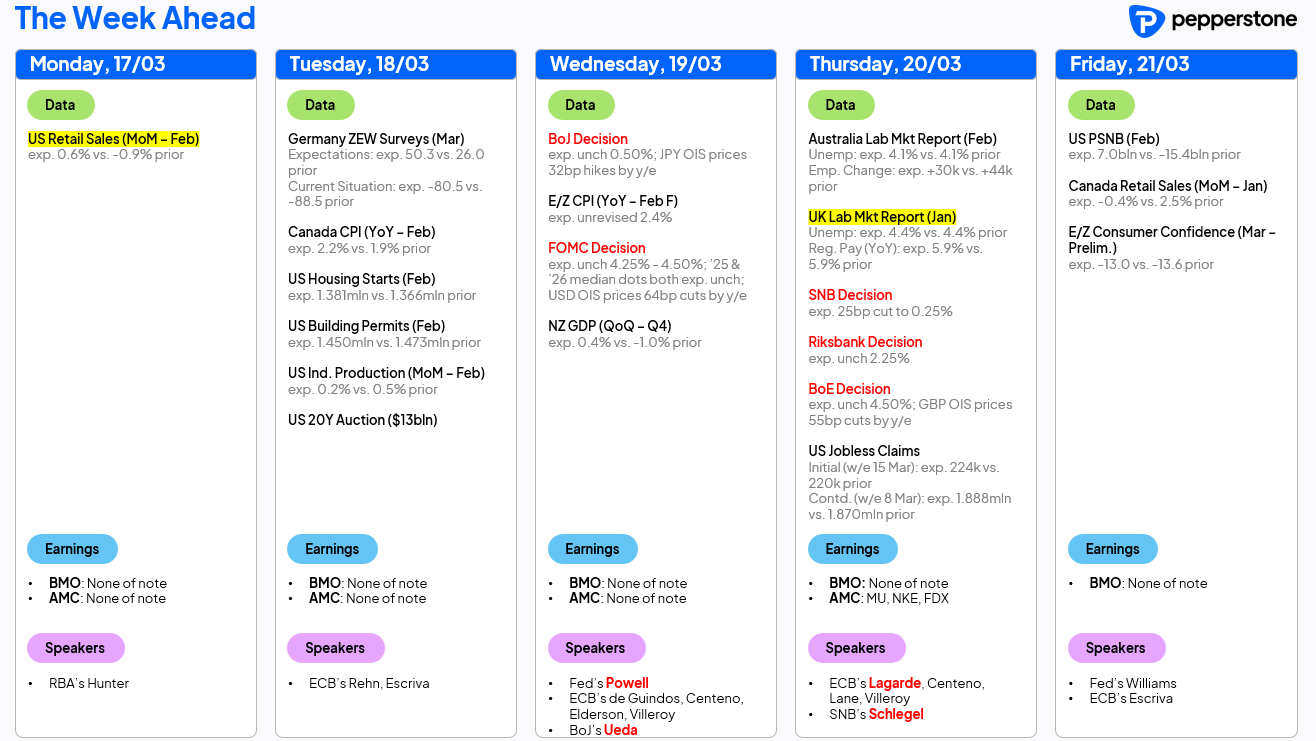

The Week Ahead

A case of ‘no rest for the wicked’ this week, with last week’s chaos being followed up by a monster data docket, all the while the threat of a Trump tape bomb continues to hang over financial markets.

Something of a policy bonanza awaits, with five G10 central bank decisions due, in what will be a hectic 36 hours from Wednesday morning to Thursday lunchtime:

- The Bank of Japan will hold rates steady at 0.50%, though it seems likely policymakers will seek to roll the pitch for another rate hike in relatively short order, potentially as soon as the next meeting in May. Annual wage negotiations seem set to yield pay increases of well over 5%, while CPI recently rose to 4.0% YoY, further strengthening the case for additional policy tightening. The JPY OIS curve prices just 32bp of further hikes by year-end, which seems a little too dovish, even if policymakers will seek not to trigger a significant bout of JPY strength in delivering further rate increases.

- The FOMC will also stand pat this week, maintaining the target range for the fed funds rate at 4.25% - 4.50%, seeking not to ‘rock the boat’ amid the elevated degree of uncertainty which already prevails. Policymakers, though, will likely nudge higher their near-term inflation forecasts, while pencilling in a slower pace of economic growth in the short-term, even as the median ‘dot’ for both 2025 and 2026 remains unchanged, pointing to 50bp of cuts in each of those years. Chair Powell will likely ‘stick to the script’ at his press conference, reiterating that the Fed is in “no hurry” to deliver further rate cuts, but that the economy remains in a “good place” despite mounting headwinds.

- On Thursday, the Swiss National Bank will deliver another 25bp cut, lowering rates to 0.25%, in what will likely be the last rate cut of this cycle. This, though, would only leave policymakers with 25bp of headroom in the event of downside economic surprises before having to reach into the NIRP/ZIRP toolbox that we had all hoped would never be seen again.

- Meanwhile, the Riksbank will hold rates steady at 2.25% at the March meeting, with recent inflation figures having surprised to the upside. While the direction of travel for rates remains lower, the pace of future cuts is likely to be relatively slow, with CPI likely to remain above the 2% target for much of the year

- In a similar vein, the Bank of England will hold Bank Rate steady at 4.50%, in what will likely be an 8-1 vote, as Dhingra dissents in favour of another 25bp rate reduction. Guidance is likely to be unchanged from that delivered in February, noting a “gradual and careful” approach to future rate cuts. The outlook remains particularly cloudy, ahead of April’s National Insurance hike, and with headline CPI likely to rise towards 4% by the end of summer. Further cuts, though, remain likely, with quarterly 25bp cuts, taking Bank Rate to 3.75% at year-end, remaining my base case.

Away from all that, there’s plenty else of interest.

Monday’s US retail sales figures will be pivotal in terms of the broader growth scare narrative, with market participants likely to be in no mood whatsoever to forgive a downside surprise here, which would only serve to heighten concerns over a deeper economic slowdown. Meanwhile, jobs figures are due from both Australia and the UK, though the latter remain highly unreliable amid ongoing ONS data collection issues.

Elsewhere, a couple of notable corporate earnings are due, including semiconductor name Micron, as well as classic bellwether stock FedEx, who may help to provide a broader read on US economic conditions.

Lastly, despite the busy data docket, participants will also remain on high alert for the latest musings from the White House, in turn likely leading to a defensive, cautious bias persisting once more.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.